Sanitary Taps Market: Insights, Key Players, and Growth Analysis

Other |

2026-03-16 06:22:58

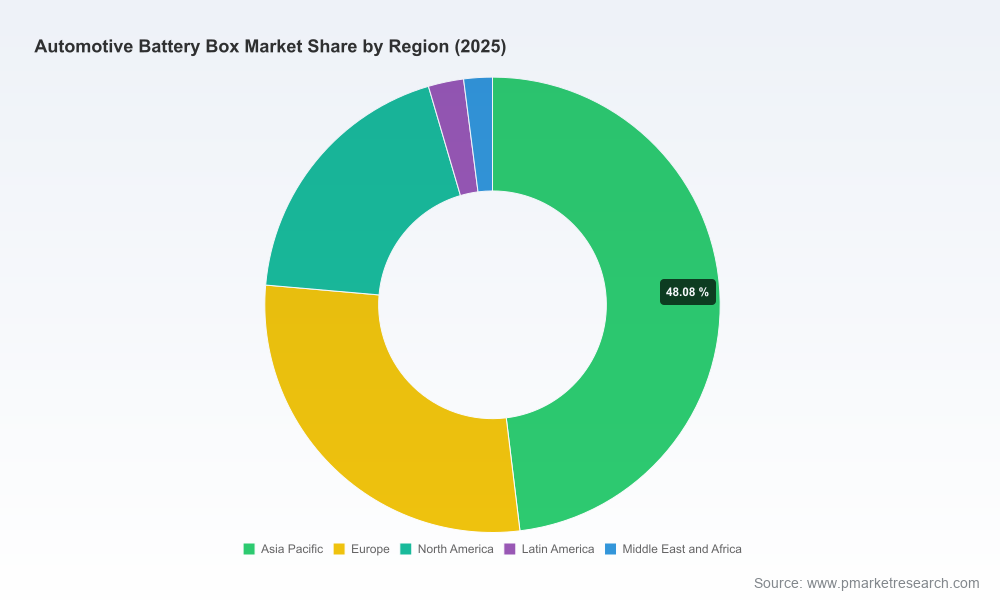

PW Consulting’s latest Automotive Battery Box Market Research—anchored on a 2025 base year and a 2026–2032 forecast horizon—translates accelerating electrification into concrete decision levers for executives planning 2026 programs. The sector has moved from niche engineering projects into mainstream manufacturing: total market value more than doubled from the start of the decade and reached roughly USD 6.45 billion in 2025. With a projected compound annual growth rate (CAGR) of 18.52% through 2032, PW Consulting’s report converts these headline dynamics into operational playbooks for procurement, product strategy, manufacturing footprint, and M&A decisions.

Automotive Battery Box Market Research

Volume momentum meets technical complexity. OEM ramp plans and cell-to-pack architectures are increasing both enclosure volume and integration requirements; decisions made in 2026 about supplier selection, material strategy, and test protocols will set multi-year cost and safety trajectories.

Automotive Battery Box Market Research

Material innovation is changing the economics. Aluminum-intensive designs, advanced composites, and new thermoplastic grades are shifting mass, safety, and manufacturing trade-offs—creating a bifurcation between low-cost stamped/formed steel solutions and higher-value, lighter designs that enable greater vehicle range or packaging flexibility.

Automotive Battery Box Market Research

Regulation and certification are maturing. New test standards and lifecycle requirements are already influencing supplier qualification pipelines; readiness to pass material screening and battery-enclosure-specific protocols is becoming a gating factor for high-volume supply awards.

Market scale and trajectory: The battery box market has grown rapidly through 2020–2025 and is forecasted to expand substantially over the 2026–2032 period, reaching north of USD 21 billion by 2032 under our base scenario, reflecting a robust CAGR of 18.52%.

Supplier concentration: Market concentration shows that the top three suppliers account for around 42% of industry revenue while the top five account for roughly 58%—a structure that combines global players with specialized niche suppliers, producing both competitive pressure and partnership opportunities for newcomers.

Material mix and cost sensitivity: Aluminium-intensive approaches, composites, and advanced thermoplastics are each commercially viable paths; their relative adoption will be driven by vehicle architecture, safety/thermal-performance trade-offs, and absolute cost curves that vary by region and scale.

Full market model (2020–2032) with scenario-based forecasts, enabling sensitivity testing for cell format, vehicle mix, and adoption curves.

Discrete supplier profiling and capability maps: engineering competencies, manufacturing footprints, tooling strategies, and certification readiness to support rapid supplier shortlisting.

Unit-cost-driver framework and benchmarked BOM breakdowns to run build-versus-buy and make-versus-buy analyses under different volume assumptions.

Regulatory & safety matrix: mapping UL-style material screening and regional battery rules (including EU lifecycle requirements) against supplier certification status and test requirements.

Manufacturing scale playbook: CAPEX/OPEX templates, cycle-time levers, and modularization pathways to accelerate ramp while preserving quality.

M&A and partnership scorecards, with integration playbooks tuned to preserve IP and accelerate productization of new materials or configurations.

Executive dashboards and procurement negotiation scripts that translate technical differences into commercial levers for 2026 sourcing rounds.

The market is being shaped by a mix of large-tier suppliers with global reach and material specialists introducing disruptive enclosures. Our report synthesizes public disclosures, primary interviews, and factory visits to create decision-ready supplier comparisons.

Magna International Inc. (Aurora, Canada) — Magna brings integrated engineering and production scale, offering steel, aluminium and one-piece OPTiForm solutions. Their footprint in Europe and North America positions them as a logical partner for OEMs seeking global harmonization in enclosure platforms.

Novelis Inc. (Atlanta, USA) — Novelis’ second-generation aluminium-intensive enclosures (Advanz™ s650) highlight the material-performance frontier: significant mass reductions and high frame-efficiency that translate directly into range gains and structural integration opportunities for OEMs pursuing lightweighting at scale.

SGL Carbon (Wiesbaden, Germany) — SGL has demonstrated that carbon- and glass-fibre-based composite enclosures are manufacturable at automotive serial volumes, providing a pathway for premium segments where mass saving and high stiffness justify material cost.

Teijin Mobility (Japan) — Teijin’s multi-material expertise allows enclosures to be engineered for combined impact, thermal and electrical protection—useful for customers seeking integrated solutions rather than a parts supply relationship.

Constellium (Paris, France) — As a supplier capable of cast, extruded and sheet aluminium, Constellium offers design flexibility and crash management capabilities valuable for OEMs with stringent structural targets.

Kautex (Textron) (Bonn, Germany) — Kautex’s Pentatonic™ composite enclosures target the cell-to-pack trend, providing lightweight, monolithic solutions suitable for modular production strategies.

Trinseo (Berwyn, USA) — Trinseo’s halogen- and PFAS-free flame-retardant thermoplastic grades enable rapid cycle manufacturing and recyclability advantages, increasingly relevant for OEMs pursuing sustainable material roadmaps.

voestalpine Metal Forming, BENTELER, and Linamar — These established formed-metal and modular-tray manufacturers provide proven volume manufacturing technologies and program execution experience important for tight ramp schedules and automotive qualification cycles.

Material certification is converging: independent screening services—such as UL’s battery enclosure material screening—are becoming core to supplier qualification. Expect OEMs to demand tested material stacks rather than supplier assurances alone.

Regulatory pressure is increasing: lifecycle rules that extend into recycling and digital passports are elevating the importance of material traceability and end-of-life planning in supplier selection.

Componentization vs. integration debate continues: cell-to-pack approaches compress part-count but require enclosure suppliers to integrate thermal, electrical and mechanical functions earlier in the design cycle.

Recent industry moves underline the pace of commercialisation: major contract awards and new production facilities announced through 2025–2026 show that capacity commitments are being traded ahead of final cell technology convergence—creating first-mover advantages for certain suppliers.

Adopt a material-agnostic sourcing playbook: qualify at least two enclosure technologies (e.g., aluminium-intensive and thermoplastic/composite) to preserve optionality as cell formats and safety requirements evolve.

Insist on independent material screening and a regulatory readiness plan tied to contract milestones—be explicit about UL-style test pass-through and EU lifecycle documentation requirements.

Embed supplier capability metrics in RFPs: request demonstrated cycle-times, scrap rates, and previous ramp performance rather than just quoted lead-times.

Pursue manufacturing proximity for high-volume programs to reduce logistics and synchronization risk—consider co-investment or captive tooling agreements to secure capacity.

Use the report’s cost-model templates to stress-test scenarios for material price shocks, rising freight costs, and differing recycling credits—turn qualitative supply risks into quantified margin impacts.

Companies that treat battery enclosures as a strategic system—rather than a commoditized box—will capture a disproportionate share of value in 2026 and beyond. PW Consulting’s Automotive Battery Box Market Research delivers the quantitative backbone (market sizing, concentration metrics, and forecast scenarios) and the operational toolset (supplier scorecards, cost models, and certification roadmaps) required to convert market growth into defensible commercial advantage. This document is purpose-built to inform sourcing decisions, design trade-offs, plant investments, and M&A activity in the critical 2026 planning window.

To access the full dataset, granular segment breakouts, supplier scorecards and downloadable modelling tools, visit our report page and download the complete intelligence pack—designed to turn 2026’s momentum into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Automotive Battery Box Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com