Patient Safety and the Vascular Access Devices Market Forecast 2031

Health |

2026-07-01 15:11:20

PW Consulting’s latest market study on Jet Engine Nozzles delivers a focused, decision-ready perspective for executive teams preparing for 2026. Grounded in a full historical review (2020–2025) and a detailed forecast (2026–2032), the report synthesizes technical, commercial, and supply-chain intelligence to translate market movement into actionable choices. At the top-line level, the global market for jet engine nozzles is expected to continue expanding from the mid-2020s base, following a compound annual growth rate of approximately 5.85% through the forecast horizon. That trajectory drives meaningful revenue expansion for suppliers, OEMs, and aftermarket providers and creates discrete strategic inflection points for capital allocation, M&A, and product development in 2026.

Jet Engine Nozzles Market

Investment timing: The projected multi-year expansion informs when to accelerate capital deployment into new nozzle production capabilities (e.g., additive manufacturing or hybrid machining lines) versus prioritizing incremental process upgrades.

Jet Engine Nozzles Market

Technology bets: Emerging nozzle architectures and manufacturing techniques—ranging from variable-geometry and thrust-vectoring designs to advanced surface treatments—are moving from R&D into demonstrator and program phases. Executives must decide which pathways to internalize, partner for, or license.

Jet Engine Nozzles Market

Supply-chain resilience: Concentration in critical raw materials and the increasing role of specialty superalloys and titanium highlight the need for supplier diversification, long-term contracts, and material hedging strategies.

Aftermarket strategy: As fleet utilization and MRO cycles normalize post-pandemic, there are earnings opportunities in repair, retrofits, and nozzle upgrades—especially for firms that can deliver reduced life‑cycle cost or emissions improvements.

OEM-led platform evolution: Progress on industry programs—such as open‑fan and other next‑generation architectures—has accelerated nozzle technology requirements. Public program updates observed in 2025 reinforce the timeline for prototype and qualification work.

Demonstrators and platform showcases: Military and demonstrator programs are advancing advanced nozzle forms (including 2D thrust-vectoring hardware) that will compress the development-to-field cycle for downstream suppliers.

Academic and lab advances: University and research center projects focused on noise‑reducing nozzle geometries are reaching maturity, signalling opportunities to couple academic IP with industrial scale‑up in 2026.

Market sizing & trajectory: A robust top‑line market model that tracks historical performance (2020–2025) and projects market evolution across 2026–2032 under base, upside and downside scenarios.

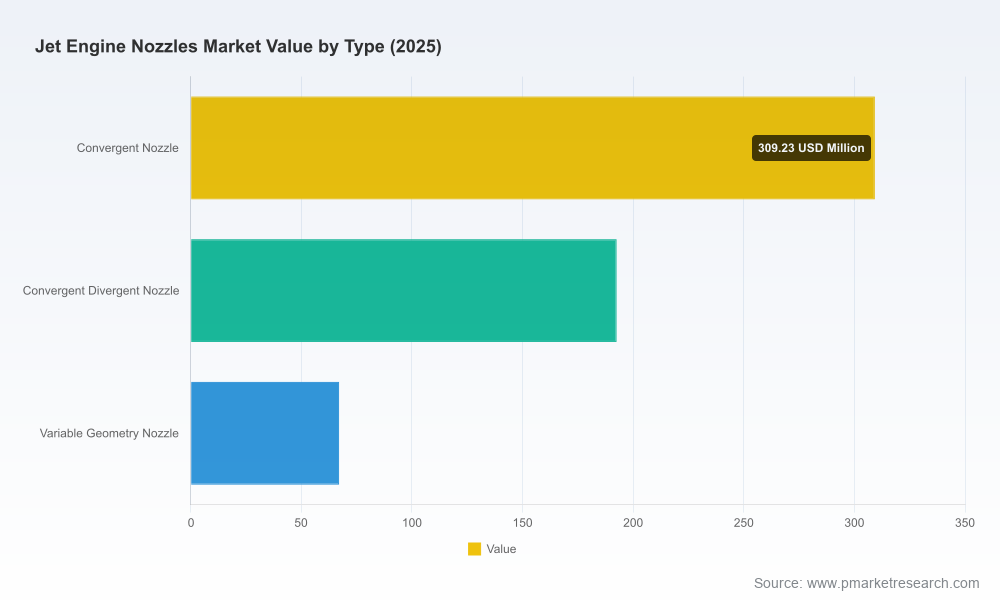

Technology landscape map: Detailed profiles of nozzle architectures (fixed convergent, convergent‑divergent, variable geometry, thrust vectoring, low‑noise geometries), technology readiness levels, and expected timeline to commercial adoption.

Manufacturing playbook: Benchmarked unit-cost drivers, capacity planning guidance, comparative case studies on additive versus machining pathways, and plant-scale investment modeling to support CAPEX decisions.

Materials and sourcing diagnostic: A targeted assessment of nickel‑based superalloys, titanium alloys, and coating markets—identifying single‑point risks, qualification lead times, and preferred sourcing levers.

Aftermarket & MRO module: Serviceable lifecycle analyses, retrofit upgrade cases, and a roadmap for capturing remanufacturing revenue and improving Time Between Overhauls (TBO) economics.

Competitive and partnership strategies: Player matrices, supplier archetypes, and a staged partnership playbook for OEMs, tier‑1 suppliers, fabricators, and repair specialists.

Regulatory and sustainability impact review: How emissions standards and noise regulation pathways are likely to shape nozzle design priorities and procurement preferences in 2026 and beyond.

Decision support tools: Excel models, sensitivity runs, risk heatmaps, and an executive checklist tailored for board‑level and operating committee use in 2026 planning cycles.

The nozzle market exhibits notable concentration among a small set of technologically advanced OEMs and specialized suppliers. PW Consulting’s competitive analysis synthesizes public program activity, technology investments, and capability footprints to reveal strategic positioning that matters for 2026.

GE Aerospace: A leader in integrating additive manufacturing into nozzle production—notably for high‑value, complex geometries tied to contemporary commercial engine families. GE’s emphasis on additive routes supports light‑weighting and part consolidation strategies that reduce assembly steps and lead times.

Safran Aircraft Engines (via JV partnerships): Through collaborative programs with major engine OEMs, Safran continues to refine high‑temperature nozzle capabilities. Their strength is in scaling high‑temperature materials and coatings for sustained thermal performance.

Pratt & Whitney: With a footprint in both military and geared turbofan applications, Pratt & Whitney’s nozzle developments are aligned with fuel‑efficiency and thermal-management priorities across commercial and defense segments.

Rolls‑Royce: Focused on widebody and advanced platform programs, Rolls‑Royce couples large‑scale engine integration with advanced‑materials efforts (notably for next‑generation UltraFan‑class architectures).

Specialists and suppliers: Firms such as Wall Colmonoy/Aerobraze, Moeller Aerospace, The Lee Company, and ITP Aero play complementary roles—offering repair and refurbishment expertise, precision machining, compact fluid systems, and niche thrust‑vectoring designs respectively. These specialists are critical partners in sustaining OEM program schedules and aftermarket performance.

Market concentration metrics indicate a high degree of aggregation among leading firms, underlining the strategic importance of partnerships and selective M&A to access capability gaps or secure program positions.

Superalloys dependency: Nickel‑based superalloys remain a foundational material for many high‑temperature nozzle components. Their market dominance and long qualification timelines create potential bottlenecks that should be addressed through dual sourcing and long‑lead procurement.

Titanium criticality: Titanium alloys are indispensable in many nozzle subcomponents—particularly for military applications—where substitutes are limited. This adds a structural constraint to supplier selection and inventory strategies.

In sum, materials strategy is not a peripheral procurement exercise but a core strategic lever that will determine whether a manufacturer can meet program timelines and margin targets in 2026.

Prioritize capability pockets, not blanket investment: Target investment into additive manufacturing where it reduces part count, shortens supply chains, or unlocks performance benefits; avoid across‑the‑board capital expansion without validated program routes.

Lock strategic supply agreements for superalloys and titanium now: Negotiate multi‑year frameworks with priority production slots and qualification support to avoid costly program delays.

Use M&A selectively to fill capability gaps: Identify acquisition targets among precision specialists and MRO providers to secure aftermarket channels and specialized manufacturing skills.

Shift from product to systems wins: Compete on nozzle sub‑systems (materials + coatings + control elements + integration) rather than on single components to capture higher value and create switching friction.

Embed regulatory scenario planning into product roadmaps: Ensure new nozzle concepts address both emissions and noise trajectories; early certification planning shortens time‑to‑market.

Commercialize retrofit and upgrade pathways: Develop low‑risk, high‑margin nozzle retrofit kits for in‑service fleets to capture aftermarket cashflows while new platform ramps proceed.

Create a lab‑to‑line pipeline with academic partners: Convert demonstrator benefits (e.g., noise‑reducing geometries) into validated production designs through co‑funded scale‑up programs.

This release intentionally highlights strategic direction, validated technology trends, and practical decision frameworks while withholding the detailed subsegment breakouts and discrete regional/application financial splits that many operating teams require for contract tendering, procurement negotiations, and CAPEX approval. Those granular tables, downloadable models, and supplier maps are available exclusively in the full PW Consulting report package and accompanying dataset.

If your 2026 planning cycle requires program‑level sensitivity runs, supplier heatmaps, or executable procurement playbooks, PW Consulting’s full Jet Engine Nozzles Market report provides the complete data pack and tailored advisory options to convert insight into action.

Review the full dataset to validate assumptions used in CAPEX and M&A memos.

Engage PW Consulting for a condensed executive workshop that ties the report’s strategic recommendations to your program timelines and budget cycles.

Commission a supplier‑level due diligence focused on materials qualification and additive‑manufacturing readiness if your 2026 roadmap includes nozzle product launches or aftermarket rollouts.

PW Consulting’s Jet Engine Nozzles Market report is crafted for boardrooms, strategy teams, and functional leaders who must transform technical complexity into executable corporate choices in 2026. For access to the full analytical dataset, subsegment granularity, and decision support tools, please visit our website to request the complete report and advisory options.

For detailed analysis of this topic, please visit the official page:Jet Engine Nozzles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com