What's Driving the Next Wave of Innovation in Antiviral Drug Development?

Networking |

2026-06-08 06:25:55

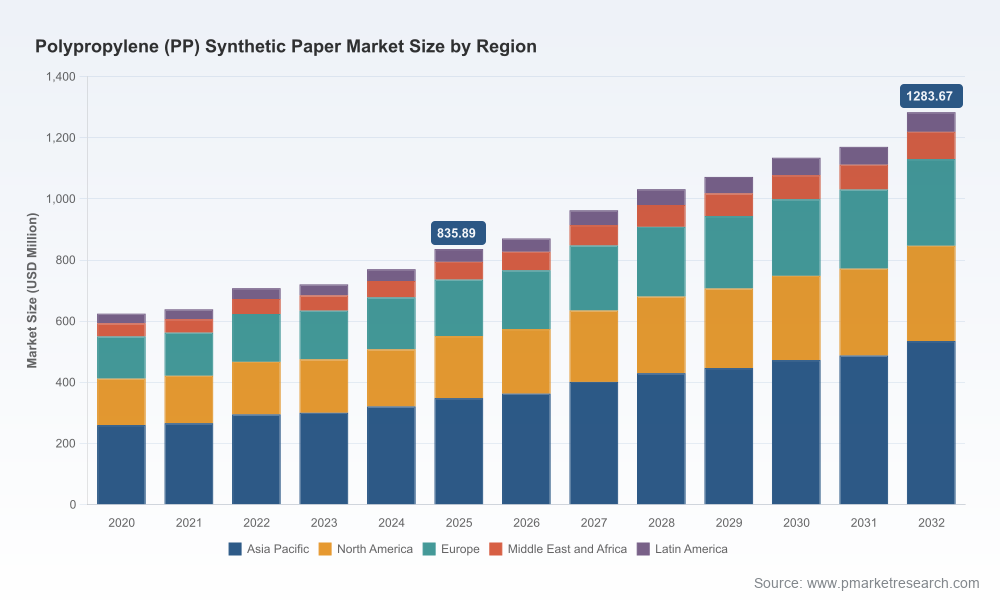

As stakeholders across packaging, labeling, specialty printing, and technical substrates prepare their 2026 playbooks, PW Consulting’s latest Polypropylene (PP) Synthetic Paper Market report provides a focused, operational roadmap built on an updated market model, supplier intelligence, and scenario-ready strategy options. Our analysis shows a resilient market trajectory: after a five-year expansion through 2025, the market is projected to continue growing at a mid-single-digit compound annual growth rate (CAGR) through the 2026–2032 forecast window, reflecting both steady end-use demand and accelerating substitution of traditional fiber-based papers in durability-driven applications.

Polypropylene Pp Synthetic Paper Market

Actionable foresight: We translate market momentum into clear decision levers for procurement, product, and corporate strategy teams — from raw material hedging to differentiated product development.

Polypropylene Pp Synthetic Paper Market

Validated market sizing: Our model tracks the market from 2020 through 2025 and extends to 2032, enabling planning horizons aligned to capital cycles and multi-year contracts.

Polypropylene Pp Synthetic Paper Market

Competitive clarity without data leakage: We map supplier capabilities, capacity footprints, and innovation pathways while deliberately withholding granular segment shares and proprietary pricing curves to protect commercial sensitivity and to guide readers to the full report for transaction-grade intelligence.

PW Consulting’s base-year analysis (2025) verifies consistent market expansion across 2020–2025 followed by continued growth in our 2026–2032 forecast. The market’s structural dynamics — resilient end-use demand, product innovation in printability and durability, and an emerging sustainability narrative — underpin a multi-year growth path. Our concentration analysis shows a moderately consolidated supplier landscape, with the top three and top five firms collectively representing meaningful shares of global supply, underscoring both competitive intensity and opportunities for scale-driven players to defend margins.

Durability-led substitution: Increased demand for water-, tear-, and chemical-resistant substrates in labeling, outdoor graphics, and long-life documentation is driving adoption over coated fiber papers and PVC-based alternatives.

Print technology alignment: Advances from print OEMs (digital and UV/inkjet) are expanding addressable use cases; substrate suppliers that certify and co-develop with print platforms will capture premium volumes.

Sustainability and compliance: Regulatory expectations and corporate pledges are raising the bar on recyclability, restricted substances, and lifecycle claims — firms with audited environmental management systems and documented material restrictions are better positioned to access institutional procurement.

Feedstock volatility and margin pressure: Polyolefin feedstock costs and feedstock-related inputs remain a primary input risk. Short-term spikes tied to crude/naphtha cycles and regional propylene tightness have been observed; buyers and producers must embed dynamic cost models into pricing and procurement strategies.

Scale and customization: Ability to offer a spectrum of grades (coated, uncoated, orientation/film-based, thickness variants) and to provide converter-friendly formats is becoming a differentiator in supplier selection.

The market is populated by established specialty manufacturers alongside large polymer film producers that have extended portfolios into synthetic papers. Key industry players combine brand recognition, certification-backed claims, and channel reach. Strategic takeaways for 2026:

Leading specialty brands emphasize product systemization: Dedicated product families optimized for specific print technologies and end-use conditions deliver higher conversion rates and lower customer technical friction.

Integrated polymer groups leverage scale: Large polymer manufacturers with in-house film/PP capabilities can compete on cost and rapid capacity response, especially where vertical integration reduces exposure to external resin supply shocks.

Regional champions exploit proximity advantages: Near-market production and distribution solve logistics and lead-time challenges in time-sensitive labeling and packaging supply chains.

Innovation differentiators include coatings and topcoats that improve ink adhesion, specialty formulations for thermal or security applications, and grades that meet stringent food-contact or medical standards.

Trade show and OEM engagement: Ongoing participation by major suppliers at global exhibitions and labeling shows indicates active commercial acceleration and channel development — expect announcements of certified grades and partnership-driven go-to-market plays throughout 2026.

Product line expansion: Continued launches and capacity rollouts of thicker, high-brightness, and print-optimized grades show supplier focus on high-value applications such as premium packaging and secure documents.

Operational and environmental credentials: Manufacturers publicly reinforcing environmental management certifications and substance restrictions are positioning for procurement mandates and large corporate tenders.

Market model and dashboard: Historical and forecast market sizing with sensitivity scenarios, plus an interactive dashboard for scenario toggling across demand, feedstock, and adoption assumptions.

Supply chain heatmaps: Capacity footprints, converter networks, and logistics risk layers for prioritizing nearshoring, dual-sourcing, and buffer inventory strategies.

Raw-material scenario suite: Price-path stress tests and margin impact analyses that translate feedstock volatility into actionable pricing and sourcing plays.

Commercial playbooks: Product positioning templates, channel strategies, and value-based pricing approaches tailored to labeling, packaging, commercial print, and specialty segments.

Regulatory and sustainability toolkit: Compliance checklists, green credential validation pathways, and lifecycle assessment (LCA) inputs to support procurement RFPs and ESG disclosures.

Competitive intelligence annex: Firm profiles, capability matrices, recent developments, and M&A watchpoints, designed to support vendor selection and partnership diligence.

Investment and M&A framework: Deal-screening criteria, integration risk indicators, and contribution-to-value models specific to synthetic paper and adjacent film assets.

Adopt a hybrid procurement stance: Combine long-term offtakes for volume stability with agile spot exposure to capture favorable feedstock drops. Embed monthly recalibration triggers tied to verified polymer indices.

Pursue technical partnerships: Co-develop certified grades with major digital and UV ink OEMs to shorten adoption cycles and to secure preferential conversion support from print houses and converters.

Differentiate with validated sustainability: Prioritize suppliers with audited environmental systems and transparent substance management; quantify customer-facing sustainability benefits through unit-level LCAs.

Segment go-to-market by application economics: Reserve premium, higher-margin grades for long-life and security applications while using cost-optimized film-based papers for high-volume labels and packaging.

Invest in converter enablement: Technical support, sample programs, and co-marketing with converters materially reduce switching friction and accelerate trials.

Prepare for consolidation and partnership plays: With moderate market concentration, 2026–2028 may present attractive M&A and JV opportunities for firms seeking rapid scale or technology access.

Feedstock price spikes: Mitigate through blended procurement windows, indexed contract clauses, and limited strategic reserves.

Regulatory shifts: Maintain an environmental and compliance roadmap, prioritize suppliers with certifications, and monitor material-restriction developments that impact market access.

Technological obsolescence: Invest in continual co-development with print OEMs and invest in R&D for coatings and topcoats that extend compatibility across print platforms.

Reputational and sustainability risk: Ensure transparent labeling of recyclability claims and back them with third-party verification to avoid greenwashing exposure.

Procurement teams should operationalize the report’s price-sensitivity scenarios into quarterly sourcing strategies. Product managers should prioritize two to three grade upgrades or certifications in their 2026 roadmaps. Strategy and corporate development teams should use our M&A framework to build watchlists and to stress-test accretive targets under different feedstock and demand scenarios.

PW Consulting’s release is intentionally a strategic preview: we have showcased core insights and the decision framework necessary for 2026 planning while withholding transaction-level segmentation and granular regional/application splits in this public brief. The full report contains detailed segment models, interactive forecasting files, supplier scorecards, and convertor-validated use-case ROI calculators — essential tools for deal teams, procurement, and product leadership preparing for 2026 execution.

For organizations seeking prioritized briefings, scenario walkthroughs, or bespoke advisory (procurement optimization, supplier due diligence, or M&A support), PW Consulting is scheduling in-depth workshops in Q2 2026 to translate these insights into executable plans.

For detailed analysis of this topic, please visit the official page:Polypropylene Pp Synthetic Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com