Global Security Robots Market Analysis by Type, Application, and Region

Technology |

2026-06-08 17:58:39

As organizations confront accelerating regulatory complexity, relentless breach rates, and the operational demands of AI-enabled governance, the Legal Risk and Compliance Solution market has moved from niche support function to mission-critical strategic asset. PW Consulting’s latest market research — Legal Risk And Compliance Solution Market — synthesizes quantitative trajectory and qualitative intelligence to inform high-stakes decisions for 2026. The report documents a market that reached roughly USD 18.5 billion in 2025 and, on a 12.8% compound annual growth path, is forecast to surpass the USD 42.9 billion threshold by 2032. This growth reflects a combination of regulatory pressure, enterprise digital transformation, and vendor innovation anchored in AI and platform convergence.

Legal Risk And Compliance Solution Market

Regulation as a growth driver: New and evolving rules — from national privacy regimes to sector-specific mandates — are creating recurring compliance obligations that are most efficiently managed through integrated, automated platforms rather than ad hoc point solutions.

Legal Risk And Compliance Solution Market

Scale and resilience: Buyers must assess technology choices through a resilience lens: data residency and energy efficiency requirements for data centers, supply-chain transparency, and forensic readiness are now procurement criteria.

Legal Risk And Compliance Solution Market

Economic calculus: With a multi-year double-digit CAGR, the market presents both opportunity and risk for incumbent vendors and new entrants. Mean re-investment in product R&D and partnerships will determine winners; for buyers, the question is whether to standardize on broad platforms or compose best-of-breed stacks.

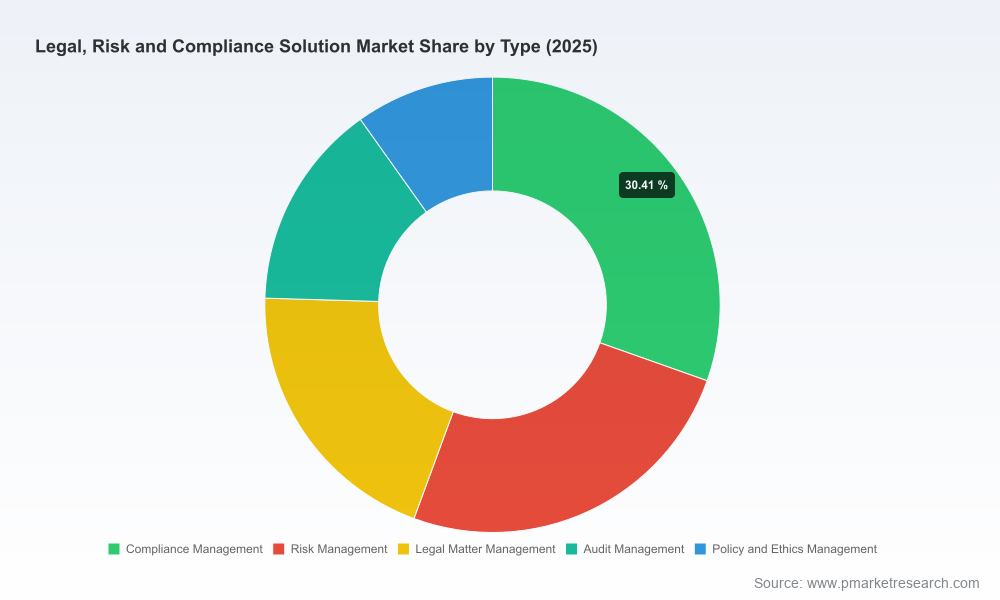

The market exhibits a moderate level of concentration: the top three vendors collectively command approximately 22.5% of industry revenue, while the top five account for roughly 35.4%. That profile signals meaningful scale advantages for a handful of players — especially in enterprise sales, global regulatory coverage, and deep integrations — while leaving ample space for specialists and regional players to capture niche or adjacent demand.

Notable trends shaping competitive dynamics include:

AI-first product strategies: Vendors are embedding machine learning and LLM-based capabilities to automate regulatory change capture, contract review, and monitoring of risk signals.

Platform convergence: GRC, privacy, legal matter management, audit, and ESG/compliance offerings are migrating toward unified platforms or tightly integrated ecosystems to reduce friction and improve traceability.

Service-layer differentiation: Professional services, regulatory expertise, and localized compliance content remain key value levers—particularly for multinational clients navigating fragmented regulatory regimes.

This report is designed as an operational toolkit for 2026 planning cycles. It combines forward-looking market sizing and CAGR trajectory with hands-on, actionable modules intended for procurement, legal, risk, and CIO offices. Core deliverables include:

Board-ready strategic briefings that translate market dynamics into investment theses for platform consolidation, insourcing vs. outsourcing decisions, and cross-functional governance operating models.

Vendor selection frameworks: weighted scorecards, integration checklists (API, data model, audit trail continuity), and vendor risk assessment templates enabling objective comparisons in RFP/RFI processes.

Implementation playbooks: phased deployment plans (prioritizing high-risk use cases), change-management templates, KPI dashboards for compliance performance, and runbooks for incident response and regulatory reporting.

Technology and cost benchmarking: TCO modeling templates, scenario-based ROI calculators, and sensitivity analyses that account for license costs, cloud consumption, implementation, and ongoing professional services.

Regulatory watch and content packs: curated rule summaries, mapping matrices linking obligations to control frameworks, and gap-analysis tools that accelerate remediation planning.

We intentionally refrain from publishing full segment-level breakdowns in this announcement; the report preserves proprietary segmentation intelligence to deliver differentiation for subscribing leaders.

The ecosystem spans global incumbents anchoring enterprise-wide suites and highly focused innovators targeting privacy, vendor risk, or automated assurance. Key provider archetypes we analyze in the report include:

Integrated information and content leaders (e.g., Thomson Reuters, Wolters Kluwer) — combining deep regulatory content and legal research with workflow tooling to serve corporate legal departments and regulated industries.

Platform and infrastructure players (e.g., IBM, Oracle, SAP) — offering GRC suites and enterprise-grade integration with ERP, identity, and IAM systems for large-scale deployments.

Modern cloud-native GRC specialists (e.g., ServiceNow, MetricStream, Archer) — focused on orchestration of governance, risk, and compliance workflows across IT and business functions.

Privacy and security-centric entrants (e.g., OneTrust, Vanta) — specializing in data protection, privacy program automation, and security certification workflows for growth-stage to mid-market firms.

Reporting and assurance platforms (e.g., Workiva, Diligent) — linking financial and ESG reporting to compliance controls and board governance processes.

No-code/low-code orchestration players (e.g., LogicGate) — enabling rapid customization for risk models and case management without heavy engineering lift.

Our competitive profiles dissect go-to-market models, IP and content moats, partner ecosystems, and likely consolidation vectors. We assess each vendor’s strategic strengths and gaps so procurement and strategy teams can make defensible choices aligned to enterprise risk appetites.

OneTrust’s Winter 2026 release expands AI-powered governance capabilities, underscoring how privacy and governance vendors are accelerating automation of manual reviews and embedding governance into innovation cycles.

Wolters Kluwer’s late-2025 launch of an Expert AI regulatory intelligence product highlights content-plus-AI as a high-bar competitive play, especially for financial services clients requiring curated regulatory feeds.

Specialist product launches — including improved machine-learning engines for reducing false positives in trade and denied-party screening — point to continuing investment in niche accuracy and operational efficiency.

Collectively, these moves signal a market where data quality, model explainability, and regulatory-grade auditability will define commercial viability.

Several regulatory and operational realities are shaping buyer requirements:

Enforcement and recordkeeping: The U.S. Department of Justice’s Bulk Data Rule (effective 2025) and staggered enforcement timelines have raised baseline cybersecurity and recordkeeping obligations for sensitive transactions.

Fragmented privacy landscape: By early 2026, roughly twenty U.S. states have implemented comprehensive privacy laws, increasing the compliance burden for multi-state operators and elevating the value of centralized privacy programs.

Infrastructure reporting: Revisions to EU energy efficiency directives now require operational metrics from data centers that host compliance platforms — a new procurement filter for sustainability-conscious buyers.

Rising breach notifications and fines: Continued GDPR-style enforcement and a notable year-over-year uptick in incident reporting have made automated detection, documentation, and reporting capabilities non-negotiable.

Budget composition: Privacy and compliance programs in 2026 are allocating significant shares of budgets to cloud and license costs, personnel, and advisory services — a triage that influences contract terms and delivery models.

Board-level alignment: Use our executive summaries to brief your board on market dynamics, vendor risk, and an investment timeline that balances quick wins with architectural resilience.

Procurement acceleration: Apply the report’s vendor scorecards and integration checklists to shorten procurement cycles while preserving negotiation leverage on SLAs, data residency, and audit rights.

Implementation risk reduction: Adopt the phased deployment playbooks to prioritize high-exposure use cases (e.g., privacy incident response, sanctions screening, regulatory reporting) and defer low-risk integrations.

Vendor partnership roadmap: Use our ecosystem analysis to identify complementary partners for content, identity, and security services that lower total cost and speed time-to-compliance.

This press release provides a strategic preview of the insights and operational tools available in PW Consulting’s full Legal Risk And Compliance Solution Market report. For legal teams, CIOs, risk officers, and procurement leads planning 2026 budgets and transformation programs, the full report contains proprietary segmentation intelligence, detailed vendor matrices, customizable procurement artifacts, and scenario-based financial models not published here. To access the complete dataset, segmentation breakouts, and subscription options, please visit our report landing page.

PW Consulting stands ready to translate these market insights into a bespoke roadmap for your organization — from vendor shortlists to governance design and implementation oversight. In an era where compliance capability is strategic capability, timely intelligence and disciplined execution will determine who leads and who follows.

For detailed analysis of this topic, please visit the official page:Legal Risk And Compliance Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com