UAV-Based Gas Leak Detector Market: Strategic Imperatives for 2026 — PW Consulting Report Highlights

As energy, waste management and industrial operators confront intensifying regulatory scrutiny and elevated expectations for methane mitigation, UAV-based gas leak detection has moved from experimental to operational in a remarkably short time. PW Consulting’s latest market study — covering the historical period 2020–2025 with 2025 as the base year and a forecast window of 2026–2032 — quantifies this transition and distills the practical implications that senior executives and technical leaders must act on in 2026.

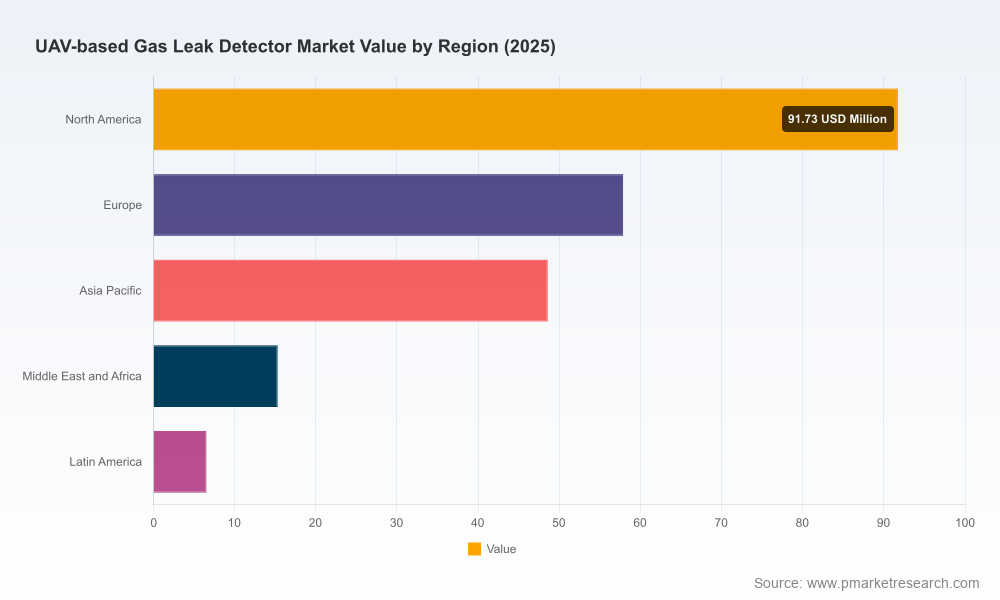

Uav Based Gas Leak Detector Market

Market trajectory at a glance

Our analysis shows the UAV-based gas leak detector market expanding from a nascent set of pilots and point solutions into a mainstream monitoring modality. The market size reached USD 220.0 Million in 2025 and is projected to grow to approximately USD 257.7 Million in 2026, with a compound annual growth rate (CAGR) of 14.82% across the 2026–2032 forecast period. By the end of the forecast horizon the market is expected to be several times its 2025 scale — reflecting faster adoption across pipeline operators, landfill operators, utilities, and offshore/remote facilities.

Uav Based Gas Leak Detector Market

That growth is not uniform: it is driven by a confluence of regulatory momentum, sensor capability improvements, lower operational costs for UAV deployments, and the rising importance of verified emissions inventories. These tailwinds create a narrow window in 2026 for companies to secure technology leadership, win preferred-vendor status with large asset owners, and shape emerging standards.

Uav Based Gas Leak Detector Market

Why 2026 is a strategic inflection point

- Regulatory acceleration: Recent rulemaking and approvals from U.S. federal agencies — including pipeline safety updates and EPA authorizations of certain drone-based methods — have materially changed the risk calculus for compliance. These shifts make aerial leak detection an eligible and often preferred choice for meeting inspection obligations.

- Technology differentiation: Multiple sensing approaches (laser absorption methods, optical gas imaging, gas-mapping LiDAR, and conventional electrochemical/semiconductor sensors) have matured, creating distinct value propositions for accuracy, range, and quantification. Platform-agnostic analytics and integrated GPS-tagged reporting are becoming the de facto standard.

- Operational economics: The cost profile of UAV deployments has improved as sensor payloads, flight autonomy, and data analytics reduce per-inspection time and false positive burdens. Organizations running broad asset portfolios can achieve rapid payback on pilots when combined with risk-based inspection cadences.

What this report delivers — actionable intelligence, not generic forecasts

PW Consulting designed this study as an operational playbook for decision-makers moving from evaluation to deployment. The report combines quantitative market sizing and trend analysis with hands-on frameworks that support tactical implementation:

- Full historical market series (2020–2025) and a granular forecasting model for 2026–2032, enabling scenario-based planning across conservative, baseline, and accelerated adoption paths.

- Vendor scorecards and technology assessments that compare detection thresholds, operational range, platform compatibility, and software capabilities — intended to streamline vendor selection without substituting for site pilots.

- Procurement and contracting templates, including recommended SLAs, data ownership clauses, and performance-based payment structures tailored to recurrent inspection programs.

- Step-by-step pilot-to-scale playbooks: recommended KPIs for 30/90/180-day pilots, integration checklists for GIS and asset management systems, and a sample ROI/TCO model to validate business cases.

- Regulatory mapping and compliance checklists aligned to major frameworks and recent regulatory changes, including methods now recognized by U.S. agencies for certain drone-applied inspections.

Competitive landscape — who matters and why

The vendor ecosystem is diverse, spanning focused sensor specialists, systems integrators, and industrial automation incumbents. Competitive intensity is moderate: the three largest vendors capture a substantial but not dominant share of market value, while the top five account for a clear majority — a structure that encourages both vertical specialization and ongoing consolidation as enterprise buyers prefer bundled hardware + analytics + services.

- Pergam USA (Pergam-Suisse AG) — Offers laser-based detectors optimized for a range of UAV platforms and fixed-wing installations, with emphasis on real-time GPS-tagged reporting for pipeline and facility inspections.

- SeekOps — Sensor-agnostic, analytics-driven provider focused on methane localization and quantification (LDAQ). Their product suite targets energy sector compliance programs where quantified leak data feeds regulatory reporting and emissions inventories.

- ABB Ltd. — Industrial incumbent that integrates OA-ICOS sensing into a packaged aerial solution, leveraging its field automation and control pedigree to serve regulated utilities and transmission operators.

- Bridger Photonics — Differentiates on LiDAR-based gas mapping, which is particularly suited to high-precision, wide-area surveys including offshore and LNG sites.

- Percepto — Brings autonomous OGI drone systems with documented regulatory acceptance for certain federal inspections, emphasizing reliability at low emission rates.

- Teledyne FLIR — Supplies multi-gas payloads and imaging cameras widely used on industrial UAVs, leveraging its thermal imaging heritage to expand into hydrocarbon and methane monitoring.

- Sniffer Robotics — Focuses on landfill and biogas applications with payloads and methods that have secured alternative approvals under EPA guidance for surface emissions.

Two recent developments underscore the shifting competitive and regulatory landscape: in 2025, one autonomous OGI drone system received an EPA Alternative Test Method designation for certain oil & gas inspections, and another provider introduced a drone-deployed gas-mapping LiDAR optimized for offshore and LNG environments. These milestones validate aerial methods for compliance use cases and accelerate commercial procurement.

How to use the report to shape 2026 decisions

- Technology selection and pilot design: Use our sensor-technology decision matrix to match detection needs (range, quantification, target gas) to platform and analytics choices. The report’s pilot templates reduce trial time and produce defensible results for procurement committees.

- Compliance-first roadmaps: Map inspection cadences, reporting formats, and evidence chains directly to regulatory requirements. We provide legal-technical checklists to bridge field data to audit-ready deliverables.

- Vendor / partner strategies: Identify whether to build in-house capabilities, select a managed-service provider, or pursue joint development with a sensor OEM. We provide M&A scorecards for acquirers seeking bolt-on capabilities in analytics or specific sensor technologies.

- Operational scaling: Deploy reusable SOPs for flight ops, data QA/QC protocols, and maintenance schedules for sensor drift and calibration — all included as downloadable templates.

Risks, uncertainties, and watch items for 2026

- Regulatory nuance: While federal recognitions expand options, state-level and international regimes remain heterogeneous. Buyers must confirm that chosen methods meet local acceptance criteria.

- Performance variability: Differences in detection thresholds and quantification accuracy across sensor types can drive large variations in false positive rates and remediation costs if not carefully validated.

- Airspace and operational limits: BVLOS waivers, battery endurance, and weather resilience remain operational constraints that will influence fleet sizing and inspection economics.

- Data governance: As aerial detection scales, asset owners must define ownership, retention, and cross-border transfer policies for sensitive emissions datasets.

- Consolidation and vendor risk: The market is evolving — alliances, acquisitions, and product retirements can change supply dynamics rapidly. Our vendor risk matrix helps buyers mitigate single-source exposure.

Final observations — converting insight into advantage

For companies deciding capital allocation in 2026, the question is no longer whether aerial gas detection will be part of the toolkit; it is how much of the inspection program will migrate to UAV-enabled methods and under which commercial model. With a robust baseline market of USD 220.0 Million in 2025 and an estimated market expansion to roughly USD 257.7 Million in 2026 (CAGR 14.82% through 2032), leaders must act quickly to: secure proven vendors for compliance, standardize data pipelines for emissions accounting, and build flight ops know-how that scales safely and cost-effectively.

Accessing the full intelligence

PW Consulting’s full report includes the complete forecasting model, vendor scorecards, scalable pilot templates, procurement language, and downloadable operational checklists. In keeping with our “trailer” approach, this release highlights the report’s strategic value and core findings while reserving detailed subsegment tables and proprietary vendor scoring data for the full document. To review the full dataset and obtain licensing information, visit our official report page or contact our industry team directly for a briefing and tailored executive summary.

For detailed analysis of this topic, please visit the official page:Uav Based Gas Leak Detector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com