PW Consulting: 5‑HMF Market to Reach USD 80 Million by 2032, Backed by a 3.8% CAGR

Other |

2026-06-29 17:32:33

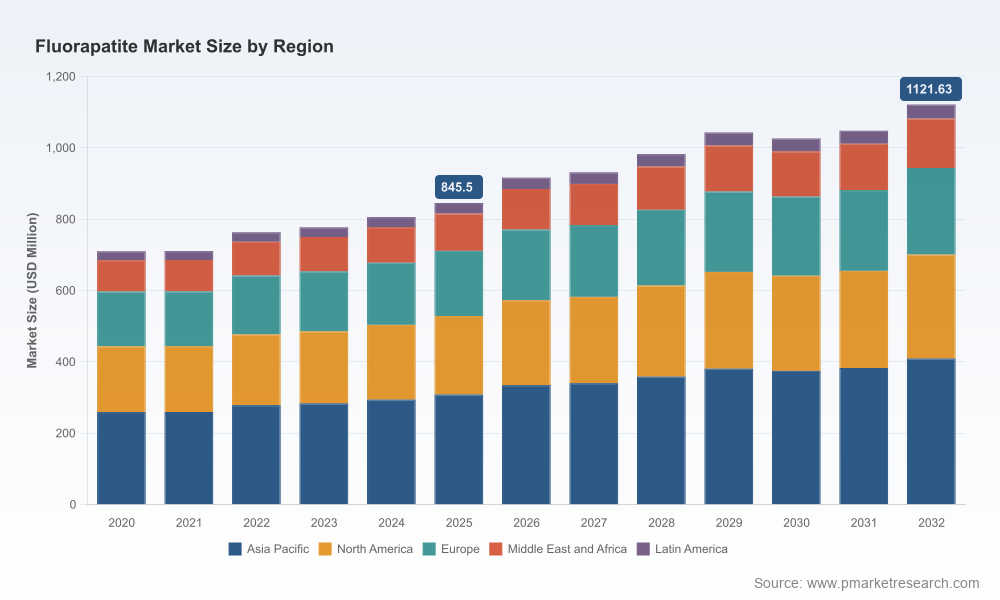

PW Consulting’s latest Fluorapatite Market report provides actionable intelligence designed to inform high-stakes corporate decisions in 2026. Our analysis projects the global fluorapatite market to grow from an estimated USD 845.5 million in 2025 to roughly USD 916.7 million in 2026, and continue on a steady trajectory to exceed USD 1.12 billion by the end of the 2026–2032 forecast window. This path corresponds to a compound annual growth rate (CAGR) of approximately 4.12% over the forecast period.

Fluorapatite Market

Those headline figures mask a market undergoing structural evolution—driven by feedstock availability, fertilizer demand patterns, industrial chemistry needs, and nascent biomedical applications—each of which carries distinct strategic consequences for upstream miners, integrated fertilizer producers, specialty material manufacturers and end-users pursuing differentiation.

Fluorapatite Market

Fluorapatite (Ca5(PO4)3F) continues to anchor the phosphate value chain as both the dominant form of phosphate rock and an industrial feedstock with diverse end-uses. Macroeconomic drivers supporting the medium-term expansion include persistent fertilizer demand in food security portfolios, incremental uptake in industrial phosphate-derivatives, and the emergence of high-value biomedical and dental materials. Supply-side developments—new mine approvals, reserve development, and novel manufacturing routes for bioactive forms—are reducing near-term supply constraints in some producing regions while increasing competitiveness for players that control processing capacity.

Fluorapatite Market

Policy, environment and trade factors are equally influential. Permitting decisions and environmental scrutiny around water and habitat management for phosphate mining now factor materially into project risk assessments. Meanwhile, capital discipline among major producers and modest concentration at the top of the market have created windows for targeted M&A and strategic partnerships.

Upstream supply remains the single most critical determinant of market outcomes. U.S. marketable phosphate rock production—primarily fluorapatite—continued to be significant in recent years, supporting domestic wet-process phosphoric acid production and downstream fertilizer supply. New mine approvals and reserve replacement initiatives in 2025 have partially alleviated immediate domestic pressure points.

Concurrently, technology and product innovation are reshaping demand composition. Recent publicized developments include a successful scale-up and quality assurance milestone for bioactive fluorapatite production (October 2025), representing a potential pathway to commercial volumes for high-margin biomedical-grade material. Such advances create a bifurcated opportunity set: commodity-grade fluorapatite used in fertilizers and industrial chemistry, and specialty fluorapatite for biomedical/dental and other high-value uses.

Strategic implications for supply risk:

The fluorapatite value chain is populated by a mix of large integrated phosphate miners and fertilizer groups, national champions and specialized mineral suppliers. Several industry leaders—each with substantial upstream operations and end-market integration—shape pricing and capacity deployment dynamics. PW Consulting’s market concentration analysis indicates that the top three firms account for a meaningful share of the market, while the top five approach a clear majority, underscoring both concentration and room for strategic plays by midsized and specialty players.

Major upstream and integrated players include (representative, non-exhaustive):

What this concentration means for market entrants and incumbents:

Corporates, investors and public-sector actors planning capital allocation for 2026 must balance supply security, margin management and regulatory risk. PW Consulting highlights five priority actions that should underpin 2026 strategies:

Our report is intentionally designed as a decision-grade toolkit for 2026. It combines rigorous market modeling with practitioner-focused outputs to guide capital allocation, commercial strategy, and risk mitigation. Key deliverables include:

Importantly, the report contains granular segmentation, regional breakdowns and application-level forecasts that underpin our headline numbers. These granular datasets are not reproduced in this release; PW Consulting has curated them to support executable strategies while preserving the value of proprietary modeling.

For organizations finalizing budgets and strategic plans in 2026, the choice is between passive exposure to commodity cycles or active repositioning to capture value from specialty demand and improving supply fundamentals. Our analysis shows that modest, targeted investments—combined with contractual protections and selective vertical integration—can materially improve risk-adjusted returns.

PW Consulting’s Fluorapatite Market report is structured to move decision-makers from insight to action: from identifying which projects to accelerate or defer, to defining partnership structures that secure feedstock without onerous capital commitment, to constructing premium product strategies for biomedical and advanced industrial markets. For access to the full dataset, company-level profiles, and downloadable modeling tools, request the full report and supplementary materials through PW Consulting’s market portal.

For detailed analysis of this topic, please visit the official page:Fluorapatite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com