What Makes Skims Shapewear Different

Health |

2026-06-29 11:43:40

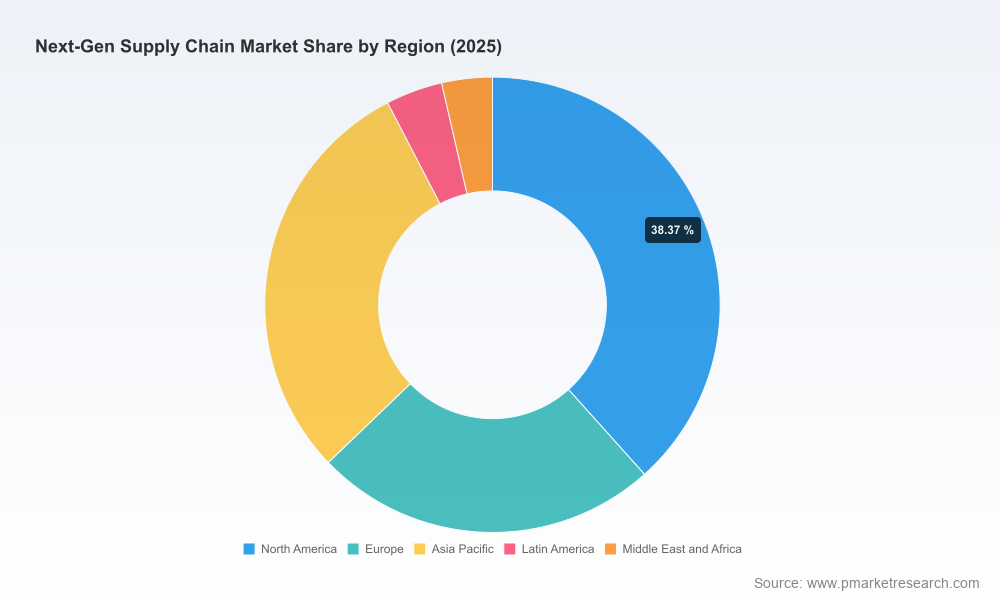

PW Consulting’s new Next Gen Supply Chain Market report (base year 2025; forecast 2026–2032) arrives at a critical inflection point for corporate supply chain strategy. The market reached an estimated USD 62,450 Million in 2025 and, driven by accelerating adoption of AI, robotics, cloud orchestration and networked platforms, is projected to grow at an 11.4% CAGR through 2032 to roughly USD 133,000 Million. For executives preparing budgets, capital plans and transformation roadmaps for 2026, this report provides the evidence-based guidance required to convert momentum into measurable advantage.

Next Gen Supply Chain Market

Regulation is changing the definition of a product. New regulatory frameworks that treat physical goods as data-rich assets are forcing companies to reconcile product data across multi-tier supply networks — a shift that turns traceability into a strategic capability rather than a compliance checkbox.

Next Gen Supply Chain Market

AI is moving from proof-of-concept to infrastructure. The growth of AI workloads has material implications for data center power, cooling and hardware strategy. Organizations that plan for higher rack power densities and the accompanying operational costs will avoid late-stage infrastructure squeezes that can derail digital twin and analytics rollouts.

Next Gen Supply Chain Market

Geopolitical volatility is resetting network design. North–South and East–West trade dynamics are increasing the strategic value of multi-regional footprints, nearshoring and supplier diversification — forcing executives to model resilience alongside efficiency.

Transformation momentum has crossed a threshold. Survey evidence shows that a large majority of executives now rank next‑gen supply chain as a top technology priority and many firms have moved beyond pilots into scaled deployments of agentic systems and automation.

Our approach is explicitly operational. The report is structured to support the decisions you must make in 2026 and includes:

Executive playbooks for board-level and C-suite alignment — tailored agendas and milestone templates to accelerate funding and cross-functional governance for supply chain transformation programs.

Roadmaps for technology adoption — sequenced capability builds for AI/ML, IoT, robotics, and cloud that balance speed-to-value with integration risk and data maturity.

Vendor evaluation frameworks — standardized criteria and scoring models for comparing orchestration platforms, planning suites, intralogistics integrators and robotics OEMs, mapped to buyer archetypes and total cost of ownership horizons.

Operational playbooks and KPI templates — measurable success metrics for inventory optimization, lead-time reduction, warehouse throughput and end-to-end visibility, with scenario templates for demand shocks and supplier interruption.

Data and integration blueprints — reference architectures for digital product passports, master data governance, and event-driven connectivity to minimize friction in multi-vendor environments.

Capital planning and infrastructure guidance — models for sizing compute and power needs for AI-driven analytics and digital twins, including sensitivity analyses for rising rack power densities and data center operating costs.

Use-case ROI calculators and implementation timelines — ready-to-run models that help procurement and operations teams estimate payback periods for automation, AMR fleets, and orchestration layers.

The vendor ecosystem is maturing into distinct value clusters: enterprise orchestration suites, real-time planning and scenario platforms, execution and warehouse automation providers, and specialty robotics/AMR players. Market concentration remains relatively open, with top-tier incumbents occupying gateway roles while specialized providers drive rapid point innovation.

SAP SE and Oracle Corporation continue to emphasize end-to-end orchestration and integrated planning within broad enterprise stacks — attractive to organizations seeking deep ERP alignment and supplier governance capabilities.

IBM’s platform and AI expertise positions it as a bridge between traditional B2B connectivity and next-gen, AI-enabled automation — a compelling choice for large, complex networks with heavy integration needs.

Cloud-native planning specialists such as Blue Yonder and Kinaxis are differentiating on speed-to-insight and concurrent planning capabilities, enabling faster scenario modeling and resilience testing.

Execution and warehouse orchestration vendors (e.g., Manhattan Associates, E2open) are focused on harmonizing fulfillment workflows and multi-party visibility; their value is measured in execution KPIs and plug-and-play integration across transportation and warehouse stacks.

Material handling and automation OEMs (Dematic, SSI Schaefer, Vanderlande, Swisslog, Daifuku, TGW) are rapidly integrating software into historically hardware‑centric offers, shifting conversations from capex-only projects to outcomes-based automation services.

Robotics and AMR innovators (GreyOrange, Locus Robotics, Hai Robotics) continue to compress the time-to-value for high-throughput fulfillment and are becoming standard components in modern distribution networks.

Consulting and software integrators (GEP Worldwide, Descartes Systems Group, and others) remain critical for systems integration, hybrid sourcing models and procurement transformation.

Collectively, these players demonstrate that the market is neither winner-takes-all nor purely fragmented — rather, it is characterized by ecosystem specialization, partnership-driven go-to-market strategies, and rising deal complexity that favors integrators with both domain expertise and technical depth.

Industry events and vendor roadmaps indicate a near-term focus on agentic AI, supplier onboarding, and orchestration enhancements — signaling where product investment and partner discussions should start in 2026.

Hardware and infrastructure announcements show that compute supply chains are evolving in parallel: expansions in Arm-based platforms and data-center building block solutions are enabling more cost-effective AI deployments.

Recognition programs and awards highlight practical execution: firms expanding networks and deploying robotics at scale are being rewarded, underscoring the marketplace’s preference for demonstrable outcomes over theoretical benefits.

Vendor cadence, including scheduled product updates, is accelerating — procurement and IT teams should plan for periodic refreshes and compatibility checks when negotiating multi-year contracts.

Prioritize modularity and interoperability: Architect transformation in discrete, testable increments that preserve optionality across orchestration, planning and execution layers.

Build infrastructure cost into the business case: AI-driven modeling changes the calculus for data center investment, energy procurement and infrastructure OPEX—don’t treat compute as an afterthought.

Adopt a resilience-first sourcing posture: Scenario-based planning should be embedded in supplier contracts, inventory strategies and network design to withstand geopolitical shocks.

Make the vendor ecosystem work for you: Use our vendor evaluation frameworks to structure proofs of value (PoVs) that focus on measurable throughput, fill-rate and inventory outcomes rather than feature checklists.

Govern data as a strategic asset: Regulatory requirements converting products into data assets require forward-looking master data governance and product passport strategies to avoid retroactive compliance costs.

Boards and executive committees will use this report as a reference to validate investment size and strategic sequencing. The combination of market sizing, scenario-driven forecasting, vendor benchmarking and executable playbooks provides a single source of truth for capital allocation decisions, procurement negotiations and program governance in 2026.

Immediate: Use the executive playbook to align stakeholders, secure a 2026 transformation budget and launch 90‑day pilots tied to clear KPIs.

Short term: Apply the vendor evaluation framework to narrow partner selections and structure PoVs with financial guardrails and exit criteria.

Medium term: Run the infrastructure sensitivity models to finalize data center and cloud commitments that will underpin AI and digital twin initiatives.

This preview outlines the strategic value and practical applications of our Next Gen Supply Chain Market research. The full report contains the comprehensive datasets, regional and technology segmentation, vendor scorecards, and financial models necessary to operationalize the recommendations outlined here. To obtain the complete market tables, segmented analysis and plug-and-play decision tools, please visit the PW Consulting report page.

PW Consulting — We translate market evidence into executable strategy. Let 2026 be the year your supply chain moves from resilient idea to competitive advantage.

For detailed analysis of this topic, please visit the official page:Next Gen Supply Chain Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com