Sleep and Recovery: The Unsung Heroes of Post-Weight Loss Surgery in Dubai

Health |

2026-05-07 07:24:05

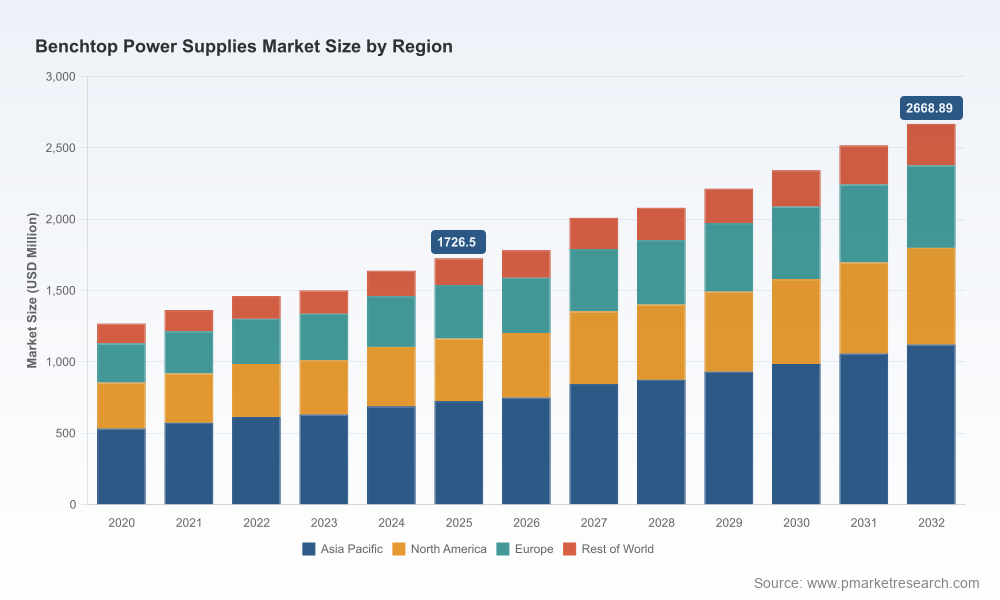

As benchtop power supplies continue to underpin R&D, test-and-measurement, industrial validation and automated test environments, PW Consulting’s latest market study delivers the practical intelligence executives need to prioritize investments, shape product roadmaps, and de‑risk supply chains going into 2026. Our analysis shows the market expanding from approximately USD 1.73 billion in 2025 to an expected USD 2.67 billion by 2032, underpinned by a 6.42% compound annual growth rate over the 2026–2032 forecast window. That trajectory, combined with an industry that is moderately concentrated (top‑3 and top‑5 manufacturers control a meaningful share of industry revenue), creates a dynamic landscape where timing and differentiation matter.

Benchtop Power Supplies Market

Growth is steady, not explosive. The mid‑single digit CAGR reflects broad, technology‑driven demand (semiconductor/electronics test, automotive & EV validation, industrial and lab segments) rather than speculative uptake. This favors disciplined, ROI‑focused investments rather than scope‑expanding gambles.

Benchtop Power Supplies Market

Competitive intensity is structural. The market’s concentration profile favors manufacturers with deep channel relationships, established instrument reliability, and software ecosystems that extend device value through automation and remote management.

Benchtop Power Supplies Market

Costs and regulation are reshaping product economics. Raw material cycles, component cost deflation in strategic semiconductors, and tightened environmental and safety standards are converging to shift product design priorities toward higher efficiency, modularity, and serviceability.

The PW Consulting study is built as an executive toolkit, not an academic exercise. It combines a granular revenue model and forward scenario runs with a suite of actionable deliverables managers can deploy immediately:

Bottom‑up market model calibrated to vendor shipments, bill‑of‑materials trends and channel feedback, producing annual revenue series (2020–2025) and detailed forecasts across 2026–2032.

Five strategic playbooks (product, pricing, channel, service, and calibration) that map to specific revenue levers and cost levers for OEMs, contract manufacturers and distributors.

Supply‑chain heat maps and vulnerability scoring that identify single‑point risks (critical magnetics, connector assemblies, calibration fixtures) and quantify near‑term margin exposure from commodity cycles.

M&A and partnership scorecards oriented by capability gaps — e.g., remote instrumentation software, high‑power modular architectures, automated calibration services — with target prioritizations based on strategic value and integration friction.

Regulatory impact assessment and compliance playbook covering RoHS updates, safety standard adoption and energy efficiency thresholds, with recommended BOM and process changes to minimize certification delays.

Three structural forces will dominate boardroom discussions next year:

Technology substitution and cost deflation. The price decline in wide‑bandgap power devices has meaningfully altered the performance/cost calculus for switch‑mode architectures. Lower costs for SiC and improved switching efficiency enable smaller, higher‑power density benchtop supplies — a competitive edge for suppliers that can integrate these devices effectively.

Commodity and labor pressure. Recent upward swings in copper costs and rising skilled assembly wages are increasing the variable cost base for precision instruments. Producers that pursue modular designs, localized calibration hubs, or alternative materials will be better positioned to protect margin while maintaining uptime guarantees.

Regulatory and standards tailwinds. The growing emphasis on energy efficiency and tightened hazardous substance limits requires early design changes; vendors that pre‑certify platforms to the newest safety and eco‑directives will shorten time‑to‑market and win enterprise procurement cycles where compliance auditing is mandatory.

Our competitor assessment synthesizes product roadmaps, channel footprint and recent go‑to‑market moves to identify where market share is most contestable:

Large instrument OEMs continue to defend premium segments through measurement accuracy, certification pedigree and integrated software suites. Recent product activity shows this playbook remains intact — for example, high‑precision quad‑output benchtop introductions and expanded data‑logging capabilities have been focal points for established brands.

Mid‑tier and value players are sharpening differentiation via multi‑channel configurations, embedded connectivity (USB/LAN) and competitive power‑per‑dollar positioning. These firms are gaining traction in education, small‑lab and certain industrial test budgets.

High‑power and modular suppliers target specialized lab and ATE applications where scalability and serviceability matter more than per‑unit price. Their value proposition is in system integration and total cost of ownership across bench and rack deployments.

Product introductions emphasizing multi‑output capability and advanced data logging have accelerated adoption in labs that need parallel validation streams and traceability.

Connectivity and remote control (enhanced web interfaces, LAN/USB management) are moving from convenience features to procurement must‑haves for distributed test facilities and automated test systems.

Trade show demonstrations and incremental product upgrades continue to be the fastest route for vendors to validate real‑world usability enhancements before broad commercial launch.

Product Management — Prioritize modular architectures and energy‑efficient switch‑mode designs; accelerate platforms that support remote calibration and instrumentation APIs.

Supply Chain — Build alternative sourcing for copper and magnetics; qualify regional calibration/service partners to offset labor shocks and reduce cross‑border logistics risk.

Sales & Channel — Differentiate on service SLAs and long‑term TCO modeling rather than headline price; develop vertical propositions for EV validation rigs and semiconductor fabs.

M&A — Target software and automation assets that accelerate instrument‑level telemetry, calibration automation, and fleet management, rather than purely hardware bolt‑ons.

Boards and executive teams will need concise, executable options amid increased vendor activity and shifting input costs. This study is structured to support three common planning use cases:

Capital allocation — quantitative scenario models show how different investment paths (R&D in SiC integration, service network expansion, or channel incentives) affect EBIT and payback in core markets.

Commercial strategy — playbooks translate market signals into go‑to‑market actions, including differentiated warranty structures, bundled software subscriptions, and calibration-as‑a‑service offerings.

M&A and partnership screening — an actionable scorecard shortlists targets by strategic fit, execution risk, and expected synergies, reducing the diligence timeline and improving negotiation posture.

In keeping with the “trailer” principle of this briefing, we deliberately do not publish the report’s detailed segment revenue splits, regional breakdowns, or application‑level share tables in this announcement. The full dataset, sensitivity matrices, and downloadable models are available in the comprehensive report. That level of granularity is essential for transactional work (pricing negotiations, bid structuring, target valuation) and is therefore reserved for subscribers and licensed users.

If your organisation needs to align R&D roadmaps, re‑frame product economics, or run a targeted M&A screen in 2026, PW Consulting’s Benchtop Power Supplies Market report provides the scenario models, vendor benchmarks and the implementation checklists required to move quickly and confidently. Clients who subscribe before Q2 2026 gain access to a tailored briefing and a 30‑point strategic action plan mapped to their stated priorities.

For a summary of methodologies, a sample executive dashboard and details on customization options, request access to the full report through PW Consulting’s publications portal. Our analysts are available to present a leadership briefing and to assist with bespoke scenario modelling for board workshops and investor diligence.

For detailed analysis of this topic, please visit the official page:Benchtop Power Supplies Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com