Global Luxury Dog Apparel Market: Size, Share, and Future Outlook

Other |

2026-05-12 12:17:36

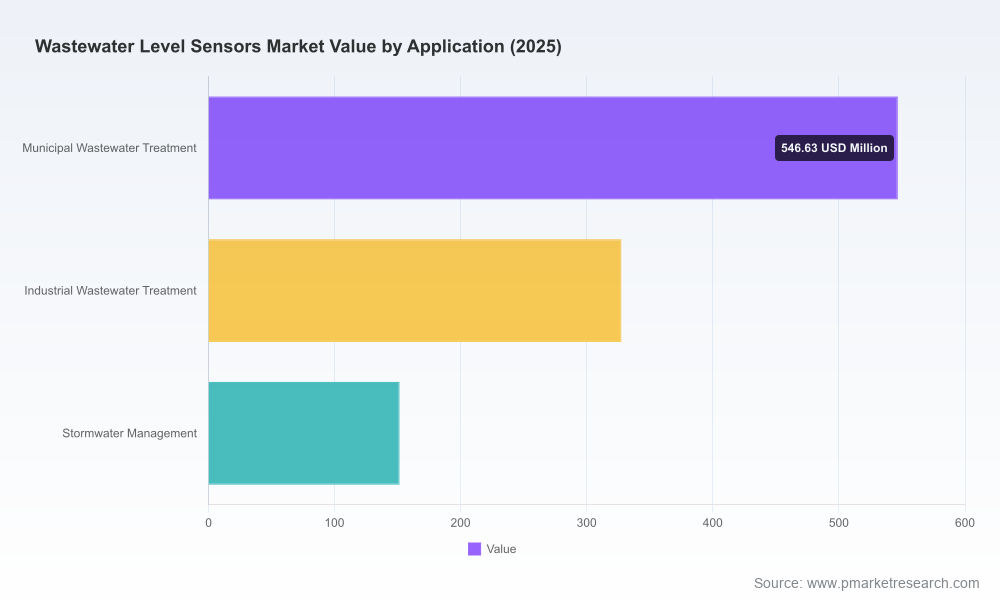

PW Consulting’s latest market research — Wastewater Level Sensors Market: Strategic Outlook 2026–2032 — frames a decisive moment for organizations that design, deploy, operate and finance wastewater infrastructure. Our analysis shows the sector moving from a foundation of steady recovery into a phase of accelerated digitization and regulatory-driven investment. The global market, which PW has tracked from 2020 through a 2025 base year, reached roughly USD 1.03 billion in 2025 and is forecast to approach USD 1.70 billion by 2032, expanding at a compound annual growth rate (CAGR) of approximately 7.45% over the 2026–2032 forecast period. For executives planning capital allocation, product roadmaps or M&A activity in 2026, these directional signals are critical: demand is broadening, technologies are diversifying, and supply-side fragility is beginning to shape strategic choices.

Wastewater Level Sensors Market

Regulatory inflection. Emerging regulatory regimes — including tighter PFAS monitoring in industrial stormwater and heightened compliance requirements for public-sector wastewater programs — are increasing monitoring obligations and shifting cost into third-party instrumentation and monitoring services. These changes raise the floor for baseline monitoring spend and favor reliable, low-maintenance level sensing technologies.

Wastewater Level Sensors Market

Smart infrastructure adoption. Smart-city procurement and digital water programs are accelerating the replacement of legacy float switches with non-contact radar and ultrasonic systems coupled to telemetry and analytics. Operators prioritize sensors that reduce false alarms, lower maintenance outages in wet wells and enable predictive maintenance across pumping networks.

Wastewater Level Sensors Market

Supply-chain pressure. Ongoing semiconductor shortages and volatility in piezoelectric and rare-earth material markets are increasing lead times and OEM production costs for ultrasonic and radar product lines. Procurement and product teams must now balance specification preferences with resilience strategies such as dual-sourcing, inventory hedging and localization of critical components.

Market sizing and trajectory: A consistent historical series (2020–2025) and a granular forecast (2026–2032) that quantify the market’s expansion and the implied addressable opportunity for hardware, service contracts and value-added analytics.

Technology-by-use-case insights: Comparative analysis of ultrasonic, radar, hydrostatic/pressure and hybrid solutions, focusing on performance trade-offs (accuracy, susceptibility to foam/condensation, installation complexity), lifecycle cost and typical failure modes in wastewater environments.

Procurement & deployment playbooks: Practical checklists and RFx language for municipal and industrial buyers, deployment-ready testing protocols for wet wells and clarifiers, and performance acceptance criteria to reduce “shrinkage” between pilot and full-scale rollouts.

Supply-chain risk maps and mitigation strategies: Line-item analysis of critical component risks, supplier concentration for semiconductors and piezoelectric elements, plus scenario-based contingency plans for lead-time shocks.

Regulatory impact modeling: Forward-looking scenarios that translate proposed and likely regulation changes into incremental monitoring spend and compliance timelines across municipal and industrial segments.

Vendor benchmarking and go-to-market playbook: Proprietary scoring across technology, service capability, geographic reach and aftermarket economics designed to inform vendor selection, partnership decisions and potential acquisition targets.

Case studies and ROI frameworks: Real-world deployments that quantify downtime reduction, maintenance labor savings and operational benefits when moving from legacy electromechanical sensors to modern non-contact systems paired with analytics.

The wastewater level sensor market is moderately fragmented. A mix of large industrial conglomerates, specialist manufacturers and regional players compete across product families and go-to-market models. Major international vendors remain influential because of scale, established service networks and the ability to bundle level sensing into broader water instrumentation portfolios. At the same time, focused specialists continue to capture share through technology depth and targeted product lines for wastewater challenges.

Xylem Inc. — Known for integrating level sensors into broader measurement and control solutions for water and wastewater infrastructure. Xylem’s strength is its systems approach: coupling sensors, controls and aftermarket service to reduce total cost of ownership for municipal and utility customers.

Endress+Hauser Group — Offers a broad portfolio including ultrasonic, radar and hydrostatic transmitters tailored for clarifiers and pumping stations. The company’s instrument reliability and global service footprint make it a preferred choice for industrial and municipal operators seeking predictable lifecycle performance.

VEGA Grieshaber KG — A technology leader in high-frequency radar (80 GHz) and submersible pressure transmitters. VEGA’s focus on severe-environment applications, such as sewage lift stations and stormwater basins, positions it well in markets prioritizing non-contact measurement to mitigate maintenance risks.

KROHNE Messtechnik GmbH — Competitive in non-contact radar for pumping stations and treatment plants. KROHNE’s solutions are commonly specified where electromagnetic immunity and long-range non-contact performance are required.

Flowline Inc. & Pulsar Measurement — U.S. and U.K.-based specialists respectively, these firms focus on tailored ultrasonic and radar products for municipal wastewater applications such as wet wells and foaming tanks. Their agility in product customization and competitive pricing make them attractive to local operators and integrators.

SJE-Rhombus, ABB, Siemens, APG Sensors — These vendors round out a competitive set where diverse channel strategies (OEM partnerships, distributorships, direct municipal sales) and product breadth determine win rates in tendered contracts.

From a strategic perspective, incumbents leverage scale and aftermarket services to protect margins, while specialist vendors compete on innovation, rapid customization and localized support. New entrants should evaluate whether to prioritize technology differentiation (e.g., advanced radar, AI-enabled signal processing) or channel depth (service contracts, municipal relationships).

Prioritize supplier resilience over lowest-cost components. Given component volatility, lock-in dual-source agreements for critical semiconductors and piezoelectric materials, increase safety stock for long-lead items, and consider near-shore partners to reduce transit risk.

Bundle hardware with analytics-enabled services. Operators are willing to pay premiums for reduced unplanned maintenance and better asset visibility. Vendors that offer subscription-based analytics and guaranteed uptime can capture higher lifetime revenue per sensor.

Instrument procurement to regulatory timelines. Map installation waves against compliance deadlines (e.g., emerging PFAS monitoring rules and DoD/municipal maintenance mandates) to avoid last-minute procurement spikes that inflate costs and strain supply.

Invest in pilot-to-scale playbooks. Reduce deployment risk by standardizing acceptance tests, environmental validation and integration templates for SCADA/IoT platforms. These reduce the “pilot purgatory” that slows municipal rollouts.

Explore selective M&A and partnerships. For larger players, acquiring specialist sensor firms can accelerate access to niche technologies and municipal accounts. For smaller vendors, partnerships with system integrators and analytics firms improve market access and recurring revenue potential.

Raw material and subcomponent supply shocks. Monitor lead times and price volatility for piezoelectric ceramics, rare-earth magnets and key semiconductor families. These are the leading indicators of product cost pressure.

Regulatory shifts and enforcement timelines. Track federal and state rulemaking for contaminant monitoring and municipal performance measures; these will materially affect short-term procurement cycles.

Technology substitution risks. Non-contact radar and ultrasonic technologies are improving rapidly. Vendors that fail to invest in firmware signal processing and remote diagnostics risk obsolescence in tendered procurements.

Our report synthesizes granular supplier intelligence, technology roadmaps and regulatory scenario models into a decision-ready playbook for 2026 planning. Clients tell us they value the report not as a static dataset but as a practical toolkit: procurement language they can copy into tenders, deployment acceptance criteria that reduce implementation dispute, and supplier scorecards that accelerate vendor selection.

We follow industry events and programmatic shifts — including the major trade shows and conferences where suppliers reveal incremental product innovations and municipal procurement trends — to ensure our recommendations reflect current market behavior and near-term developments.

PW Consulting’s Wastewater Level Sensors Market: Strategic Outlook 2026–2032 is designed to be operationally useful in boardroom and field-planning contexts. To preserve competitive advantage and ensure decision-makers receive the full analytical depth (including regional, type and application splits, detailed vendor scorecards and downloadable procurement templates), the full dataset and supporting models are available via the PW Consulting report portal. For a briefing tailored to your organization’s position — whether you are an OEM, systems integrator, municipal utility or investor — contact our research team to schedule a personalized strategy session.

Access the full report and brief by visiting the PW Consulting website or contacting our industry practice leads for a direct consultation.

For detailed analysis of this topic, please visit the official page:Wastewater Level Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com