What’s Driving Demand for Polyethylene Glycol Across Industries?

Networking |

2026-03-24 07:48:43

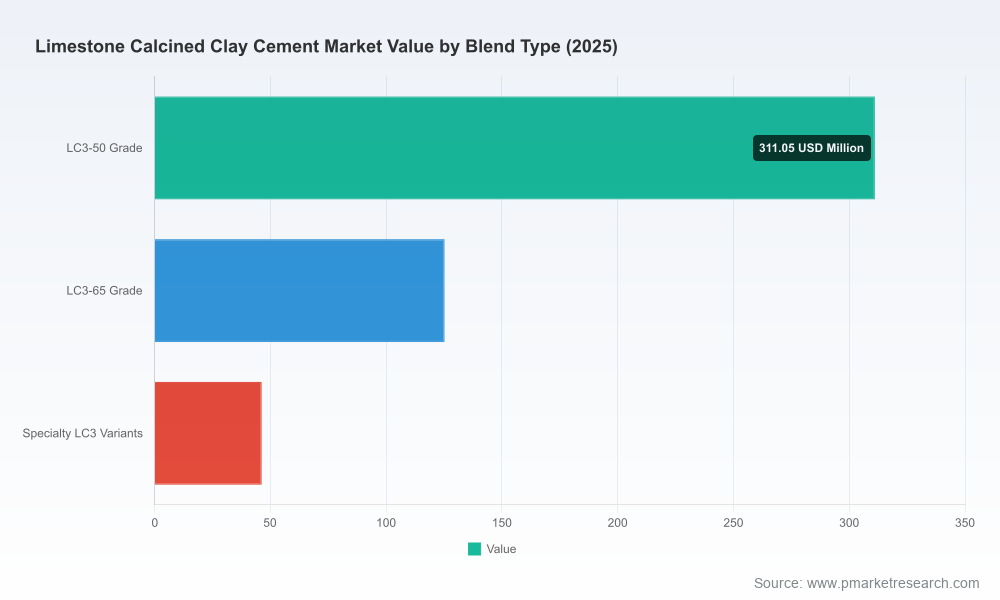

PW Consulting’s latest market study on Limestone Calcined Clay Cement (LC3) frames 2026 as a decisive year for companies seeking to convert low‑carbon ambition into competitive advantage. The global LC3 market has expanded rapidly—from approximately USD 255.4 Million in 2020 to USD 482.5 Million in our base year (2025)—and is forecast to grow at a compound annual growth rate (CAGR) of 13.85% through 2032, reaching roughly USD 1,196.3 Million. These macro dynamics, combined with a maturing technology, evolving standards, and targeted policy support, create both a window of opportunity and a narrow runway for capital deployment, commercial roll‑outs, and strategic partnerships.

Limestone Calcined Clay Cement Market

Standards and policy are aligning with market readiness. Recognition of LC3 under major national and international norms—such as recent updates to U.S. blended cement standards and explicit national acceptances—reduces specification friction for owners and engineers, accelerating procurement decisions in infrastructure and building projects.

Limestone Calcined Clay Cement Market

Industrial scale production is now real. A succession of plant commissions and large‑scale flash calciner projects moved LC3 from pilot to industrial scale in 2025–2026, demonstrating both unit economics and constructability at commercial volumes.

Limestone Calcined Clay Cement Market

Decarbonization incentives are creating asymmetric returns. Targeted grants and demonstration funding—most prominently industrial program awards supporting first‑of‑their‑kind calcined clay lines—materially derisk capital for early adopters and provide a valley‑of‑death bridge for higher‑rate projects.

Input‑cost and energy advantages are measurable. Calcination of clay for LC3 requires significantly lower temperatures than traditional clinker production, delivering material energy reductions (leading studies demonstrate up to ~33% lower energy use) and operational savings versus ordinary Portland cement. Typical calcined clay production costs fall in a narrow band driven primarily by raw clay and energy, supporting rapid scale economics where feedstock and energy are secure.

Our research is structured to turn insight into action across five pragmatic workstreams—each containing proprietary models, decision templates, and implementation guidelines:

Market sizing & scenario modelling: A robust baseline with upside and downside demand pathways (short‑cycle demand shocks, high‑adoption decarbonization scenarios), sensitivity tests for energy price variance, and roll‑rate assumptions calibrated against recent plant commissions.

Commercial playbooks: Go‑to‑market strategies for producers (brand differentiation, specification pathways, blended product portfolios), procurement templates for owners and EPCs, and route‑to‑market blueprints for distribution partners and ready‑mix chains.

Techno‑economic and plant design tools: Retrofit vs greenfield calculators, stepwise capex schedules, LCOC and LCOE‑style carbon marginal abatement models, and modular build‑out sequencing for flash calciners and auxiliary systems.

Regulatory & standards playbook: Mapping of local and international normative frameworks, acceptance strategies for project specifications, and a compliance checklist for ASTM, national standards bodies, and green certification schemes.

M&A and partnership radar: Target profiles for asset and capability acquisitions, JV term sheets and earn‑outs, and a short list of engineering and raw‑material service providers aligned to rapid scale‑up.

To preserve commercial sensitivity and to drive strategic conversations, granular subsegment financials and the full dataset of regional/application splits are available exclusively with the full report and accompanying models.

Market structure analysis shows a moderate level of concentration: the top three players account for roughly one‑third of market activity while the top five approach just under half—indicative of an industry where major cement groups lead with scale, but regional and fast‑moving challengers hold decisive tactical advantages.

Global integrated players (e.g., major European and Mexican groups) are leveraging existing clinker portfolios to accelerate LC3 offerings within broad low‑carbon cement portfolios. Their strategic advantage lies in cross‑plant deployment, customer relationships, and downstream logistics integration.

Regionally dominant producers in India and Latin America are converting first‑mover local credibility into national specification wins on large infrastructure projects. These firms demonstrate how a focused commercial push—paired with localized manufacturing—can secure long‑term demand commitments.

New industrial entrants and JV models—particularly those that deploy flash calcination at scale—are changing the cost curve. Several recently completed plants and cross‑border joint ventures validate a new capital‑efficient route to large LC3 throughput.

Notable company developments and strategic moves signal where capability leadership is consolidating: large flash calciner completions, commissioning of million‑ton capacity LC3 lines, commercial rollouts in infrastructure projects, and targeted funding for first‑of‑a‑kind plants in developed markets. Collectively these moves accelerate technology validation and create reference projects that shorten sales cycles for product adoption.

Cement producers: Prioritize a dual approach—deploy at least one commercial‑scale LC3 line (or convert a pilot into a line) and simultaneously sign offtake or specification agreements with key infrastructure customers. Use modular capex staging to reduce exposure while building technical expertise.

Investors and financial sponsors: Assess projects via our LCOC and abatement curves rather than headline CAPEX. Early‑stage grants and DOE‑style incentives materially improve IRR; structure investments with milestone‑based tranches tied to commissioning and performance guarantees.

Equipment and engineering firms: Focus on flash calciner modularization and energy‑integration packages. Offering integrated services—calciner supply, kiln retrofits, and commissioning support—creates stickiness and differentiates you from pure‑equipment vendors.

Project developers and EPCs: Update specs and tender templates to include LC3 acceptance clauses and performance‑based warranties. Engage materials testing partners early to remove technical objections in design phases.

Policy makers and project sponsors: Link low‑carbon procurement incentives to validated performance metrics and prioritize funding for demonstration projects that deliver long‑term feedstock security and worker retraining plans.

Key risks for 2026 implementation include feedstock supply security, energy price volatility, specification inertia in conservative construction markets, and scaling execution. Mitigation levers that repeatedly surface in profitable programs include diversified clay sourcing strategies, energy‑efficiency retrofits and waste‑heat recovery, early engagement with standards bodies and specifiers, and binding offtake agreements with performance clauses tied to product acceptance.

Board level: Use the report’s scenario set to calibrate capital allocation and to set internal decarbonization targets with associated ROI timelines.

Business unit leaders: Apply the go‑to‑market playbooks and commercial checklists to accelerate specifications and secure pilot projects that convert into long‑term contracts.

Investment committees: Use the techno‑economic models and risk matrices to underwrite equity or debt for LC3 projects on a like‑for‑like basis with other low‑carbon investments.

LC3 is no longer a niche research topic—it is an investable industrial pathway that can materially reduce embodied carbon in concrete while offering meaningful operational cost leverage. Our analysis shows a large, fast‑growing market (from ~USD 255.4 Million in 2020 to ~USD 482.5 Million in 2025, and projected to surpass USD 1,196.3 Million by 2032 at a 13.85% CAGR) and a competitive landscape in active flux. The PW Consulting LC3 report is designed as a transactional playbook: it provides the detailed models, procurement instruments, and field‑validated checklists that senior leaders need to convert strategy into executed projects in 2026 and beyond.

To preserve competitive value and to catalyze direct engagement, we intentionally withhold granular subsegment tables and region/application splits from this preview. For full access to the dataset, proprietary scenario models, and tailored advisory packages—plus an executive briefing with our senior strategists—contact PW Consulting or visit our report page to request the complete intelligence package.

For detailed analysis of this topic, please visit the official page:Limestone Calcined Clay Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com