Hydrogen-Cooled Synchronous Condenser Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive summary

As power systems accelerate the shift from synchronous fossil generation to inverter-dominant renewables, hydrogen-cooled synchronous condensers have emerged as a pragmatic engineering response for high-capacity system-strength needs. PW Consulting’s latest market research — anchored on a 2025 base year and projecting through 2032 — quantifies a market that has expanded materially through the 2020–2025 period and is forecast to continue growing at a compound annual growth rate of 5.86% between 2026 and 2032. Measured on our revenue basis (USD Million), the global market expands from a mid-three-hundred million-dollar base in 2025 toward a substantially larger opportunity by 2032.

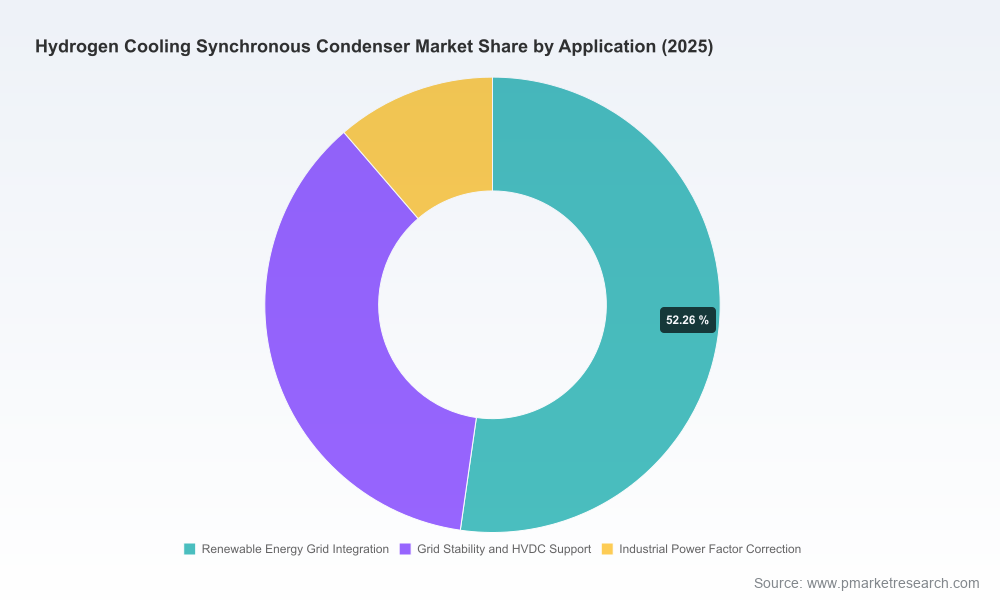

Hydrogen Cooling Synchronous Condenser Market

Why this matters for corporate strategy in 2026

- Timing and scale: Market momentum that consolidated over 2020–2025 continues into 2026. For project developers, OEMs, and grid operators, procurement and manufacturing lead-times mean decisions taken now determine deployment schedules across multiple renewable integration projects planned for the late 2020s.

- Decision risk vs. option value: Choosing hydrogen-cooled architectures brings clear performance upside for high-power ratings and thermal efficiency, but also requires investments in hydrogen handling competence, seal technology, and safety infrastructure. Firms must balance near-term tender competitiveness against longer-term total cost of ownership and system performance.

- Supplier concentration: The market is materially concentrated — the top three suppliers control a large majority of installed capacity while the top five push concentration further. This oligopolistic structure shapes negotiation dynamics, delivery risk, and opportunity for new entrants with differentiated technical or service propositions.

Market trajectory — what the headline numbers tell you

Our report synthesizes historical data from 2020–2025 and builds a detailed projection for 2026–2032. The trajectory shows steady expansion driven by utility-scale renewable integration, transmission reinforcement programs, and targeted state/provincial Renewable Energy Zone initiatives. The headline CAGR of 5.86% across the forecast period captures both ongoing deployments and the gradual acceleration of replacement, retrofit and reinforcement cycles as synchronous generation retires in favor of inverter-based resources.

Hydrogen Cooling Synchronous Condenser Market

Technology and regulatory context

- Technical advantage: Hydrogen as a cooling medium delivers superior thermal conductivity and lower density relative to air, enabling higher continuous ratings for large rotating machines — a factor that becomes decisive where constrained footprint and high MVA ratings are required.

- Operational complexity: Hydrogen systems demand specialized sealing, purity control and leakage-management systems. These operational and safety requirements influence O&M regimes, insurance terms, and lifecycle cost models.

- Regulatory drivers: Grid operators in high-renewable systems are explicitly prioritizing synchronous condensers (including hydrogen-cooled variants) to supply inertia, short-circuit strength and dynamic reactive power. At the same time, some tenders and operators favour non-hydrogen options to sidestep hydrogen handling complexity, creating a bifurcated procurement landscape.

Competitive landscape — who’s shaping the market and how

The hydrogen-cooled synchronous condenser market is populated by long-established rotating-machinery specialists, global power-equipment conglomerates, and agile regional manufacturers. Key industry players maintain a mix of historical experience with hydrogen-cooled designs and recent project activity that signals strategic prioritization:

Hydrogen Cooling Synchronous Condenser Market

- Global incumbents with deep hydrogen-cooled heritage and modular offerings continue to lead in high-MVA, utility-scale contracts. Their value proposition rests on field-proven thermal designs, integrated balance-of-plant capability, and long-term service portfolios.

- Electrical conglomerates that bundle synchronous condenser supply with turnkey grid solutions are winning complex REZ and transmission reinforcement projects by offering integrated engineering, procurement and construction (EPC) capability and system-level warranties.

- Regional manufacturers and newer entrants are leveraging local supply chains and competitive service models to capture retrofit work and regional tenders where delivery speed and local content matter.

Recent contract activity underscores these dynamics. Major contract awards and EPC selections in 2025–2026 across Australia, Brazil, the UK and the U.S. demonstrate active tender pipelines, consortium-based project delivery, and cross-vendor collaboration on complex site deployments. These transactions are practical evidence that hydrogen-cooled technology is being deployed at scale where project-level ratings and thermal performance justify the hydrogen approach.

Practical contents of the PW Consulting report — what you get

This market brief is an executive extract. The full PW Consulting Hydrogen Cooling Synchronous Condenser Market Report provides operationally focused intelligence to support procurement, product strategy, and capital planning, including:

- Methodology and base-data transparency: historical time series, assumptions, and sensitivity testing for macro drivers and technology adoption rates.

- Outlook and scenario analysis: baseline forecasts, upside/downside scenarios reflecting policy shifts, commodity price shocks, and accelerated retirements of synchronous generation.

- Detailed vendor dossiers: capability maps, product features (cooling architectures and control systems), aftermarket and service models, and commercial positioning.

- Procurement playbook: recommended tender language, risk allocation clauses for hydrogen handling, acceptance testing templates, and warranty approaches tailored to high-MVA projects.

- Technical deep dives: hydrogen sealing solutions, purity and leakage management, maintenance protocols, and O&M cost modeling for hydrogen vs. alternative cooling systems.

- Investment and financing guidance: CAPEX/OPEX modelling, life-cycle cost comparisons, and structuring options for EPC, BOOT and servitization contracts.

- Regulatory and safety matrix: compliance checklists, permitting pathways, and insurance implication analysis for hydrogen-cooled installations.

- Case studies: annotated project timelines, commissioning lessons learned, and post-commissioning performance data from recent deployments.

Actionable strategic recommendations for 2026 decision-makers

- Procurement timing: If your project requires ratings above typical air-cooled envelopes or you have constrained footprint requirements, plan procurement windows now. Long lead times for hydrogen-ready rotating machinery and associated balance-of-plant works mean late decisions compress choices and increase premium risk.

- Supplier engagement: Prioritize suppliers with demonstrable hydrogen-cooling heritage, robust service networks and clear spare-parts strategies. Given the market concentration, develop parallel supplier tracks and consider consortium or JV models to diversify delivery risk.

- Capability building: Invest in hydrogen handling competence early — sealing technologies, purity monitoring, emergency response protocols, and vendor-neutral O&M training reduce long-term operational risk and insurance costs.

- Design trade-offs: Use our TCO and sensitivity modules to evaluate hydrogen-cooled vs alternative cooling strategies in your specific grid and environmental context. In some tenders, non-hydrogen options deliberately specified by operators reduce complexity — align technical proposals to procurement preferences.

- Service and digitalization: Differentiate through predictive maintenance, digital monitoring and condition-based service contracts. These measures materially lower lifecycle costs and are increasingly demanded by large transmission owners.

- Local content and modularization: For public tenders and REZ programs, build local assembly or service footprints where feasible to accelerate approvals and capture value.

Risk considerations and red flags

- Operational safety and leakage: Hydrogen’s flammability and permeation characteristics require rigorous sealing and maintenance regimes. Underestimating these will increase downtime and liability exposure.

- Supply chain concentration: High concentration among top suppliers means single-source exposure for key components. Consider spares pools and parts standardization strategies.

- Regulatory divergence: Regional variation in tender specifications — from hydrogen-embracing jurisdictions to operators that explicitly prefer non-hydrogen solutions — demands agile proposal strategies rather than one-size-fits-all product offers.

How to use this intelligence in 2026

PW Consulting’s report is designed as a decision-ready tool: procurement teams can extract tender-ready language and risk matrices; OEM product leaders can identify feature gaps and aftermarket opportunities; financial sponsors can calibrate cashflow models to absorption curves reflected in the forecast; and grid operators can benchmark resilience metrics against alternative investments.

Next steps

This brief highlights the strategic contours that will shape capital allocation and product strategy in 2026. For granular breakdowns, regional and application-level demand tables, vendor scorecards and full scenario outputs — including downloadable models and procurement templates — consult the full report and supporting dataset on our report page. PW Consulting’s advisory team is available for tailored briefings, competitive-sourcing support and implementation workshops to translate the market intelligence into executable project plans.

Contact PW Consulting to arrange a briefing and obtain access to the full Hydrogen Cooling Synchronous Condenser Market Report and accompanying decision tools.

For detailed analysis of this topic, please visit the official page:Hydrogen Cooling Synchronous Condenser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com