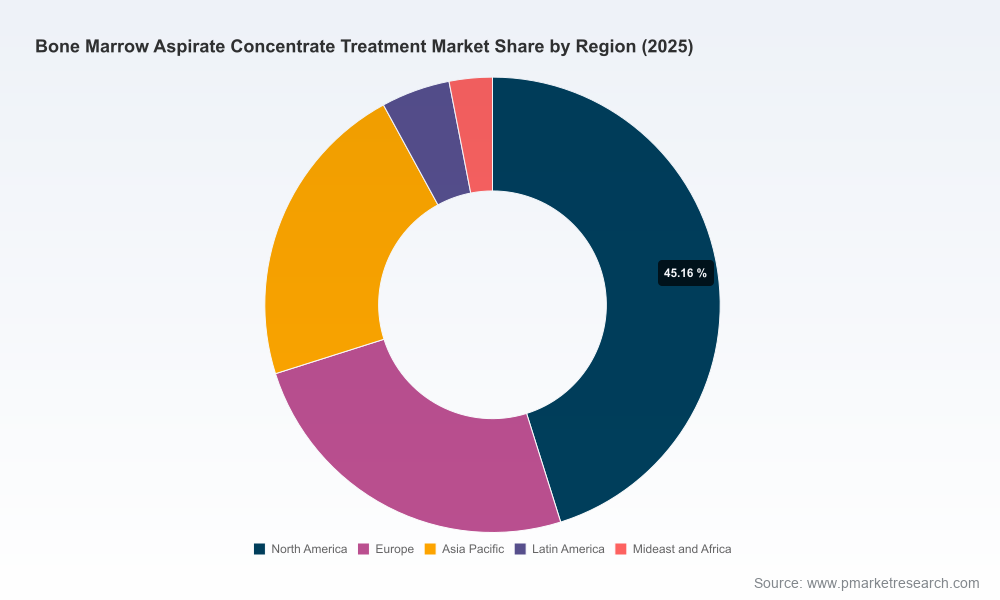

Bone Marrow Aspirate Concentrate (BMAC) Treatment Market — Strategic Preview for 2026 Decision-Making

PW Consulting today releases a strategic preview of our forthcoming Bone Marrow Aspirate Concentrate (BMAC) Treatment Market report, designed to equip life-science leaders, medical device executives, healthcare providers and investors with the actionable intelligence they need to make high-stakes decisions in 2026. The global BMAC market has expanded from a modest base in 2020 to an estimated USD 520.0 Million in 2025, and our model projects continued momentum through the forecast horizon (2026–2032) at a compound annual growth rate (CAGR) of 7.65%, with the total market opportunity approaching the high hundreds of millions by 2032. This preview synthesizes the strategic implications of that trajectory while preserving the granular segmentation and proprietary models for subscribers of the full report.

Bone Marrow Aspirate Concentrate Treatment Market

Why 2026 Is a Pivotal Year

Two concurrent trends make 2026 a decision inflection point. First, the technology and device ecosystem for point-of-care concentration has matured: compact centrifuge platforms, sensor-driven automation and filtration-based aspiration kits are improving procedural throughput and clinical confidence. Second, regulatory and reimbursement frameworks are evolving in ways that create both opportunities and constraints for commercialization.

Bone Marrow Aspirate Concentrate Treatment Market

- Regulatory clarity: many BMAC devices qualify as minimally manipulated autologous HCT/Ps under the FDA 361 pathway when used homologously, enabling point-of-care deployment without the full biologic licensing burden. At the same time, cultured/expanded cellular therapies remain a separate regulatory class and require IND pathways—an important strategic distinction for R&D roadmaps.

- Reimbursement friction: BMAC procedures for most orthopedic indications typically lack broad Medicare or private payer coverage, placing a premium on value demonstration and price architecture that can support out-of-pocket models or bundled care arrangements. Coding practice remains fragmented—CPT 20939 applies in certain grafting contexts while many musculoskeletal uses are billed under unlisted codes—creating revenue predictability challenges that commercial teams must address.

For executives planning 2026 budgets, these forces translate into concrete choices: prioritize product features that lower total procedure cost and clinical time, invest in evidence generation that speaks to payers and hospital financial leadership, and design commercial motions that can win both hospital systems and ambulatory surgical centers.

Bone Marrow Aspirate Concentrate Treatment Market

Market Dynamics Shaping the Opportunity

- Clinical adoption is being driven by outpatient-friendly device designs and increasing operator familiarity with autologous biologics in orthopedics and sports medicine. The shift toward ambulatory settings amplifies demand for compact, single-use consumables and integrated systems that shorten room time.

- Technology differentiation will be decided at the interface of yield, ease-of-use and workflow integration. Double-spin systems and sensor-enabled centrifuges compete with single-step filtration and centrifuge-free kits—each approach has trade-offs between cell concentration yields, contamination risk and capital footprint.

- Commercial success will depend less on headline biological claims and more on quantifiable clinic economics: staff time savings, reduced ancillary disposables, predictable per-procedure costs and demonstrable patient satisfaction metrics that support premium pricing in cash-pay markets.

Competitive Landscape — Where Firms Are Positioning

The BMAC market is showing signs of consolidation alongside pockets of rapid product innovation. The top three global players currently account for a sizeable portion of market revenue, with the top five exerting majority share—creating a landscape where scale, distribution reach and clinical relationships matter, but where differentiated technology and workflow advantages can still upset incumbency.

- Terumo BCT (Harvest) continues to leverage its SmartPrep platform and procedure pack ecosystem to capture institutional business, focusing on reproducibility and integration with existing surgical workflows.

- Arthrex has emphasized sensor-based automation and configurability through its Angel cPRP and Bone Marrow Processing System, targeting clinicians who value customizable formulations and data-enabled consistency.

- Zimmer Biomet’s BioCUE system is positioned around grafting and regenerative applications with channel strategies aimed at established orthopedics networks.

- EmCyte markets high-concentration double-spin systems aimed at customers prioritizing progenitor cell enrichment and laboratory-grade yields.

- Globus Medical, Ranfac and smaller innovators are differentiating through accessory kits, aspiration needle design and single-use disposables that address blood contamination and ease of harvest.

- SurGenTec’s recent FDA 510(k) clearance (August 2024) for a centrifuge-free B-MAN kit with integrated filtration illustrates how regulatory milestones can accelerate market access for alternative approaches to concentration and collection.

Across these players, strategic vectors include: (1) bundling consumables with capital systems to secure recurring revenue, (2) partnering with ambulatory surgical center networks to accelerate adoption, and (3) investing in payer evidence and registry programs to improve coverage outcomes over time.

What PW Consulting’s Report Delivers — Practical, Executable Intelligence

Our full report goes beyond headline figures to provide the operational detail leaders need to act in 2026. Key deliverables include:

- A transparent market model with historical (2020–2025) performance, a detailed base year (2025) calibration and scenario-based forecasts for 2026–2032 that incorporate technology, reimbursement and adoption sensitivities.

- Competitive commercial intelligence: vendor profiles, product feature mapping, distribution footprints, pricing archetypes and M&A activity analysis—built from primary interviews, clinical registry data and proprietary sales channel checks.

- Go-to-market playbooks tailored to device OEMs, consumable suppliers and hospital procurement teams—covering value propositions for hospitals, ambulatory surgical centers and specialty clinics, and including operational templates for procedure cost modeling.

- Regulatory and reimbursement blueprints—an actionable map of FDA pathway considerations (361 vs. IND), payer engagement strategies, and coding risk mitigations tied to CPT treatment patterns.

- Investment and partnership scoring: a framework to evaluate targets and projects against market growth drivers, commercial defensibility and regulatory risk.

To honor the “trailer” principle, the report reserves granular segmentation (detailed splits by region, indication and end-user) and the underlying datasets for subscribers. Those granular views are precisely the inputs decision-makers will use to size addressable segments, prioritize launch geographies and model ROI for product investments in 2026.

Actionable Strategic Imperatives for 2026

- Build a payer/evidence-first commercialization plan: Sponsor pragmatic clinical trials and registries that translate procedural outcomes into cost-offset narratives for hospitals and private payers.

- Prioritize workflow-integrated designs: Systems that reduce OR/clinic time and minimize staff training will win in ASCs and high-volume hospital settings.

- Design pricing for mixed reimbursement realities: Offer tiered capital/consumable bundles and patient-pay programs to preserve volume while protecting margins where insurance coverage is limited.

- Consider strategic M&A or distribution partnerships to accelerate access to ASC networks and specialty clinics—particularly valuable where top players command concentrated share.

- Prepare regulatory contingency plans: Differentiate product development paths depending on whether future innovations will fall under 361 or require IND review.

How PW Consulting Supports Your 2026 Decisions

Leaders engaging with the BMAC opportunity need both the macro roadmap and the micro playbook. Our report combines a transparent forecasting engine, competitive due diligence and implementation-level commercial tactics to shorten the time between insight and impact. Whether you are evaluating a new product launch, an acquisition target, or an evidence generation program, the actionable frameworks in our study are calibrated to the market realities you will face next year.

For access to the full segmentation datasets, proprietary adoption curves and company-by-company financial estimates, visit our report page or contact PW Consulting. The full report contains the detailed tables and model access required to run scenario planning and prioritize investment with precision—information we intentionally withhold from this preview to preserve client value and to direct practitioners to the complete intelligence set.

PW Consulting’s Bone Marrow Aspirate Concentrate Treatment Market report is the strategic reference for any organization that intends to compete meaningfully in BMAC in 2026 and beyond. The growth window is clear; the tactical playbook is now the differentiator.

For detailed analysis of this topic, please visit the official page:Bone Marrow Aspirate Concentrate Treatment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com