Velashape 3 Treatment in Dubai: Your Guide to Firm Skin

Health |

2026-04-06 10:06:05

PW Consulting today releases a strategic preview of our forthcoming Arthroscopy Irrigation Pumps Market report — a pragmatic, decision-focused analysis crafted for C-suite leaders, corporate development teams, product strategists and procurement executives preparing for 2026. Built on a historical baseline (2020–2025) and a detailed forecast through 2026–2032, the study synthesizes market sizing, regulatory context, competitive dynamics and actionable playbooks that translate market intelligence into executable plans.

Arthroscopy Irrigation Pumps Market

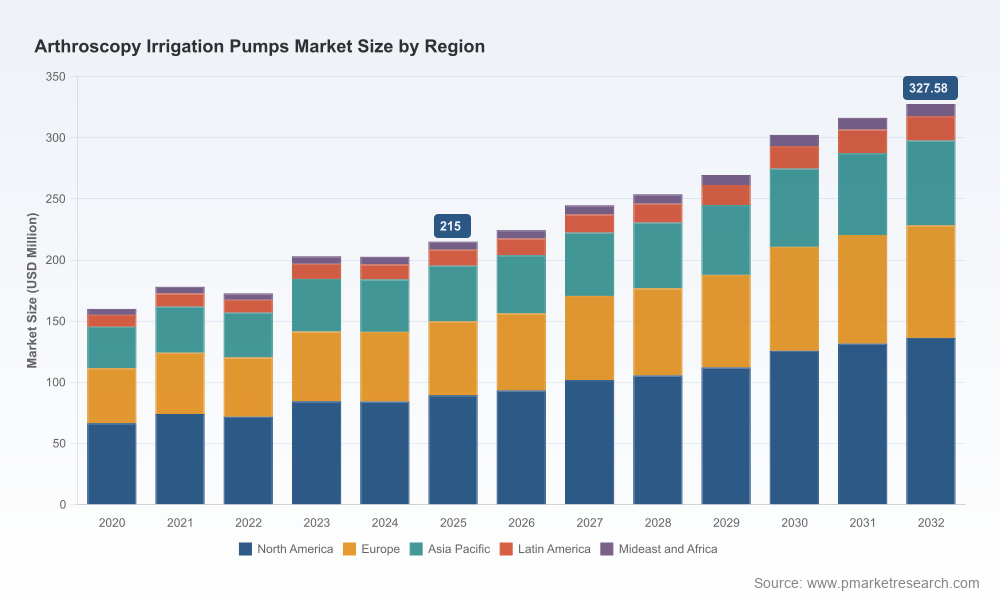

Market momentum: Our market model shows the arthroscopy irrigation pumps market expanding at a steady compound annual growth rate (CAGR) of 6.2% over the forecast horizon. From the report base year (2025) through 2032, the market grows meaningfully — a trajectory that underpins both product investment cases and consolidation scenarios.

Arthroscopy Irrigation Pumps Market

Scale and runway: With a robust historical dataset (2020–2025) and a seven-year forecast, PW Consulting quantifies near-term demand drivers while flagging inflection points that will shape procurement cycles, capital allocation and partnership strategies in 2026.

Arthroscopy Irrigation Pumps Market

Concentration profile: The market exhibits a high degree of concentration (CR3 ≈ 65.4%; CR5 ≈ 82.1%), indicating that a small set of incumbents commands the majority of commercial activity. This concentration has direct implications for competitive response, channel negotiation and M&A valuation in the coming year.

Timing of resource allocation — R&D and commercialization: The projected growth path provides the quantitative basis to prioritize investment in next-generation fluid management capabilities (e.g., integrated visualization, closed-loop pressure control, battery-powered portability). Our analysis identifies when incremental demand justifies increased R&D spending versus when OEMs should defer to modular partnerships or licensing.

Portfolio optimization: For medical device companies and hospital procurement groups, the report distills which product attributes are becoming table stakes (e.g., reliability, user interface ergonomics, infection-control features) and which characteristics create differential pricing power. This helps determine where to prune, invest or acquire.

M&A and JV playbooks: Given the market’s high concentration, bolt-on acquisitions and strategic joint ventures remain attractive routes to scale. Our scenario-driven valuation guidance and integration roadmaps are designed for deal teams preparing bids in 2026.

Channel & pricing strategy: With increasing adoption of integrated systems by leading institutions, the report outlines contracting levers — from bundled capital-plus-consumables models to outcome-based agreements — that can be operationalized in 2026 to protect margins and accelerate adoption.

The full report is built to be operational. It moves beyond description to provide tools and templates that executives can act on immediately:

Robust market model: Historical reconciliation (2020–2025) and granular scenario forecasts (2026–2032) with sensitivity testing to support capex and revenue planning.

Adoption drivers and inhibitors: Deep analysis of clinical workflows, hospital procurement cycles, reimbursement trends, and the interplay between device performance and OR throughput.

Regulatory and reimbursement playbook: A practical compliance checklist for FDA 21 CFR 888.1111 pathways, 510(k) considerations, and EU MDR readiness. We map likely regulatory timelines and corresponding go-to-market actions.

Commercial playbooks: Contract templates and negotiation tactics for hospitals and health systems, distributor selection criteria, and a phased launch plan for new products (pilot → scale → national roll-out).

Technology assessment: An evidence-based framework to evaluate pump technologies — from electronic closed-loop systems to manual/gravity-fed platforms — against clinical KPIs (visualization reliability, pressure stability, fluid clarity) and total cost of ownership.

Supply chain resilience checklist: Practical steps to mitigate single-source risks, reduce lead-times for critical components, and structure supplier SLAs to protect uptime in high-volume arthroscopy centers.

Investor/M&A dossier: Target scoring templates, integration risk heatmaps, and accretion/dilution models tailored to strategic acquirers and private equity sponsors.

The market is anchored by established orthopedic and endoscopy OEMs alongside niche specialists and regional manufacturers. PW Consulting’s competitive chapter profiles each major player with strategic implications rather than raw market share tables — helping executives understand intent, capability and likely next moves.

Arthrex, Inc. (Naples, Florida): Known for systems such as Continuous Wave™ 4 and DualWave™, Arthrex emphasizes integrated fluid management and visualization. The company’s May 2025 launch of a next-generation integrated system signals a strategic push to converge pump performance with imaging and procedural workflow — a direct bid to capture value further up the OR stack.

Stryker Corporation (Kalamazoo, Michigan): Stryker’s CrossFlow and FloSteady offerings, coupled with ReconiSense suction optimization, reinforce the company’s systems-led approach. The March 2025 contract win with a major U.S. health system underlines Stryker’s channel strength and bundling capabilities — a trend we expect will accelerate competitive contracting in 2026.

Smith & Nephew plc (London): With products like the DOUBLEFLO inflow/outflow pump (manufactured by Hemodia), Smith & Nephew’s positioning focuses on consistent debris removal and sports medicine workflows. Their strategy highlights clinical partnerships and OEM co-development as a rapid route to differentiated field performance.

CONMED Corporation (Utica, New York): The CrystalView™ Pro system exemplifies a configurable, high-performance approach intended to attract hospitals seeking flexibility. CONMED’s playbook centers on reliability and customization for OR teams that prioritize predictable joint distention.

Richard Wolf and KARL STORZ (Germany): Both vendors integrate pump systems into broader endoscopy portfolios, using cross-sell dynamics to strengthen customer relationships. Their value proposition emphasizes integration, serviceability and long-term maintenance agreements.

Hemodia (France) and regional suppliers (e.g., Advin Healthcare, JD Meditech): These firms compete on focused engineering, cost-effective designs and regional distribution networks. Their presence highlights a bifurcated market: premium integrated systems versus cost-sensitive, high-volume offerings.

Strategic takeaways: incumbents are leveraging system integration and service models to lock in customers, while regional manufacturers exert price pressure in cost-sensitive segments. Expect intensified bundling and field-service commitments in 2026 as major suppliers defend and extend their installed bases.

Regulatory guardrails: Arthroscopy pumps are regulated as arthroscope accessories under standards such as FDA 21 CFR 888.1111 and must typically navigate 510(k) clearances. The EU MDR continues to raise the bar for conformity and post-market surveillance, making regulatory readiness a non-negotiable element of product launch timing.

Reimbursement trends: Favorable Medicare reimbursement policies for arthroscopic procedures have historically supported device adoption. Our modeling links reimbursement trajectories to hospital investment willingness, showing clear inflection points where improved payments accelerate technology refresh cycles.

Clinical workflow drivers: Adoption is driven by demonstrable improvements in visualization, reduced OR time, and predictable fluid handling that minimizes complications. The report synthesizes clinical literature with frontline OR interviews to quantify these performance thresholds.

For OEMs: Prioritize integration features that directly reduce OR time and enhance visualization. Invest selectively in battery- and software-enabled differentiation that can be monetized through service contracts.

For Hospitals and Health Systems: Leverage purchasing cycles to negotiate bundled commitments that include uptime guarantees and outcome-based clauses. Run focused pilots to validate new integrated systems before large-scale rollouts.

For Investors and M&A Teams: Target targets with complementary service capabilities or regional distribution networks. Use our valuation scenarios to stress-test acquisition return profiles under multiple adoption-rate assumptions.

For Regulators and Compliance Teams: Prepare for MDR and 510(k) timelines by front-loading clinical and usability data collection to avoid launch delays in 2026.

This release is a high-level, decision-oriented preview — designed to surface the strategic choices executives face in 2026. It intentionally omits detailed segmentation tables and certain proprietary splits to preserve the commercial value of our full analysis. The complete PW Consulting Arthroscopy Irrigation Pumps Market report contains the granular segmentation, pricing curves, vendor scorecards, downloadable financial models and negotiation templates required to operationalize 2026 plans.

For executives preparing budgets, acquisition targets, or product roadmaps in 2026, the report provides the empirical backbone and the practical instruments to act decisively. Contact PW Consulting to request the full report, licensing options, or a tailored briefing that maps our findings directly to your strategic agenda.

For detailed analysis of this topic, please visit the official page:Arthroscopy Irrigation Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com