New Zealand Medical Imaging market Size, Share, Trends, Key Drivers, Growth and Opportunity Analysis

Other |

2026-05-21 13:05:38

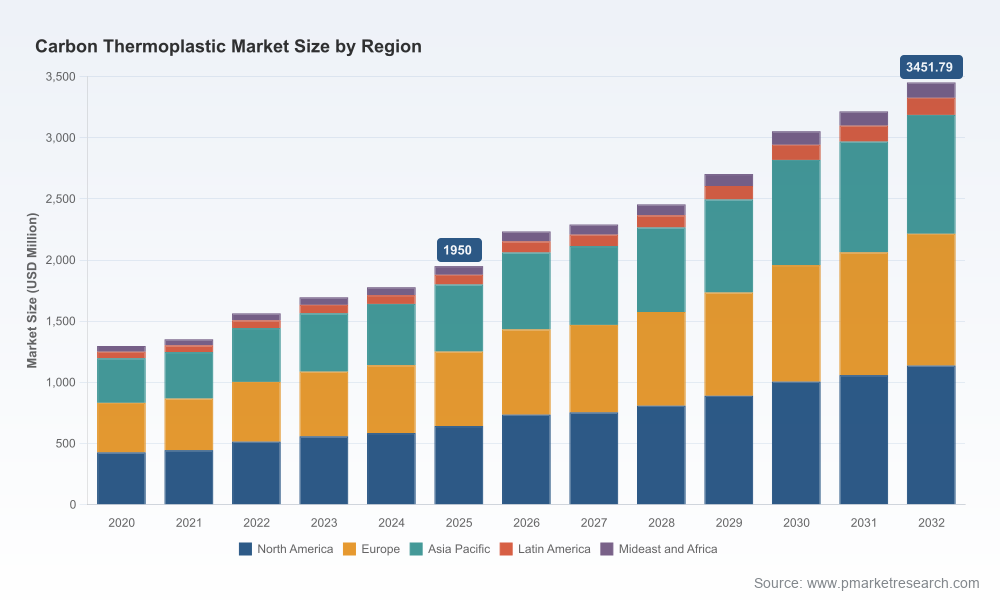

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I am pleased to introduce a strategic preview of our full Carbon Thermoplastic Market report. The market has moved from a niche advanced-materials segment to a commercially relevant platform for mobility, aerospace, and industrial OEMs. Critically, total industry revenue reached USD 1,950.0 Million in our base year (2025) and, under our central forecast, is projected to expand at a compound annual growth rate (CAGR) of 8.5% — surpassing USD 3,450 Million by 2032. This preview highlights the insights that will matter most to C-suite and business-unit leaders planning 2026 capital, sourcing and product decisions. Core subsegment tables and our proprietary demand models are intentionally omitted here; full datasets and executable playbooks are available on the report landing page.

Carbon Thermoplastic Market

Transition to high-volume applications: Carbon thermoplastic composites are crossing the gap from low-volume, premium applications into mid- and high-volume transport and industrial platforms thanks to faster cycle manufacturing methods and material system improvements.

Carbon Thermoplastic Market

Commercialization meets regulation: New recyclability claims and regulatory changes are reshaping acceptable chemistries and hand-in-hand driving product development priorities.

Carbon Thermoplastic Market

Macro tailwinds and constraints: Electrification of transport and demands for lightweight structures underpin long-term growth, while input-cost volatility and trade measures require tactical responses in 2026.

Top-down and bottom-up demand forecasts (2026–2032) for the overall market and our scenario envelopes—used to stress-test CAPEX and commercial plans.

Technology readiness mapping for major matrices (PA, PEEK, PC and emerging resins), linking process constraints to unit economics and cycle-time improvements.

Supplier and value-chain scorecards — manufacturing footprints, capacity trajectories, and strategic moves, with bespoke recommendations for supplier diversification and localization.

Commercial playbooks for OEMs and tier suppliers covering go-to-market, pricing strategy, and co-development frameworks designed to derisk first-mover investments.

CapEx modelling templates and project-level IRR sensitivity checks to inform brownfield vs greenfield decisions and automation investment thresholds.

Risk heatmaps: raw material, regulatory, transport, and geopolitical shocks with recommended mitigation actions prioritized by business impact.

Input-cost pressures: Upstream supply tightness pushed polyacrylonitrile (PAN) precursor prices materially higher; our analysis incorporates reported increases that tighten margins for carbon fiber and, by extension, thermoplastic compounds. Procurement strategies that ignored precursor pricing signals in 2024–25 are now a liability.

Regulatory reclassification and material compliance: Updated chemical restrictions in major markets have constrained some flame-retardant options for certain matrices, creating a compliance-driven pivot toward alternative chemistries and supplier-qualified formulations.

Trade and transport friction: Elevated tariffs and sustained ocean freight surcharges are reshaping effective landed costs. We quantify the impact of recent tariff and IMO-driven freight changes and model threshold distances where local sourcing becomes economically attractive.

Processing constraints: High-temperature systems (e.g., PEEK-based solutions) remain technically attractive but require specialized processing (>400°C in many cases), limiting near-term scale-up to players with the right capital and processing expertise.

The competitive field is diverse: incumbent carbon fiber majors, specialty-chemical groups, composite-focused manufacturing houses, and a set of regional specialists. Market concentration is moderate — our CR3 and CR5 metrics show significant, but not dominant, topline shares among leading players, indicating space for regional challengers, vertical integration by OEMs, and tuck-in acquisitions.

Toray Industries — Leading with advanced carbon fiber systems and recently launched thermoplastic prepregs engineered for high-rate automotive programs. Toray’s technology depth and integrated fiber-to-prepreg capability make it a natural partner for OEMs wanting a single-source roadmap to mass production.

Solvay / Syensqo — Focused on capacity expansion aligned with EV platform demand; the company’s investments are defensive and offensive: securing feedstock to support thermoplastic CFRT for structural transport parts.

Teijin Limited — Competes on application-specific, high-performance matrices and has been progressing through certification workflows for demanding industrial and aerospace use cases.

Mitsubishi Chemical Group — Brings compound and prepreg expertise and a broad resin portfolio—advantageous for OEMs seeking material system bundling for mixed-architecture platforms.

Arkema — Differentiates on recyclable resin solutions showcased at major industry venues, positioning itself for OEMs that must demonstrate circularity credentials.

Hexcel, SGL Carbon, Gurit — Each plays to strengths: Hexcel on aerospace production readiness; SGL on automotive tape solutions and strategic OEM partnerships; Gurit in larger-structure wind and marine segments. Recent targeted collaborations underline an ecosystem shift toward co-development.

PlastiComp, Lingol — Specialists in long-fiber compounds and molding-ready feedstocks; they are the pragmatic choice for high-volume supply and rapid manufacturing adoption at the tier level.

Sourcing and supplier strategy: Move from transactional to strategic supplier relationships. Lock in multi-year pricing where possible, prioritize regional dual-sourcing to mitigate tariff and freight exposure, and include precursor-indexed clauses to share unforeseen PAN price volatility.

Product and technology choices: Favor matrix systems that balance performance with manufacturability. PEEK will remain premium and niche until processing and cost barriers are meaningfully reduced — plan PEEK use for high-margin, safety-critical applications while driving PA/PC adoption for volume parts.

Manufacturing investments: Prioritize high-throughput prepreg and tape processes, automation in layup and consolidation, and pilot lines that validate cycle times under production constraints. Where freight and tariffs are significant, regionalize capacity with flexible, modular cells.

Commercial & pricing tactics: Adopt value-based pricing for structural applications and build tiered value propositions for recyclable/resin-certified offerings to capture sustainability premiums.

M&A and partnerships: Seek bolt-ons that close capability gaps (e.g., high-rate tape manufacturing, recycling technology, or precursor feedstock security).

This preview intentionally omits our granular regional, application and type split tables, proprietary pricing curves, and company-level financials and model outputs. Those components are the heart of transaction readiness: they include downloadable Excel models, sensitivity dashboards, SKU-level margins and the full scenario matrix that drive our CAPEX and M&A recommendations. We withhold them to preserve the strategic value of the full report and to guide readers who require the actionable datasets for board-level decisions to the report landing page.

0–90 days: Audit current contracts, run fast-sensitivity tests on feedstock price exposure, and initiate qualification pilots with at least two alternative suppliers for critical components.

90–180 days: Commence pilot manufacturing cells, finalize co-development agreements with preferred material suppliers, and validate the cost-benefit of regionalizing production vs. paying freight/tariff premia.

180–360 days: Make final CAPEX decisions conditioned on pilot performance and demand realization; execute targeted M&A or JV agreements to secure capacity or technology that materially shortens time-to-market.

PW Consulting stands ready to mobilize a tailored workshop or valuation exercise using the report’s full datasets and scenario models. For teams that need a rapid, defensible forecast to support board approvals or investment committees in 2026, our advisory engagements provide executable roadmaps and direct access to the modeling and supplier benchmarking behind these conclusions. Visit the official report page to retrieve the complete study, download the Excel models, and schedule a walkthrough with our industry specialists.

For detailed analysis of this topic, please visit the official page:Carbon Thermoplastic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com