Global PCIe Retimers Market Growing at 43.3% CAGR Through 2032

Other |

2026-07-02 12:17:15

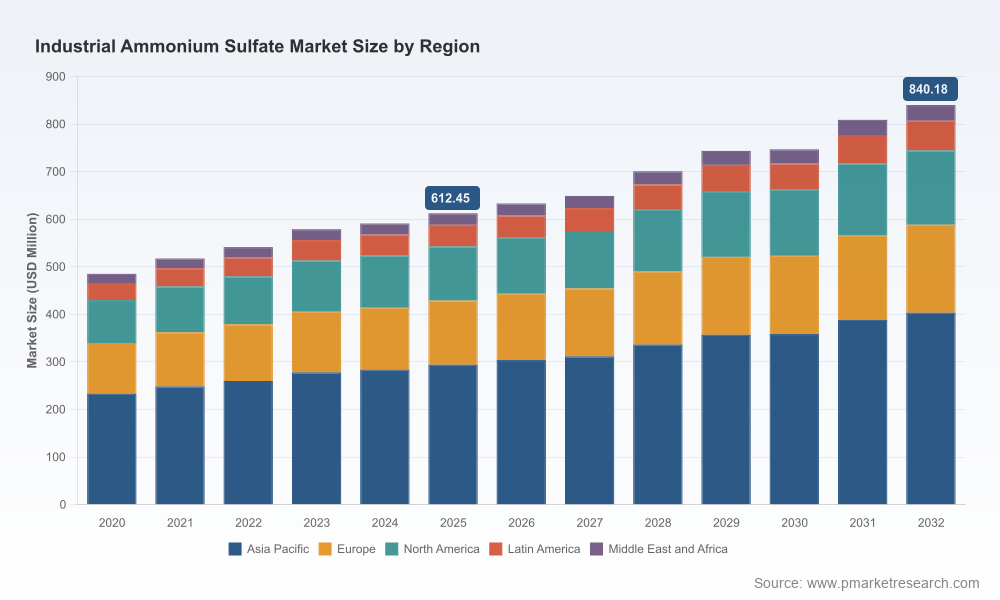

As companies prepare capital allocation and sourcing strategies for 2026, the industrial ammonium sulfate market has moved from a niche commodity into a strategically sensitive input for downstream industrial processes. PW Consulting’s newest study—anchored on a 2025 base year and extending forecasts through 2032—projects a clear upward trajectory: the market expanded from approximately USD 485 million in 2020 to about USD 612 million in 2025 and, under our central scenario, is expected to approach the mid-single-digit CAGR pathway embedded in our forecast window (2026–2032), with the market moving toward an estimated USD 840 million by 2032. This trajectory is underpinned by persistent trade flows, evolving feedstock dynamics and a regulatory environment that is reshaping cost curves and regional supply balances.

Industrial Ammonium Sulfate Market

Procurement impact: Industrial ammonium sulfate is an input for water treatment, industrial chemistry and other process-intensive sectors where small changes in feedstock availability or price can cascade into margin compression or project delays. Companies with exposure to these downstream uses must reassess purchasing strategies and contract tenors in 2026.

Industrial Ammonium Sulfate Market

Capital planning: Given the market’s steady expansion and pockets of regional trade concentration, capital investments in production capacity, tolling arrangements or toll-to-own supply agreements deserve fresh scenario analysis before board approvals.

Industrial Ammonium Sulfate Market

Regulatory and ESG risk: New emissions standards and environmental consolidation—particularly in key supply geographies—are creating discontinuities in feedstock availability and cost. Compliance-driven closures and permit tightening are actionable risks for sourcing and operations teams.

Our time series shows a resilient market with steady recovery since 2020 followed by a measured expansion into the mid- to late-2020s. The 2020–2025 history and the 2026–2032 forecast combine to illustrate several dynamics that should guide 2026 strategy: demand base resilience across cyclic and non-cyclic end uses; structurally driven trade flows where by-product sources continue to shape global supply; and an evolving mix toward specialty and industrial grades in some regional markets. The study quantifies this evolution and applies sensitivity analysis to test the market under alternative feedstock and policy scenarios—information critical to capital and procurement decisions next year.

Our report is intentionally built as a playbook for executives, commodity managers and M&A teams. Highlights include:

Comprehensive market sizing and a 2020–2032 forecast framework, including base-case, upside and downside scenarios calibrated to feedstock price variances, trade disruptions and key regulatory milestones.

Supply‑side analysis that maps primary production routes (ammonia + sulfuric acid reaction) and by‑product streams (notably caprolactam and coke‑oven derivatives), linking feedstock cost exposures to producer operating leverage.

Trade-flow diagnostics and importer/exporter risk heat maps, with port-level throughput trends and alternative logistics pathways for stress testing supply continuity.

Regulatory impact assessment, including implications of recent NESHAP updates and other jurisdictional emissions controls on operating costs, permitting timelines and capital expenditure needs.

Scenario-based pricing models and hedging templates that companies can adapt to their specific contract structures—ranging from spot-indexed purchases to long-term offtakes.

An investor toolkit: valuation sensitivities, greenfield vs brownfield investment decision matrices, and a prioritized list of potential acquisition targets based on strategic fit and integration upside.

Customizable dashboards and KPI sets for procurement, operations and commercial teams—enabling rapid translation from insight to action without sharing proprietary segment-level tables in this preview.

The market exhibits moderate concentration: our CR3 and CR5 metrics indicate that a small cluster of global chemical companies hold meaningful shares while a long tail of regional and specialty producers remains active. This structure supports both global-scale strategies and localized, service-oriented competition.

Leading industrial players—ranging from integrated chemical majors to regional specialty manufacturers—deploy distinct strategies that define opportunity sets for partners and challengers alike. Examples include:

BASF SE — leverages integrated chemical value chains and global logistics to serve industrial applications with scale and service continuity.

Evonik Industries AG — emphasizes specialty ammonium sulfate derived partly as a byproduct from caprolactam routes, positioning for higher‑margin industrial and pharmaceutical applications with sustainability branding.

LANXESS — integrates intermediates portfolios to target industrial end users across Europe and Asia, often coordinating product and application development with customers.

AdvanSix Inc. — a major North American platform with integrated ammonia and sulfuric acid capabilities, recently reporting price and mix strength that reflect tight supply-demand balances in select markets.

OCI Global, Sumitomo Chemical, Domo Chemicals, Nutrien Ltd., Jost Chemical and Hubbard‑Hall — a mix of fertilizer-scale producers, byproduct specialists and high‑purity suppliers that together shape regional supply options.

Each of these players is reacting to the same pressures—feedstock volatility, environmental regulation and shifting end-use demand—but they differ in their balance of integrated feedstock ownership, by‑product sourcing and customer-facing services. PW Consulting’s competitor playbooks in the report dissect these strategies and identify tactical moves (capacity reallocation, co‑processing agreements, geographic re‑balancing) that are likely to re-order competitiveness in 2026–2028.

Supply‑demand signals: Public filings and sector reporting in early 2026 indicate continued price strength and regionally tight volumes in select markets—insights that our report overlays with sensitivity testing for procurement teams.

Trade policy: The U.S. government’s 2026 tariff measures explicitly exempted ammonium sulfate from a new import tariff program designed to stabilize key agricultural and industrial inputs. This decision materially affects cost benchmarking and sourcing alternatives for North American buyers.

Flow concentration: Recent import volumes into major trading blocs demonstrate sustained global trade flows, emphasizing the importance of flexible logistics and diversified supplier portfolios.

Regulatory shift: The April 2026 updates to hazardous air pollutant standards introduce compliance costs and potential permit delays for certain chemical manufacturing configurations—an operational risk that should be baked into 2026 capital and outage planning.

Based on our analysis, PW Consulting recommends a prioritized set of actions that executives should consider in 2026. These are designed to be implementable within typical planning cycles and to reduce downside risk while capturing growth opportunities:

Stress‑test procurement contracts against three scenarios (soft demand, supply shock, regulatory-driven contraction). Convert insights into contract clauses that allow cost pass-throughs or volume flexibility.

Evaluate vertical integration or long-term tolling as part of a feedstock security strategy—particularly where ammonia and sulfuric acid exposures are material. Our investment calculator quantifies payback under multiple feedstock price paths.

Prioritize permitting and environmental compliance in any near-term brownfield expansion; reallocate CAPEX where regulatory timelines compress returns.

Assess M&A targets not only for capacity but for access to by‑product streams and specialty manufacturing routes that improve route-to-market economics.

Redesign supply‑chain network maps to include alternative ports, dual-sourcing nodes and inventory buffers calibrated to the market’s mid-single-digit growth and episodic trade volatility.

Adopt product differentiation strategies in customer-facing markets where purity and form factor command premium positioning, fueled by technical service and blended product solutions.

The report is built for execution. It includes scenario models that are refreshable with client-specific inputs, step‑by‑step procurement playbooks, an M&A screening matrix aligned to strategic objectives, and an operations checklist that aligns plant reliability measures to forecasted demand milestones. For procurement teams, we provide adaptable RFP templates and recommended contract language to capture price‑and‑volume protection. For investors, we include valuation sensitivity models keyed to feedstock and regulatory variables.

PW Consulting’s Industrial Ammonium Sulfate Market report delivers an evidence-based, operationally oriented roadmap for 2026. We have intentionally withheld granular regional and end‑use tables from this preview to preserve the consultancy-grade datasets that underpin our recommendations. Decision-makers reading this preview should recognize that the macro trends—steady market expansion from 2020 through 2025, an expected mid-single-digit compound growth path through 2032, concentrated yet contestable supply dynamics, and recent policy developments—create both risk and opportunity. The full report supplies the segment-level detail, scenario outputs and executable templates required to translate these high-level insights into boardroom-ready decisions.

For companies seeking immediate operational playbooks, bespoke scenario runs, or a tailored M&A screening aligned to your balance sheet and feedstock exposure, PW Consulting offers executive briefings and custom workshops. Visit our report landing page to access the full dataset, methodology appendix and to schedule a confidential briefing with our industrial chemicals practice.

For detailed analysis of this topic, please visit the official page:Industrial Ammonium Sulfate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com