PFSA Ionomer Market — Strategic Outlook for 2026 Decision-Makers

PW Consulting’s Pfsa Ionomer Market report (base year 2025; forecast period 2026–2032) synthesizes commercial, technical, and regulatory intelligence to equip executives with the evidence and playbooks needed to make high‑stakes decisions in 2026. The market is on a steep growth trajectory (CAGR 20.38%), growing from a 2025 baseline of USD 1,254.4 Million to a multi-billion dollar opportunity by 2032 (USD 4,595.35 Million). This release primes leaders on where to commit capital, how to shore up supply chains, and which technology and policy inflections will determine winners — while intentionally withholding granular segment-level allocations to encourage engagement with the full report for transaction‑grade data.

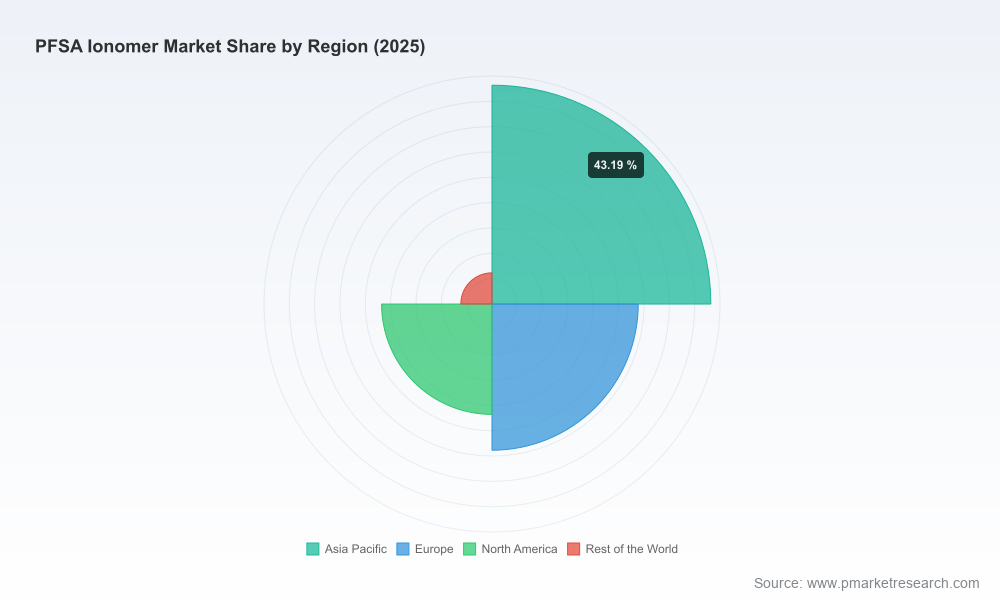

Pfsa Ionomer Market

Why this report matters for 2026

- Investment prioritization: Rapid top‑line expansion and concentrated supplier positions make timing and partner selection critical for capex and M&A. Our analysis translates market expansion into demand windows and capital intensity profiles for membrane and dispersion capacity.

- Supply‑chain resilience: Upstream feedstock dynamics and regulatory pressure on PFAS create supply risks that procurement and operations teams must mitigate now to avoid qualification delays in 2026.

- Commercial differentiation: Product form (dispersion vs. resin), performance for PEM fuel cells and electrolyzers, and end‑of‑life strategies will define premium carriers of margin. The report maps these commercial pathways and go‑to‑market timelines.

- Regulatory and reputation risk management: With PFAS governance intensifying in core markets, companies need an actionable regulatory playbook that aligns R&D, manufacturing, and sustainability communications.

Key market dynamics shaping 2026 decisions

- Accelerating demand driven by energy transition: Hydrogen-related applications and electrified mobility continue to be primary growth engines. The market’s ~20% CAGR reflects both volume growth and a shift toward higher‑value formulations and application‑specific grades.

- Upstream material concentration and feedstock constraints: Tetrafluoroethylene (TFE) is the principal monomer for PFSA synthesis; the global TFE market itself registers material scale and volatility (recent estimates put the TFE market in the low‑billion USD range). Supply disruptions or price swings in fluorinated feedstocks have a first‑order impact on PFSA production economics.

- Regulatory pressure reshaping supply chains: Ongoing PFAS regulation in Europe and North America, together with strategic exits by legacy suppliers, are forcing buyers to reassess supplier eligibility, compliance pipelines, and material stewardship programs.

- High supplier concentration: The market exhibits meaningful concentration among a few established producers. That concentration amplifies counterparty risk but also creates arbitrage opportunities for new entrants and vertically integrated incumbents.

Competitive landscape — what to watch in 2026

- Incumbent leaders and strategic posture: Longstanding technology leaders continue to invest in performance and lifecycle solutions. Recent company developments — for example, leading firms publishing sustainability research, winning government grants for hydrogen tech, and reporting strong segment performance — indicate a strategic pivot toward lifecycle management and policy‑aligned product portfolios.

- Product and process differentiation: Innovations in short‑side‑chain chemistries, dispersion technologies, and membrane architecture are changing qualification cycles. Buyers should expect faster iteration in dispersion grades and tighter integration between ionomer suppliers and stack/system OEMs.

- Geopolitical and regional supply strategies: Suppliers are pursuing capacity placements and partnerships to secure regional demand, respond to regulatory fragmentation, and shorten qualification and logistics lead times. Expect more tolling, joint ventures, and licensing deals in 2026 as a way to scale quickly without full greenfield exposure.

- New entrants and consolidation potential: High growth and concentrated returns will attract private and strategic investors; however, incumbent intellectual property, certifications, and scale create high entry barriers. The coming 18 months are likely to see targeted tuck‑ins and strategic alliances rather than broad-based consolidation.

Operational playbook for 2026

- Supply assurance and procurement: Implement multi‑tier sourcing strategies, prioritize suppliers with validated compliance and recycling pathways, and negotiate capacity reservation mechanisms (take‑or‑pay, options) to secure feedstock during ramp phases.

- Quality and qualification timelines: Align internal product roadmaps with OEM qualification cycles. Expect 9–18 month qualification windows for new ionomer grades intended for fuel cell stacks and electrolyzers; build parallel validation tracks to de‑risk launch timing.

- Manufacturing and scale planning: For players pursuing integration, consider modular capacity expansions and tolling arrangements to reduce capital intensity and shorten time to market. Technical due diligence should include feedstock sourcing, fluoropolymer processing expertise, and environmental permitting timelines under tightening PFAS frameworks.

- R&D and materials strategy: Prioritize formulations that reduce lifecycle emissions, enable easier recycling, or lower reliance on constrained feedstocks. Invest in accelerated aging and contamination resistance testing to shorten qualification cycles with OEMs.

Commercial and financial implications

- Pricing and margin dynamics: Rapid demand growth creates near‑term pricing power, but feedstock volatility and regulatory compliance costs will pressure margins for less differentiated suppliers. Develop scenario models that stress feedstock cost, regulatory compliance cost, and demand growth to test resilience.

- M&A and partnership criteria: Targets that provide feedstock access, IP in membrane architectures, or regional manufacturing footprints should be prioritized. The right deal structure often blends equity with offtake and technology licensing to accelerate commercialization while controlling cash exposure.

- Investment timing: The market’s structural growth argues for staged investments linked to demand milestones. Early movers who secure long‑term supply agreements and reciprocal R&D commitments will capture the premium in the value chain.

What the report delivers (practical contents)

- Robust market sizing and demand model (base year 2025; forecasts 2026–2032) with scenario sensitivity to policy, technology, and feedstock shocks.

- Topical supplier dossiers and strategic scorecards covering technology, capacity, commercial posture, and ESG/compliance readiness for leading producers.

- Supply‑chain heatmaps and procurement playbooks highlighting critical nodes and mitigation levers for feedstock and manufacturing risk.

- Commercial templates: TCO and TEA models for target applications (fuel cells, electrolyzers, and industrial electrolysis), go‑to‑market route maps, and product qualification timelines.

- Policy and regulatory mapping with recommended compliance pathways and stakeholder engagement strategies relevant to PFAS governance.

- Investment decision framework including valuation sensitivities, integration checklists, and recommended deal structures for 2026 transactions.

- Recycling and end‑of‑life strategy options coupled with practical pilots and cost estimates for closed‑loop programs.

How to use these insights — immediate next steps

- For CEOs and corporate development: Prioritize targets that de‑risk feedstock access or deliver immediate route-to-market for dispersion and electrode-grade products.

- For procurement and operations: Execute supplier risk audits across the fluoropolymer value chain and initiate capacity reservation conversations with top‑tier suppliers.

- For R&D leaders: Fast‑track formulations that balance performance with recyclability and regulatory defensibility; align test programs with expected OEM qualification cycles for 2026 launches.

- For sustainability and compliance teams: Build a PFAS governance playbook and engage upstream partners on feedstock traceability and end‑of‑life responsibility models.

PW Consulting’s Pfsa Ionomer Market report is structured to inform immediate 2026 decisions while reserving transaction‑grade segment detail for controlled access. If your strategic agenda includes target selection, supply‑chain reconfiguration, or technology investment in the coming 12 months, this report will shorten time to insight and reduce execution risk.

Pfsa Ionomer Market

To access the complete analysis, proprietary models, and supplier scorecards — including the withheld granular segment splits and downloadable financial templates — please consult the Pfsa Ionomer Market report page or contact PW Consulting’s advisory team for a briefing and data license.

Pfsa Ionomer Market

For detailed analysis of this topic, please visit the official page:Pfsa Ionomer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com