Quantum Dot Solar Cell Market: Size, Share, and Future Growth

Other |

2026-05-26 04:25:43

As organizations accelerate the shift from centralized cloud models to distributed compute fabrics, fog computing is emerging from research labs into mission-critical production. Our latest Fog Computing Market report positions C-suite leaders and technology strategists to make decisive 2026 investments by synthesizing market momentum, vendor dynamics, standards activity, and program-level playbooks. This brief distills the report’s strategic value without revealing proprietary segment-level numbers—serving as a trailer that highlights the decisive analysis you need to plan, procure, and partner with confidence.

Fog Computing Market

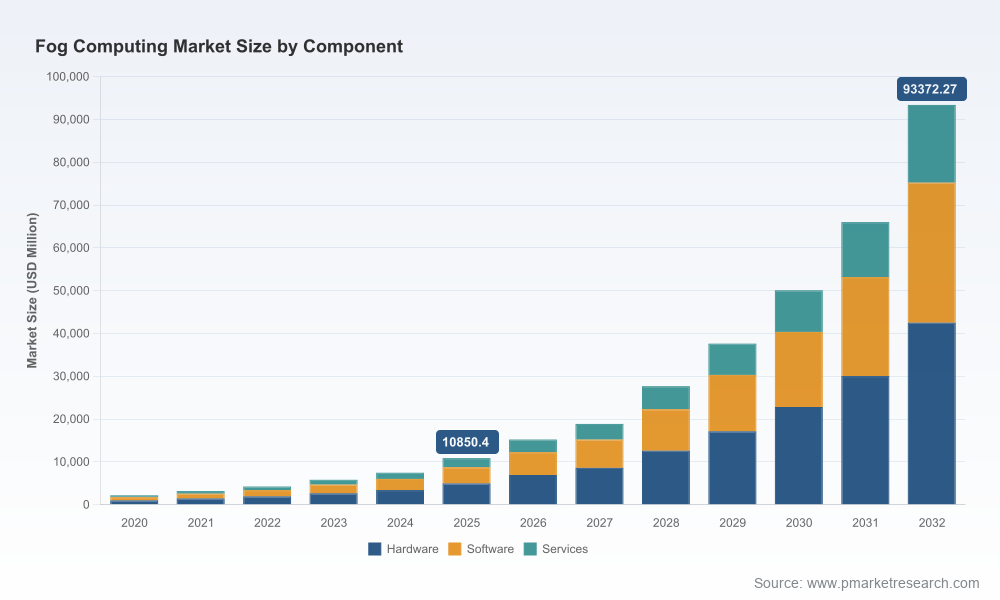

Fog computing is not incremental — it is exponential. The market expanded rapidly over the 2020–2025 historical window and, as our analysis shows, continues to accelerate into the forecast period. To put the momentum into perspective: the global fog computing market rose from the low billions in 2020 to a multi-billion-dollar industry by 2025, and is projected to reach mid-double-digit billions in 2026 and to exceed nine figures by 2032. That trajectory corresponds with a robust compound annual growth rate of approximately 36% across the forecast horizon. For decision-makers this means three realities: (1) the technology is no longer optional in many industrial and latency-sensitive contexts, (2) procurement windows are compressing as use cases mature, and (3) competitive advantage will be captured by those who move early on architecture, integration, and standards compliance.

Fog Computing Market

From pilot to production: 2026 is when many earlier pilots will either scale or be retired. Our vendor and use-case benchmarking demonstrates that operationalization risk is now the dominant gating factor — not fundamental technology feasibility.

Fog Computing Market

Standards and regulation convergence: With normative guidance from NIST and active standards work at IEEE, the next 12–18 months will determine which architectures achieve broad interoperability. Organizations that align early with these emerging norms capture integration and procurement advantages.

Security redefinition: The threat landscape for distributed compute has evolved; quantum-resistant cryptography and edge-aware anomaly detection are moving from R&D to procurement checklists, particularly for critical infrastructure and industrial deployments.

This study was designed to be a practitioner’s compass. It combines market sizing and scenario modelling with granular, executable workstreams for enterprise adoption. Key practical deliverables include:

Architecture blueprints: multi-tier reference designs that map fog nodes, edge gateways, cloud integration, and orchestration planes to specific operational constraints (latency, bandwidth, data sovereignty, and manageability).

Go-to-market and procurement playbooks: tender-ready requirements templates, RFP criteria aligned to standards (including manageability, telemetry, and security), and procurement timing guidance calibrated to the forecast growth curve.

TCO and ROI models: scenario-based financial tools that compare centralized cloud, edge-only, and fog-augmented deployments across CapEx and OpEx vectors, including migration timelines and break-even analysis.

Vendor assessment framework: a repeatable scoring model weighing technical depth, product maturity, interoperability, services capability, and ecosystem partnerships — enabling rapid shortlisting without reliance on vendor marketing claims.

Program risk matrix and mitigation playbook: identifies integration, operational, cybersecurity, and regulatory risks with prescriptive mitigations (including recommended cryptographic roadmaps and incident-response design for distributed nodes).

Standards and compliance mapping: practical guidance on aligning implementations with NIST conceptual models and the evolving IEEE edge/fog standards, and a checklist for alignment with consortium reference architectures.

The fog computing ecosystem blends hyperscale software, specialized industrial offerings, silicon architects, and niche platforms for real-time analytics. Market concentration remains relatively low: the top three vendors account for less than a fifth of the market and the top five remain well under one-third — a structure that supports both incumbent leadership and fast-follow innovation.

Cisco Systems (San Jose): an originator of the fog concept and provider of platforms that enable containerized applications at the network edge. Cisco’s strengths lie in networking integration, secure device-to-fog connectivity, and operational familiarity with large industrial portfolios.

Dell Technologies (Round Rock): hardware and systems expertise tailored to ruggedized fog architectures. Dell’s value proposition is infrastructure reliability and lifecycle services for distributed compute hardware.

Microsoft (Redmond): brings hybrid cloud-to-fog continuity with solutions that extend cloud-native services into the fog layer, accelerating AI and IoT workloads with consistent management paradigms.

ARM Holdings (Cambridge): foundational IP for energy-efficient processors that power most fog/edge endpoints; their roadmap materially affects power, CPU capability, and cost curves of node deployments.

FogHorn Systems (Sunnyvale): software-centric provider focused on real-time analytics and industrial use cases, offering differentiated edge AI tooling for latency-critical operations.

GE Digital, Fujitsu, Schneider Electric, and ADLINK Technology: each brings domain-specific strengths—industrial OT integration, 5G-enabled smart manufacturing, energy management platforms, and rugged hardware, respectively—making them preferred partners in verticalized deployments.

Niche innovators (e.g., Nebbiolo Technologies, Crosser, IOTech): provide specialized fog platforms, open-source integration options and vertical optimizations; they are common targets for strategic alliances or acquisition to accelerate specialized capabilities.

Choosing the right partner requires matching capabilities to program intent. For example, network-integrated vendors are optimal where large, distributed connectivity fabrics and operational continuity are the priority; cloud-native platform providers excel when rapid AI lifecycle management and hybrid orchestration are the core requirements; industrial specialists are preferred where deep OT integration and compliance constraints dominate.

Fog deployments are being shaped by a convergence of normative frameworks and regulatory expectations. PW Consulting’s analysis highlights several important influences:

NIST’s conceptual model: provides a neutral architecture to classify fog components and interfaces—essential for procurement language and interoperability testing.

IEEE activity: ongoing standards work on nomenclature, taxonomy, and manageability is reducing integration uncertainty; early alignment reduces vendor lock-in and accelerates time-to-production.

Reference architectures: consortium work from industry founders established core design patterns emphasizing scalability, security, and interoperability; these patterns should be embedded into enterprise architecture wrappers.

Security imperatives: recent patent-level activity in quantum-resistant encryption and edge-aware anomaly detection underscores the trend toward elevating cryptographic resilience at fog nodes, not just the cloud. For critical infrastructure, quantum-aware roadmaps and federated threat detection should be procurement requirements in 2026 RFPs.

Prioritize architecture-first pilots: run three parallel pilots that test (a) latency-critical control loops, (b) data-reduction and privacy-preserving analytics at the fog layer, and (c) lifecycle management across distributed nodes.

Embed standards compliance in contracts: include interoperability and manageability KPIs tied to IEEE/NIST-aligned test cases to de-risk multi-vendor architectures.

Build a cryptographic migration plan: require vendors to provide timelines for quantum-resistant algorithm support and distributed key management capabilities.

Design for operational tooling: invest in telemetry, centralized orchestration, and firmware/patch management systems before scaling hardware roll-outs — the marginal utility of automation increases with scale.

Adopt blended sourcing: combine hyperscaler platforms for orchestration and AI model lifecycle with specialized hardware and industrial software providers for on-premise robustness.

Create an acquisition and alliance map: identify boutique vendors and platform specialists for potential partnership or bolt-on acquisition to accelerate differentiated capabilities.

Leaders considering fog in 2026 face compressed decision cycles and heightened expectations for ROI, security, and standards alignment. Our report translates the market’s macro momentum — including the high-growth forecast and the still-fragmented vendor landscape — into step-by-step implementation guidance, financial models, risk mitigations, and vendor shortlists tailored by program archetype. The intention is not to prescribe one-size-fits-all answers, but to provide the decision frameworks that produce repeatable success across industries and deployment scales.

This executive brief highlights the strategic contours. The full report contains the underlying scenario matrices, validated vendor scoring, use-case economic models, procurement templates, and the segmented insights that executives and procurement teams need to move from intent to execution. To access the complete intelligence — including the granular datasets and recommended vendor pairings tailored to your industry — please consult the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Fog Computing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com