Oligonucleotide Therapeutics Market: Insights and Competitive Analysis

Other |

2026-05-04 03:39:58

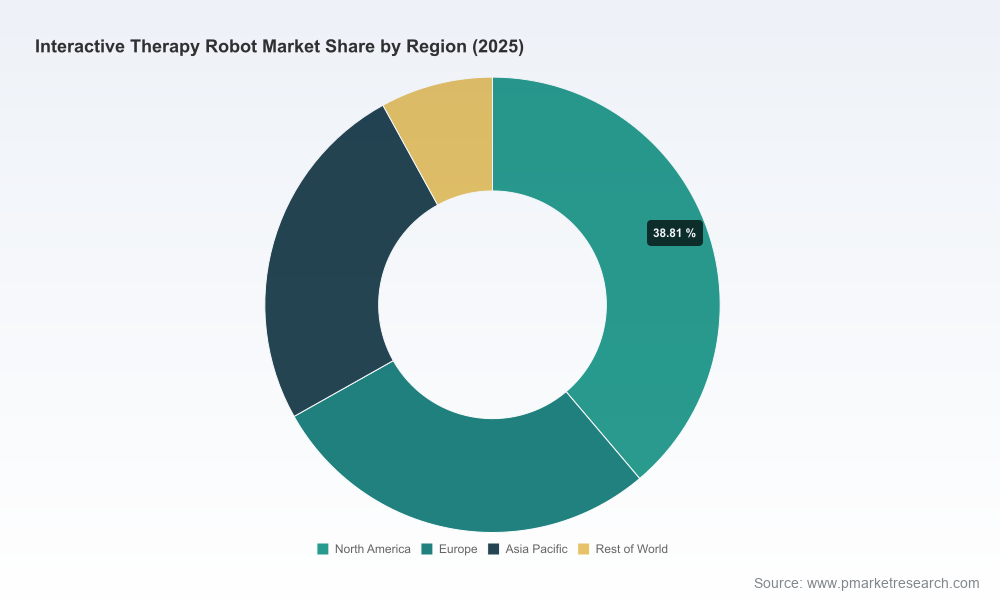

PW Consulting today releases a strategic preview of its deep-dive market intelligence on the Interactive Therapy Robot market, designed to guide corporate decision-making for 2026 and beyond. The market has entered a rapid commercialization phase: after accelerating from a modest base in 2020, total industry revenue reached approximately USD 1.59 billion in our 2025 base year and is forecast to exceed USD 1.89 billion in 2026. Underlying this expansion is a robust compound annual growth rate of 18.5% across the 2026–2032 forecast window, projecting a multi‑billion dollar opportunity by the end of the decade.

Interactive Therapy Robot Market

Market inflection point: The convergence of proven clinical pilots, aging demographics, and digital therapeutic models has shifted interactive therapy robots from experimental pilots to line‑of‑sight commercial deployments. Companies that define clear product–market fit in 2026 will capture disproportionate share as adoption scales through 2027–2030.

Interactive Therapy Robot Market

Policy and reimbursement dynamics are changing go‑to‑market economics: Recent updates to therapy-related billing (including new Remote Therapeutic Monitoring-related codes in the 2026 CPT updates) materially affect unit economics and payor pathways for device-enabled therapy delivery.

Interactive Therapy Robot Market

Regulatory clarity is resolving uncertainty: Classifications and pathways—ranging from lower‑risk emotionally assistive devices to FDA Class II designations for biofeedback instruments—are shaping product design, claims strategy, and timelines to commercialization.

PW Consulting’s topline model captures an industry that more than doubled in revenue from the early 2020s to the 2025 base year, reflecting increasing clinical acceptance and commercial roll‑outs. The forecasted growth trajectory—an 18.5% CAGR through 2032—signals sustained investment opportunity, but also increasing competitive intensity as incumbents and specialist challengers vie for scale. Importantly, market concentration metrics indicate the space is neither a fragmented fringe nor a tightly consolidated oligopoly: the top three firms command a meaningful share of the market while the top five consolidate an even larger portion, implying an environment in which partnerships and strategic M&A will be decisive.

Leading vendors illustrate a diversity of strategic approaches—specialist therapeutic devices, socially assistive AI companions, humanoid and expressive platforms—each with distinct value propositions for hospitals, long‑term care, pediatrics, and home care. Key profiles from our competitive scan include:

PARO Robots (AIST / PARO Robots U.S., Inc.): A pioneer whose therapeutic seal robot has secured clinical acceptance and regulatory classification as a medical device in the U.S. market. PARO’s FDA Class II status provides a blueprint for firms aiming for formal clinical positioning and claims that support integration into institutional procurement.

Intuition Robotics: Focused on AI companionship with ElliQ, targeting loneliness mitigation and engagement in home settings. Their strength lies in user-centered AI, long‑term engagement metrics, and an ecosystem approach to senior care.

Expper Technologies (Robin): Demonstrating strong hospital and nursing home traction with child‑like therapeutic avatars; recent deployments in 2025 show the power of targeted clinical pilots to accelerate institutional adoption.

SoftBank Robotics, Blue Frog Robotics, LuxAI, Hanson Robotics: Each brings platform, humanoid, or social-robot capabilities—competing across therapy, social engagement, and cognitive support use cases with varying emphases on hardware standardization, voice/gesture interfaces, and developer ecosystems.

From a strategic perspective, incumbent device makers and pure‑play robotics firms are diverging on priorities: leaders are monetizing integrated solutions with clinical evidence and reimbursement pathways, while challengers leverage agility, AI, and local value‑added services to win pilots. Successful 2026 strategies balance clinical validation with pragmatic implementation support—training, data integration, and outcome measurement.

Two regulatory and payor developments are particularly consequential for near‑term strategy:

Regulatory classification paths: Therapeutic robots that make clinical claims or provide biofeedback are being assessed under medical device frameworks (e.g., U.S. FDA, EU MDR), as demonstrated by current device classifications in market. Conversely, emotionally assistive robots that focus on engagement without diagnostic claims tend to follow lower‑risk pathways—but their labeling and intended use statements must be tightly managed to avoid reclassification risk.

Reimbursement code evolution: The 2026 CPT landscape has added and clarified codes for Remote Therapeutic Monitoring and related digital therapeutic interactions. These changes materially improve reimbursement feasibility for device‑enabled therapy services and create new monetization routes (subscription, outcome‑based contracts, payor partnerships) that did not exist a few years ago.

Adoption is driven by three linked buyer priorities: demonstrable clinical outcomes, operational ease of integration, and transparent ROI that aligns with institutional budgeting cycles. PW Consulting’s field work and case studies show procurement committees demand:

Clinical evidence tied to measurable endpoints (reduced agitation, improved engagement, therapy adherence), ideally from randomized or real‑world controlled pilots;

Interoperability with electronic health records and therapy workflows to minimize staff burden;

Flexible commercial models (capex vs. opex, pilot‑to‑scale pathways, outcome‑linked pricing) that mitigate procurement risk.

For vendors, the priority in 2026 should be building fast‑to‑deploy solutions that include turnkey training, KPIs for pilot success, and a clear path to reimbursement capture. For strategic investors and health system partners, the emphasis should be on proof points that convert pilots into multi‑site rollouts within 12–24 months.

This market brief previews a comprehensive report structured to support tactical and strategic decision‑making. Highlights include:

Proprietary market model and forecast methodology calibrated to a 2025 base year with scenario analysis through 2032, enabling stress‑testing of product and pricing strategies;

Competitive landscape maps with capability matrices, go‑to‑market archetypes, and recommended partnership plays;

Regulatory and reimbursement playbooks that translate policy changes into actionable commercialization steps;

Five operational playbooks—pilots, procurement, clinical validation, data integration, and scale‑up—each with checklists, KPI templates, and sample contract language;

Investment and M&A diagnostic tools to evaluate target fit based on technology defensibility, clinical evidence, and go‑to‑market traction;

Real‑world case studies and a library of pilot results that illustrate successful pathways from single‑site proof to enterprise deployment.

Note: As a “trailer” to the full intelligence suite, this press release intentionally omits the granular segmentation tables and line‑item regional and application revenue figures that accompany the complete report. Those detailed breakdowns—essential for target selection and P&L modeling—are available only in the full report and associated data appendices.

Prioritize “evidence‑first” commercialization: allocate resources to pilots that can generate publishable outcome data within 6–12 months and be prepared to convert pilots into bundled commercial offers tied to reimbursement codes.

Design modular go‑to‑market offerings: combine device, software updates, clinician onboarding, and outcome reporting to reduce deployment friction and justify premium pricing.

Invest early in regulatory clarity: classify your product and claims trajectory clearly—either as an assistive consumer device or as a medical device—so regulatory strategy does not become a gating factor for procurement.

Forge partnerships across ecosystems: health systems, payors, and therapy networks are the channels through which scale will be realized. Strategic partnerships or acqui‑hires will accelerate access to clinical pathways and reimbursement capture.

Prepare for consolidation: given the current concentration dynamics, expect increased M&A and strategic roll‑ups; build defensive and offensive scenarios into 2026 business planning.

Clinical platform play: Firms with the ability to generate consistent clinical outcomes will bundle device, analytics, and therapy services into subscription models that align financial incentives with care outcomes.

Specialist verticalization: Vendors targeting specific clinical niches (pediatrics, dementia care, post‑acute rehabilitation) will accelerate adoption through targeted evidence generation and payer contracting.

Partnership orchestration: Technology providers will seek early alliances with EMR vendors, therapy networks, and payors to reduce integration friction and enable outcome‑based contracting.

Interactive therapy robots are transitioning from innovation showcase to pragmatic clinical and commercial assets. The 2026 decision window will determine whether vendors harness regulatory clarity, reimbursement levers, and evidence generation to capture long‑term value—or cede ground to better capitalized or more clinically attuned competitors. PW Consulting’s full Interactive Therapy Robot Market report provides the granular segmentation, vendor benchmarking, and operational playbooks necessary to execute with confidence.

For C‑suite teams, corporate development groups, health system innovators, and investors seeking the detailed breakdowns, regional and application segmentation, and downloadable data tables that are essential for transaction diligence and market entry planning, PW Consulting’s complete report and Excel model are available through our market research portal. Contact PW Consulting to arrange a briefing, receive the full dataset, or commission tailored scenario analysis for your strategic planning cycle.

For detailed analysis of this topic, please visit the official page:Interactive Therapy Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com