Label Release Paper Market 2026 Preview: Strategic Imperatives from PW Consulting

Executive summary

Our new Label Release Paper Market report, published with a 2025 base year and a 2026–2032 forecast horizon, provides a focused evidence base for commercial, procurement, R&D and M&A decisions through 2026 and beyond. The market has expanded from roughly $7.0 billion in 2020 to about $8.45 billion in 2025 and is projected to grow at a steady mid-single-digit pace (4.1% CAGR) over the forecast window, approaching roughly $11.2 billion by 2032. These headline dynamics disguise important structural shifts—sustainability-driven product substitution, regulatory re‑pricing, and a reshuffling of global supply footprints—that will require calibrated action by manufacturers, brand owners, and converters in 2026.

Label Release Paper Market

Why this matters for 2026 decision-makers

- Procurement and cost management: Volatility in fibre and film inputs, combined with shifting regulatory cost-allocations under producer responsibility regimes, will raise the strategic importance of supplier segmentation, hedging and near‑term contracting flexibility.

- Product strategy and circularity: Advances in recyclable double‑sided silicone liners and low‑basis‑weight glassines are already changing spec sheets for pressure‑sensitive labels and tapes. R&D and commercial teams must align product roadmaps to recyclability requirements and customer sustainability KPIs.

- Capital allocation and capacity planning: Moderate market concentration—where the top three and five suppliers account for meaningful but not overwhelming shares—creates differentiated opportunities for regional investments and bolt‑on consolidation to secure scale.

- Regulatory compliance and market access: Emerging Extended Producer Responsibility (EPR) schemes in multiple jurisdictions will alter total landed costs and product specifications; readiness in 2026 will determine participation and margins in premium channels.

What the report includes — practical, action‑oriented intelligence

PW Consulting’s market study is designed to be a hands‑on toolkit, not an academic summary. Key deliverables tailored for immediate executive use include:

Label Release Paper Market

- Top‑down market sizing and a bottom‑up demand forecasting engine through 2032, with scenario modules that stress test adoption curves for recyclable liners and low‑weight papers.

- Supply‑chain maps and inputs cost curves (fibre, coatings, silicone, PE lamination) with breakouts by manufacturing node to inform sourcing and nearshoring choices.

- Competitive benchmarking and supplier scorecards (capacity, technology readiness, sustainability credentials, customer mix) to guide preferred‑supplier decisions and tender design.

- Commercial playbooks: go‑to‑market propositions for labelstock formulations, price‑pack architecture, and margin recovery strategies under EPR pass‑through constraints.

- CapEx prioritisation tools: ROI and payback models for coating line upgrades, silicone application technologies and film/coating conversions.

- Regulatory readiness checklists and roadmap templates for compliance with recyclability testing and producer responsibility obligations.

Dynamics reshaping the market

Three broad dynamics are acting on current and near‑term demand:

Label Release Paper Market

- Material innovation and recyclability: The industry is moving beyond single‑metric sustainability claims toward demonstrable recyclability. Recent product introductions that achieve paper‑recyclable ratings for double‑sided silicone liners illustrate a step‑change in engineering and testing. These innovations will open adoption pathways for brands demanding verified end‑of‑life performance.

- Regulatory pressure and cost reallocation: A growing number of jurisdictions have implemented or are designing Extended Producer Responsibility frameworks for packaging and paper. These schemes reallocate the cost of collection and recycling back to producers and will interact with procurement and pricing strategies in 2026—creating both cost headwinds and differentiation opportunities for compliant materials.

- Manufacturing and supply risks: Base papers (glassine, SCK, CCK, natural kraft, poly‑coated kraft) and specialty coatings remain the central inputs; practices such as PE lamination persist to control silicone migration. Grammage and substrate choices are being optimized to balance release performance, yield, and recyclability—forcing trade‑offs that procurement and product teams must reconcile.

Competitive landscape — what the leading players reveal about strategy

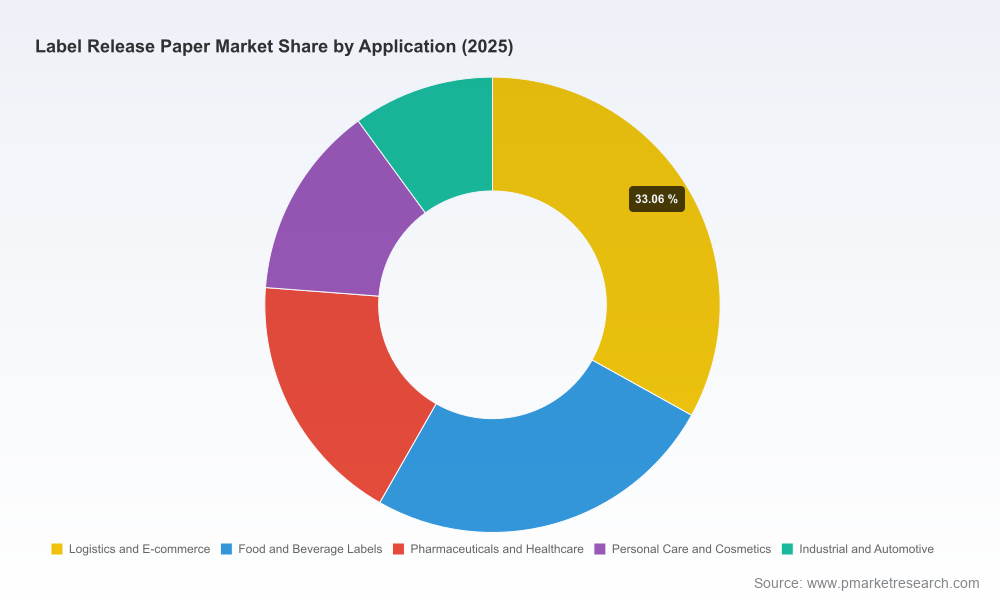

The market exhibits moderate concentration: the three largest firms account for a meaningful share of global capacity and the top five represent less than half of the total, leaving room for regional leaders and specialised innovators. This configuration supports multiple strategic plays, from scale consolidation to niche premiumisation.

- Mondi: As a global packaging and paper producer, Mondi’s integrated footprint and sustainability positioning make it a natural partner for converters and brand owners seeking paper‑based release liners with an emphasis on circularity.

- Loparex: A speciality liner and film producer, Loparex focuses on high‑performance, differentiated substrates and coatings—an attractive profile for industrial and graphics applications where technical performance commands premiums.

- Ahlstrom: The firm’s launch of a double‑sided silicone‑coated fibre-based liner with a paper‑recyclable rating signals that incumbents can achieve both performance and circularity simultaneously—a pivotal development for 2026 product strategies.

- UPM Raflatac and Sappi: Both leverage paper and film portfolios to serve self‑adhesive labelstock markets globally; their scale and cross‑market presence enable rapid commercial roll‑out of new liner variants.

- 3M and LINTEC: These firms bring technological breadth and adhesive system integration; their strength is in offering combined adhesive‑liner solutions and customised formulations for demanding specifications.

- Fox River Associates and regional players: Niche specialists and regional manufacturers (including growing Chinese suppliers) continue to capture demand based on customisation, fast lead times and price competitiveness—an important dynamic for converters operating on tight lead‑time windows.

Recent market activity illustrates both innovation and incremental product optimisation: product launches of low‑basis glassine liners and recyclable double‑sided silicone options have accelerated marketing conversations and early adoption among sustainability‑facing customers.

Strategic playbook for 2026 — immediate and near‑term actions

Based on our analysis, we recommend a prioritized set of moves for leaders seeking to convert macro trends into durable advantage in 2026:

- Immediate (next 6–12 months):

- Run a supplier segmentation and risk audit: identify strategic suppliers vs tactical vendors and build dual‑sourcing for critical base papers and silicone supply.

- Fast‑track compliance pilots: partner with recyclability‑certified liner suppliers to test integration in product lines with brand clients that have aggressive sustainability targets.

- Revise contracting: include clauses for EPR cost pass‑through, volume flexibility and quality KPIs tied to recyclability performance.

- Medium term (12–36 months):

- Invest selectively in coating and converting capabilities that reduce basis weight or enable recyclable double‑sided silicone application, backed by ROI models that incorporate EPR‑driven cost changes.

- Shape go‑to‑market propositions that monetise sustainability cred: premium SKUs, certification packs, and co‑branding opportunities with lead customers.

- Pursue targeted M&A or JV deals to secure regional capacity or technical know‑how—particularly in regions with rising label demand and constrained local supply.

- Longer horizon (36+ months):

- Build product platforms that can be repurposed across label, tape and industrial applications to maximise asset utilisation.

- Partner in upstream fibre and chemical sourcing to stabilise input availability and reduce price volatility exposure.

How PW Consulting’s report creates decision advantage

Our Label Release Paper Market report is engineered as a decision tool for the boardroom and commercial teams entering 2026. We combine robust headline forecasting with operational diagnostics: supply maps, supplier scorecards, commercial negotiation templates, CapEx prioritisation models, and regulatory readiness checklists. The report’s scenario modules let you stress test strategic choices against alternative adoption curves for recyclable liners and varying levels of regulatory stringency.

Conclusion — the strategic vantage for 2026

For firms competing in the label release paper ecosystem, 2026 will be defined less by headline growth than by who captures the value created from sustainability and regulatory transitions. Suppliers that can validate recyclability, secure resilient raw‑material supply, and translate compliance into commercial differentiation will capture outsized returns. Converters and brand owners who proactively redesign supply contracts, invest in compatibility trials and reallocate capex toward flexible converting lines will both mitigate risk and seize market share.

This article outlines the strategic contours of the opportunity. For the granular segmentation, regional dynamics, supplier scorecards and executable templates that your team will need to act in 2026, access the full PW Consulting Label Release Paper Market report at our release page—designed as the operational playbook for executives entering the next phase of industrial transformation.

For detailed analysis of this topic, please visit the official page:Label Release Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com