Shocking Facts About Buy FFxiv Gil Told By An Expert

Games |

2026-06-16 07:55:16

PW Consulting’s new market study on High Barrier Machine Direction Oriented Polyethylene (MDO‑PE) film, with a 2025 base year and a 2026–2032 forecast window, is designed as an operational playbook for executive teams planning resource allocation, product roadmaps, and partner strategies for 2026. At the macro level the market demonstrates strong expansion — our modeling shows a sustained compound annual growth rate (CAGR) of 14.5% through the forecast period, with the total market expanding materially from the 2025 base to a multi‑hundred‑percent larger market by 2032. For companies operating in packaging substrates, barrier coatings, film extrusion or flexible packaging converting, the choices made in 2026 will disproportionately determine competitive positioning through the decade.

High Barrier Mdo Pe Film Market

Sustainability requirements are no longer theoretical. Tightening regulations — notably EU mandates on recycled content and mono‑material preferences — are accelerating conversion away from multi‑material laminates toward mono‑material PE structures that can meet circularity targets without sacrificing barrier function.

High Barrier Mdo Pe Film Market

Functional parity is rapidly attainable. Advances in co‑extrusion, EVOH integration, and vacuum coatings mean many PE‑based structures now match or approach the oxygen and moisture protection historically reserved for PET/Alu laminates — enabling brand owners to pursue recyclable structures at scale.

High Barrier Mdo Pe Film Market

Raw‑material volatility and cost dynamics are a near‑term planning challenge. For example, HDPE market movements in 2025 created pronounced procurement pressure; dynamic price swings demand new hedging, sourcing and downgauging strategies to protect margins during conversion programs.

Market structure supports both consolidation and specialist plays. The sector is neither a pure commodity race nor a closed oligopoly; concentration metrics indicate leading groups have significant presence but there remains room for technological differentiation and regional champions.

Our objective was to produce a document senior teams will use as a decision‑making instrument in 2026. The report combines quantitative forecasting with a trove of executable tools:

Proprietary market sizing and growth trajectory (base 2025; forecast 2026–2032) with scenarios that stress test demand elasticity under different regulatory and raw‑material cost assumptions.

Segmentation frameworks and demand drivers by product architecture, end‑use cluster and regional go‑to‑market archetypes — presented as decision trees and willingness‑to‑pay matrices to inform product prioritization and pricing.

Supplier and technology scorecards that synthesize capacity, technical differentiation (EVOH integration, AlOx/SiOx coatings, extremely high barrier films), sustainability claims, and commercial readiness into a single vendor selection toolkit.

Turnkey playbooks for conversion programs (e.g., BOPP/PET→MDO‑PE), including pilot specifications, barrier testing protocols, downgrade targets, logistics rework flows, and cost‑benefit templates for packaging engineers and procurement.

Regulatory compliance roadmaps that map recycled‑content deadlines to packaging design decisions, with checklists for contact‑sensitive applications and an action plan to defend claims under emerging verification regimes.

Commercial scenarios and an acquisition/partnership heatmap that highlights where vertical integrations (resin + film) or technology partnerships deliver the highest ROI under alternative market conditions.

The market exhibits a mixed structure: a set of multi‑national film groups and specialized regional players competing on technical differentiation, price, and sustainability credentials. Aggregate concentration metrics show that the top three players control a meaningful share of installed capacity, while the top five nearly half the market — a dynamic that favors scale for certain applications (e.g., large‑volume coffee and pet‑food laminates) and nimble innovation for premium or niche segments.

RKW Group — Positioning: Integrated EVOH solutions for mono‑material PE packaging. Strategic implication: premium sustainable replacements for multi‑material structures; of particular interest to brand owners prioritizing fast time‑to‑market with validated recycling claims.

Polifilm — Positioning: Flexible platform films that can act as print substrates or barrier layers. Strategic implication: conversion playbooks that reduce switching friction for converters migrating off PET/OPP while preserving optics and stiffness.

CloudFilm & TOPESOL — Positioning: High‑barrier grades and AlOx‑coated variants from Chinese producers focused on cost‑performance and scale. Strategic implication: competitive supply alternatives for global converters, particularly where price sensitivity is pronounced.

Longdapac, Novel Packaging, Silvalac, ISOFlex — Positioning: Regional champions and specialist providers offering thin‑gauge rigidity, downgauging pathways, and BOPP/PET replacement tech. Strategic implication: attractive targets for strategic procurement or cooperative pilots when entering new geographies or customer segments.

Recent industry events underscore the dynamics: several leading suppliers launched mono‑material EVOH‑integrated MDO‑PE products in 2025, and value chain collaborations (e.g., resin manufacturers partnering with film producers to achieve downgauging in deep‑freeze applications) are accelerating time to commercial scale. These moves signal that the technology transition is now an operating reality, not a future aspiration.

Scenario A — Accelerated Conversion: If brand owner mandates and retail requirements compress timelines, companies must be ready to pilot and qualify mono‑material structures within 9–12 months. Action: prioritize supplier scorecarding, set up dual‑sourcing for barrier grades, and run simultaneous shelf‑life validation to shorten qualification cycles.

Scenario B — Cost Shock and Margin Pressure: If raw‑material volatility intensifies, downgrading and process optimization become essential. Action: model resin substitution and downgauging at SKU level, lock in hedged resin contracts, and explore shared capacity agreements with regional film producers to smooth cost spikes.

Scenario C — Regulation‑Led Differentiation: If recycled‑content and contact‑sensitive mandates tighten faster than expected, early movers with validated mono‑material solutions will capture incremental shelf space. Action: accelerate circularity certification programs, invest in consumer communication assets, and quantify the premium justified by compliance‑driven product placement.

Executives and functional leaders will find the report directly actionable across four decision threads:

Product Roadmaps: Use our technology readiness matrix to prioritize high‑barrier grades for specific SKUs based on barrier requirements, mechanical properties and recyclability risk assessments.

Commercial Strategy: Leverage the pricing‑elasticity and willingness‑to‑pay models to set conversion economics, determine allowable cost increases for sustainable claims, and design trade spend to support rollouts.

Procurement & Supply‑Chain Design: Apply the supplier scorecards and capacity analysis to structure multi‑tier contracts, negotiate downgrading pilots, and design buffer inventories that mitigate resin price swings.

M&A & Partnerships: Use our partner heatmap and valuation sensitivities to prioritize bolt‑on acquisitions, JV opportunities, or co‑development agreements that deliver immediate technical capability or regional access.

The report is intentionally practical: every forecast and qualitative evaluation is paired with templates, checklists and decision gates so executive teams can convert insight into executable projects in Q1–Q2 2026. Clients use the report to define 12‑month pilots, 24‑month commercialization roadmaps and three‑year investment cases that align R&D, procurement and commercial incentives.

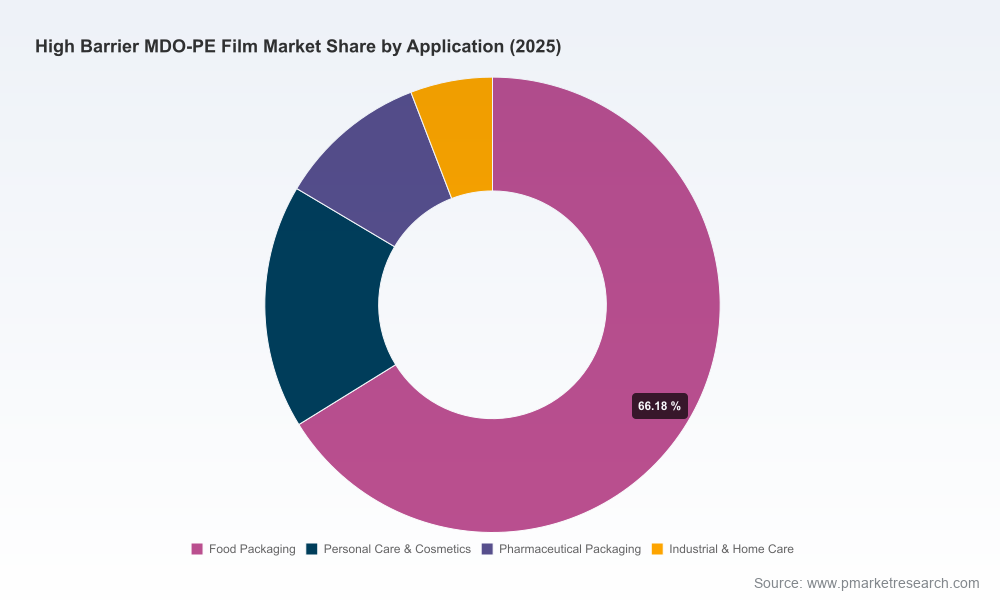

We preserve the granular regional and application splits, detailed vendor scoring and proprietary unit economics inside the full report to ensure that commercial users access the latest validated inputs and sensitive benchmarking in a controlled format. Those specific segmentation tables and supplier‑level metrics are available via the PW Consulting report portal.

For executive teams preparing 2026 capital allocation and product conversion plans, the timing is urgent: market momentum, regulatory deadlines and supplier consolidation create a narrow window in which to pilot, qualify and scale mono‑material high‑barrier solutions. PW Consulting’s High Barrier MDO‑PE Film Market report supplies the forecasting, vendor intelligence, and actionable playbooks required to reduce execution risk and accelerate time to ROI.

Contact PW Consulting to access the full study, download the executive toolkits, or schedule a workshop to translate the findings into a prioritized 12‑month plan tailored to your portfolio and geographies. The full report contains the complete segmentation tables, supplier scorecards, and unit‑level economics that underpin the strategic recommendations summarized here.

For detailed analysis of this topic, please visit the official page:High Barrier Mdo Pe Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com