How Is Motorcycle Market Expanding with Urban Mobility and EV Trends?

Networking |

2026-05-11 06:53:01

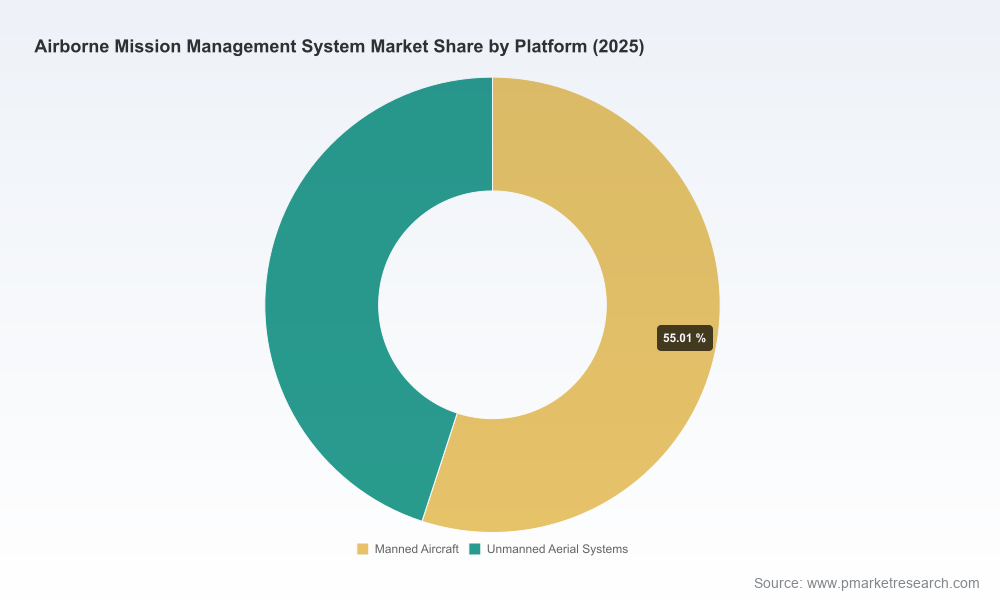

PW Consulting’s latest market research on Airborne Mission Management Systems (AMMS) synthesizes seven years of market movement and a seven-year forward view to equip defense and aerospace executives with pragmatic intelligence for 2026 decision cycles. Built on a 2025 base year and a historical window spanning 2020–2025, the study projects the market through 2032. Our analysis shows a steady expansion at a compound annual growth rate (CAGR) of 6.15% over the 2026–2032 forecast period, reflecting an evolution driven by platform modernization, sensor proliferation, and systems-of-systems integration. Total addressable market metrics in our baseline indicate growth from roughly USD 2.40 billion in 2025 to about USD 3.65 billion by 2032, underscoring material opportunity for program sponsors, prime contractors, and technology suppliers.

Airborne Mission Management System Market

Timing decisions around procurement and program starts are being reshaped by predictable market expansion and by bursts of tactical spending linked to modernizations and ISR recapitalization. Our forecast anchors your choices to a multi-year cadence and clarifies when to accelerate vs. defer investment.

Airborne Mission Management System Market

Technology risk is now as consequential as geopolitical imperative. The report unpacks where open architectures (MOSA), rugged low‑SWaP compute, and certified software toolchains intersect with acquisition policy — telling program managers which technical bets minimize integration cost and certification delay.

Airborne Mission Management System Market

Supply-chain and consolidation dynamics are influencing supplier strategy. The market remains moderately concentrated (CR3 ≈ 48.5%; CR5 ≈ 62.3%), which affects negotiation leverage, partnership choices, and M&A rationale. Our analysis converts these concentration numbers into actionable supplier engagement guidance.

From 2020 onward, the AMMS market has progressed through two distinct phases: an initial recovery and capability refresh phase (2020–2023) followed by accelerated platform modernizations and growing integration complexity (2024–2025). By anchoring the 2025 base year and projecting through 2032, our model captures the transition from discrete upgrades toward program-of-record modernization and new-platform integration, which collectively support the 6.15% CAGR we forecast for 2026–2032.

The growth drivers are multi-vector: modernization of maritime patrol and manned ISR fleets, expansion of persistent unmanned systems, increased demand for multi-sensor data fusion, and growing needs for integrated mission computing that supports edge analytics and resilient communications. Headwinds include certification friction, SWaP constraints for certain platforms, and the uneven pace at which defense buyers embrace fully modular approaches. The net effect is a market that is large enough to sustain tier‑1 incumbents and fast-moving specialist entrants, while still offering entry points for focused technologies and regional integrators.

Decision frameworks that link program intent to procurement levers: timelines, architecture choices (closed vs. MOSA), certification sequencing, and cost-of-ownership estimates keyed to mission profiles.

Vendor assessment methodology and a calibrated vendor scorecard covering technical fit, systems-integration capability, certification pedigree, and sustainment posture. (Note: detailed scorecards and full quantitative vendor rankings are available in the full report.)

Risk and mitigation playbooks for integration, with practical checklists for ensuring RTCA DO‑254/DO‑178C compliance, ARP4754A alignment for system development, and traceability strategies that reduce schedule slip during certification.

Procurement and contracting templates tailored to different acquisition paths — from rapid prototyping and OTAs to competitive fixed-price modernizations — and guidance on structuring IDIQ/indefinite-delivery vehicle language to preserve upgradeability.

Financial and program scenario analyses with sensitivity testing around platform mix, sensor payload growth, and software-centric value capture to support capital planning and R&D prioritization.

Integration and sustainment roadmaps that translate technical requirements into support concepts, obsolescence management, and COTS/NDI governance for long-lifecycle airborne programs.

The sector combines global primes with focused specialists. Established defense suppliers continue to underpin large platform programs, while nimble innovators are driving capability shifts in sensor fusion, mission processing, and tailored ISR suites. Notable firms profiled in our study include multinational systems integrators and specialized avionics and ISR vendors whose strategic moves offer insight into future industry direction.

Curtiss‑Wright Defense Solutions — recognized for scalable mission processors and rugged MOSA-aligned computing, with recent task awards tied to tactical UAV mission processors that underscore the continued market for proven airborne compute hardware.

General Dynamics Mission Systems (Canada) — a systems integrator competent across fixed- and rotary-wing modernization workstreams, demonstrating the steady demand for whole‑platform modernization and retained-life upgrades.

Saab AB — offering flexible non-flight-critical C2 and mission management suites across maritime and airborne platforms, showcasing a directional trend toward configurable mission software that supports multiple mission sets.

Ondas Holdings (through its acquisition of a specialized ISR systems provider) — acquisition activity indicates acquisition as a fast route to capability breadth in airborne ISR and mission management domains.

Leonardo, Honeywell Aerospace, and Thales Group — global suppliers combining avionics, mission systems, and platform integration capacity; their roadmaps highlight emphasis on crew situational awareness, multi-workstation environments, and integrated sensor‑to‑C2 flows.

Recent strategic moves captured in our research—such as program awards for mission processors, national modernization contracts, and targeted acquisitions—illustrate how primes and specialists are locking down capability blocks, expanding platform footprints, and shoring up product portfolios that address sensor fusion, persistent ISR, and scalable mission computing.

Certification continues to be a determinative program risk. Compliance with DO‑254 for airborne electronic hardware and DO‑178C for software remains mandatory where applicable to safety or flight‑critical elements. ARP4754A process alignment and formal requirements traceability are non-negotiable for programs that expect to be accepted into national fleets or civil-adjacent environments. Our report includes a practical end-to-end certification timeline template and a set of mitigations — from model-based engineering adoption to partitioned architectures — that reduce time-to-field for complex airborne mission systems.

On the technical side, low‑SWaP, rugged computing for mission processors remains a hard constraint. The combination of processing demand for real-time data fusion and the physical constraints of manned and unmanned airframes necessitates early co-design between payload architects and systems engineers. MOSA adoption, while mission enabling, introduces governance and integration friction that must be managed through interface control documents, common data models, and supplier onboarding processes.

Prioritize MOSA for all new procurements, but budget the first 12–18 months for architectural governance and integration testing—short-term cost is an investment that reduces long-term lock-in and sustainment expense.

Embed certification strategy into the program prime contract: require supplier DO‑178C/DO‑254 readiness evidence, and use staged acceptance criteria to decouple mission software delivery from platform certification milestones.

Focus R&D budgets on edge analytics that reduce link load and enable distributed mission processing—this will be a differentiator for both manned and unmanned mission suites.

Use market concentration metrics to shape competition strategy: leverage dual-sourcing where feasible for critical compute modules, and target partnerships or divestitures in regions where national preference or industrial policy drives buying behavior.

Prepare procurement templates and TCO models that explicitly capture sustainment, upgrade, and cyber-hardening costs; our report provides ready-to-use templates and sensitivity runs to accelerate proposal and budgeting cycles.

Procurement officers, systems architects, corporate strategy teams, and M&A advisors will find different entry points in this research. The report is organized so technical leads can jump to certification and integration playbooks, finance teams to scenario-based cash-flow models, and strategy teams to competitive intelligence and M&A screening. For readers seeking immediate program-level guidance, our executive checklists and procurement templates provide a fast path from insight to action.

The AMMS market in 2026 sits at the intersection of predictable volume growth and disruptive technology adoption. The macro trajectory is clear: steady expansion at a mid-single-digit CAGR through 2032, concentrated supplier dynamics, and durable technical constraints around SWaP and certification. What remains strategic—and is the core value of PW Consulting’s work—is converting these trends into executable program choices that reduce risk and capture capability ahead of peers.

To access our full suite of segmentation tables, regional and application breakdowns, vendor scorecards, and downloadable templates that underlie the findings summarized here, consult the full report on PW Consulting’s website. The substantive appendices and granular, source-linked datasets are available there for teams preparing 2026 budgets, RFPs, and program roadmaps.

For detailed analysis of this topic, please visit the official page:Airborne Mission Management System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com