Anti-Fingerprint Coatings Market: Strategic Imperatives for 2026 — PW Consulting Deep Industry Brief

As companies prepare strategic plans for 2026 and beyond, the Anti-Fingerprint (AFP) coatings sector has moved from niche performance chemistry to a mainstream element of product differentiation, regulatory compliance, and supply-chain risk management. Our new PW Consulting market intelligence report — anchored on a 2025 base year and a detailed 2026–2032 forecast horizon — projects continued expansion at a steady compound annual growth rate of 6.45%. The global market, assessed across materials, deposition technologies, and end‑use applications, is expected to progress materially from its 2025 base to a substantially larger market by 2032 (reported in USD, Million), underscoring why AFP coatings must appear in board-level discussions for product roadmaps, procurement strategies, and M&A screening this year.

Anti Fingerprint Coatings Market

Why 2026 Is a Strategic Inflection Point

- Regulatory acceleration: Regulatory initiatives such as the EU’s continued phase-out of legacy PFAS chemistries are forcing rapid reformulation and qualification of PFAS-free alternatives. This is not a future risk — it is an active market force shaping product portfolios today.

- Material and technology transition: Suppliers are shifting from fluorinated topcoats toward silicone-, silane-, and sol‑gel-based approaches and scalable PVD routes that can deliver comparable oleophobic/hydrophobic performance without PFAS concerns.

- OEM timing pressure: Consumer electronics, automotive displays and high-touch architectural finishes have compressed qualification windows. Device and automotive OEMs are increasingly demanding validated PFAS-free solutions that meet durability and optical clarity thresholds.

- Competitive moves: Leading suppliers are moving from R&D announcements to commercial launches and qualification programs; for example, a major Tier-1 coatings supplier released a PFAS/fluorine-free AFP portfolio in early 2026 targeted at automotive displays, signaling accelerated product availability.

For executives, these trends mean 2026 is the year to switch from exploratory pilots to executable plans: supplier selection, qualification timelines, and capex decisions must be synchronized to regulatory and product launch calendars.

Anti Fingerprint Coatings Market

What PW Consulting’s Report Delivers — Practical, Executable Intelligence

Our analysis is designed to be immediately actionable for corporate strategy, procurement, R&D leadership, and M&A teams. Highlights include:

Anti Fingerprint Coatings Market

- Forward-looking market sizing and top-line demand forecasts (2026–2032) with scenario splits based on regulatory trajectories and technology adoption curves.

- Segment-level demand drivers and adoption timing across consumer electronics, automotive displays, architectural finishes, medical devices, and other high-touch verticals (detailed regional and application-level data are available in the full report).

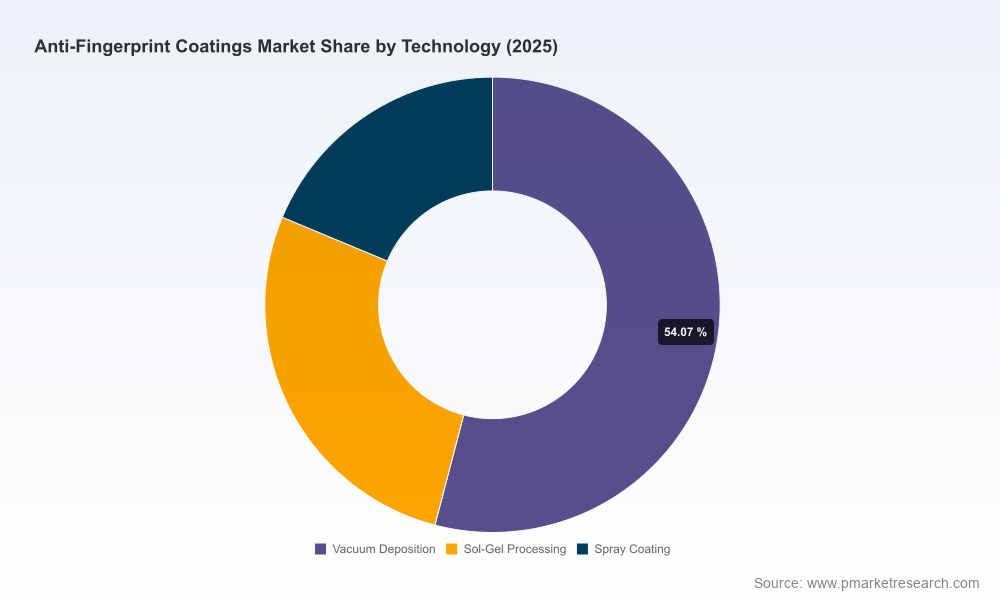

- Technology landscape mapping: deposition techniques, chemistries, process integration challenges, and throughput implications for vacuum, sol‑gel, spray and PVD-based approaches.

- Supplier benchmarking and competitive scorecards, including market concentration metrics to inform partnership or consolidation strategies.

- Commercial playbooks: procurement negotiation levers, qualification templates, total cost of ownership models, and pilot-to-scale roadmaps.

- Regulatory and sustainability risk matrix — actionable compliance pathways and reformulation timelines tied to real-world product launches and regulatory milestones.

- M&A and alliance candidate shortlist, with diligence checklists focused on IP defensibility, scale economics, and go-to-market compatibility.

Competitive Landscape: Who’s Competing, and How

The AFP coatings landscape is occupied by a mix of specialized innovators, legacy chemical giants, and coatings groups that have embedded AFP offerings into broader portfolios. Market concentration is meaningful but not insurmountable: the three-largest players account for roughly the high‑thirty percent range of global revenue (CR3 ≈ 38.45%), while the five-largest players capture just over half of the market (CR5 ≈ 52.12%). This structure favors both scale advantages for incumbents and opportunity windows for focused specialists with differentiated chemistries or application know-how.

Representative supplier archetypes covered in the report include:

- Specialist nano-solution providers: Companies that commercialize liquid-applied nano-coatings focused on easy retrofit and on-site application are attractive partners where low‑temperature or in-line spray application is needed.

- Performance-chemistry incumbents: Established chemical and coatings houses offer broad distribution, rigorous qualification processes, and deep formulation capabilities, often prioritizing enterprise customers.

- PVD and vacuum-focused vendors: Firms emphasizing physical vapor deposition routes target premium device and appliance segments that demand thin, durable inorganic layers with high optical clarity.

Selected company vignettes (indicative capabilities):

- Aculon — a specialist in liquid-applied nano AFP treatments optimized for rapid application across glass, metal and polymers; positions itself on ease-of-use and retrofit potential.

- Ionbond (IHI Group) — provides PFAS-free PVD-style AFP coatings targeted at appliances and consumer products with an emphasis on durability and smudge reduction.

- Momentive — a portfolio approach emphasizing sprayable, PFAS-free hydrophobic/oleophobic chemistries for glass and plastics, focused on stain resistance and broad substrate compatibility.

- Henkel — leveraging scale to commercialize silicone-based, fluorine-free AFP formulations aimed at automotive and display applications; recent product launches underscore incumbent responses to regulatory pressure.

- PPG, Daikin, AGC, Rimex Metals, Diamond Coatings — represent a mix of legacy fluoropolymer expertise and newer PFAS-free offerings, each with differentiated go-to-market routes and substrate specializations.

Technology and Supply-Side Dynamics: What Matters for Sourcing and R&D

Effective AFP strategies require an end-to-end view of chemistry, process integration, and lifecycle performance. Key technical takeaways:

- Chemistries in play include fluoropolymers, perfluoropolyethers (PFPE), silanes, silica-based systems, and silicone-derived formulations. The regulatory backdrop is shifting R&D budgets toward the latter groups.

- Manufacturing choices (vacuum deposition, sol‑gel processing, spray coating) produce trade-offs between unit cost, throughput, part geometry constraints, and environmental footprint; these trade-offs should drive supplier selection and capital planning.

- Durability metrics — abrasion resistance, adhesion, optical haze, and long-term oleophobic retention — will be the battleground for OEM acceptance, especially in automotive and premium consumer electronics segments.

- Raw-material sourcing carries exposure to fluorinated feedstock availability and pricing volatility; diversifying chemistries reduces regulatory and supply risk but may require additional qualification cycles.

Strategic Playbook for 2026: Five Immediate Actions

- Conduct a rapid materials audit: identify PFAS exposure across product lines and map qualification workstreams for PFAS-free alternatives with clear timelines.

- Prioritize supplier pilots that match application-specific durability targets; insist on third-party wear and optical testing as part of any POC contract.

- Align procurement and product development calendars — qualification lead times are real and must be synchronized with planned product launches.

- Pursue dual-sourcing where feasible to mitigate single-supplier disruptions and to increase negotiation leverage on price and IP rights.

- Embed regulatory foresight into product roadmaps: adopt compliance checkpoints to avoid late-stage redesigns and launch delays.

Why PW Consulting’s Report Is a Decision-Making Tool — Not Just Market Color

This publication goes beyond directional narrative. It provides the operational templates and analytic rigor required to translate market signals into boardroom decisions. The full report includes granular regional and application-level forecasts, supplier scorecards with capability matrices, negotiated pricing benchmarking, detailed capex and process integration models, and confidential M&A candidate dossiers — all of which are intentionally gated to preserve the commercial sensitivity of strategic data.

For executives evaluating entry strategies, supplier partnerships, or bolt-on acquisitions in 2026, the report delivers:

- Actionable supplier shortlists and qualification timelines tied to product-specific acceptance criteria.

- Scenario-modeled P&L impacts for switching chemistries or scaling internal coating capability.

- Road-tested procurement templates and pilot acceptance protocols designed to shorten time-to-market and reduce technical risk.

Next Steps

AFP coatings are no longer an optional aesthetic add-on; they are an operational necessity with regulatory, procurement and brand implications. PW Consulting’s Anti-Fingerprint Coatings Market report is calibrated to inform the full set of corporate stakeholders — R&D, procurement, product management, sustainability, and corporate development — as they make investment and sourcing decisions in 2026.

To access the full dataset, supplier scorecards, and scenario playbooks that underpin this executive brief, please visit our report page or contact PW Consulting directly for a tailored briefing and enterprise licensing options.

For detailed analysis of this topic, please visit the official page:Anti Fingerprint Coatings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com