It Spending On Clinical Analytics Market: Strategic Imperatives for 2026 — A PW Consulting Preview

Executive summary

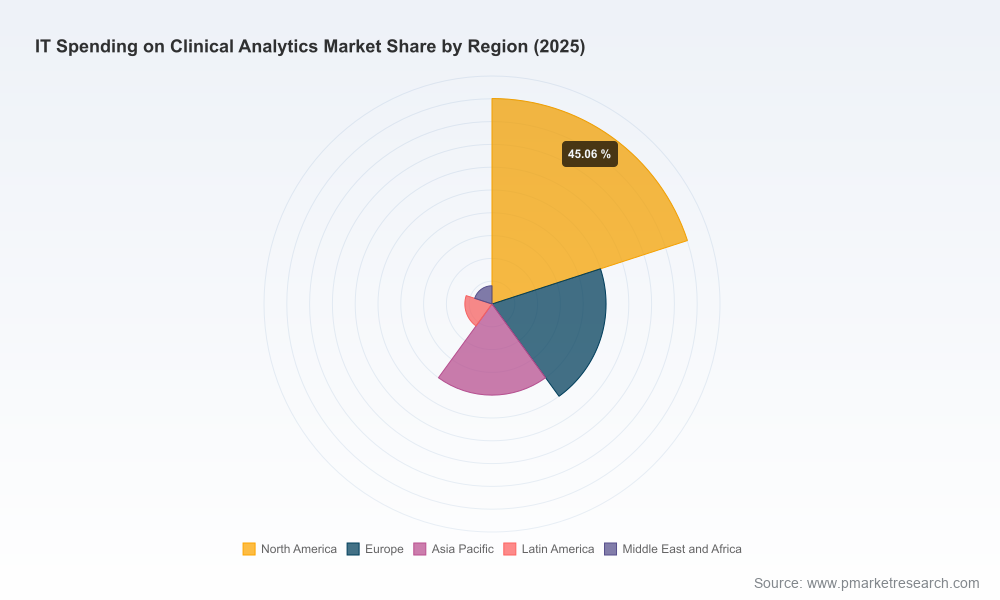

PW Consulting’s latest market intelligence — It Spending On Clinical Analytics Market (base year 2025, historical 2020–2025, forecast 2026–2032) — frames clinical analytics not as a narrow IT line item but as a strategic fulcrum for health systems, payers, life-science organizations, and vendors planning decisions in 2026. The global market reached an estimated USD 22.5 billion in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 13.45% through the forecast period, placing the 2032 opportunity in the tens of billions. These headline facts understate the practical decisions organizations must make now: where to prioritize people and data investments, how to structure vendor relationships, and how to mitigate an increasingly complex regulatory and infrastructure cost environment that can materially alter total cost of ownership.

It Spending On Clinical Analytics Market

Why this matters for 2026 decision cycles

- Budget cycles for 2026 are already in flight. Executives who treat clinical analytics as a discrete, tactical spend will be disadvantaged versus those who position it as an enterprise value engine tied to care quality, throughput, and alternative-payment-model performance.

- Macro spending momentum is strong: our market projection shows rapid upward trajectory from the 2025 base into 2026 and beyond — a signal that capital and operating budgets will increasingly pivot to analytics, AI-enabled decision support, and services that convert data into validated clinical impact.

- Concurrently, infrastructure and regulatory dynamics are creating non-linear risk to analytics programs. Energy and data-center policy, cross-border data transfer restrictions, and AI infrastructure investments are shaping the realistic TCO and time to value for analytics initiatives.

Market trajectory and concentration

Clinical analytics is scaling quickly as providers, payers, and life sciences buyers seek both predictive and operational insights. Our forecast baseline (2026–2032) reflects technology maturation, accelerated cloud adoption in clinical workflows, and growing monetization of real-world evidence. While headline growth is strong, market concentration remains moderate: the top three and top five vendors together capture a modest portion of the market, indicating a competitive landscape with opportunities for specialization, niche players, and consolidation through strategic M&A.

It Spending On Clinical Analytics Market

Dynamics shaping vendor and buyer strategies

- AI infrastructure and energy economics: Gartner estimated a substantial uplift in AI infrastructure investment for 2026; that scale of investment is driving demand for compute and data-center capacity, but it is also increasing exposure to energy policy and related cost allocation. Independent analysis highlights sizeable hidden economic and environmental costs tied to data centers and AI workloads — a factor buyers must internalize in procurement and sustainability planning.

- State and federal regulatory changes: Multiple U.S. states advanced legislation in 2025–2026 requiring data centers to internalize grid and generation costs; alongside this, U.S. DOJ rules effective April 2025 impose new constraints on cross-border bulk transfers of sensitive health data. These legal shifts change how vendors architect data flows and how enterprise buyers structure vendor contracts and compliance programs.

- Services and outcome orientation: As analytics tools proliferate, organizations are moving from tool purchases toward outcome-oriented engagements — e.g., risk-adjusted revenue protection, readmission reduction, and AI-validated decision support. Buyers increasingly demand hybrid commercial models that combine software licenses, managed services, and shared-savings arrangements.

Competitive landscape — high-level profiles and strategic differentiators

The market is populated by a mix of enterprise EHR incumbents, analytics pure-plays, life-sciences data specialists, and diagnostic OEMs. Each class of vendor brings distinct assets and constraints, which inform recommended partner strategies:

It Spending On Clinical Analytics Market

- Enterprise health IT platform vendors (examples represented in the landscape) compete on breadth — integrated EHR and analytics suites that promise seamless workflows and operational integration. Their strength is in deep provider relationships and embedded clinical workflows; buyers should assess upgrade cadence, extensibility, and openness for third-party models.

- Analytics and data-platform specialists emphasize advanced modeling, real-world evidence generation, and modular deployments. They tend to offer faster experimentation cycles and differentiated IP in predictive analytics and outcomes research, but often require stronger data-integration and governance investments from buyers.

- Diagnostic and device-aligned firms couple imaging, monitoring, and lab data with analytics, enabling diagnostic-driven insights and edge-compute use cases. These suppliers can be attractive where imaging or monitoring data is central to clinical pathways.

- Life-sciences analytics firms and CRO-aligned providers bring deep experience in real-world evidence and outcomes research, and are natural partners for pharmas and payer-provider collaborations focused on value-based arrangements.

PW Consulting’s report profiles the leading vendors across these archetypes and evaluates them against buyer-oriented criteria: data interoperability, clinical model validation, deployment speed, regulatory posture, and commercial construct. These profiles synthesize public disclosures, product roadmaps, and vendor-customer reference interviews to surface pragmatic fit considerations for 2026 procurements.

Recent market developments — context for near-term strategy

- Industry intelligence sources have highlighted a surge in C-suite prioritization of AI-based clinical solutions for 2026–2027, underscoring the imperative to align analytics investments with executive KPIs.

- Major platform vendors have expanded analytics toolsets and cloud capabilities to accelerate clinical insight generation in hospital and ambulatory settings.

- M&A activity and platform consolidation in late 2025 and early 2026 have focused on cloud imaging, data unification, and service-enabled analytics—an indicator that go-to-market value is shifting towards integrated data services that lower buyer friction.

What PW Consulting’s report delivers — practical, decision-ready assets

This release is a preview. The full report is structured to support immediate 2026 decision-making by delivering:

- Validated market sizing and a transparent forecasting methodology (historical 2020–2025, base year 2025, forecast 2026–2032) with scenario analyses that isolate technology, regulatory, and cost variables.

- A vendor evaluation framework and vendor scorecards designed for procurement teams, technology committees, and M&A diligence teams.

- Implementation playbooks and TCO models that quantify the hidden costs and timing implications of compute, energy, and compliance choices (including differential impacts of on-premise, hybrid, and cloud architectures).

- Case studies and deployment roadmaps spotlighting rapid-win clinical use cases — from decision-support pathways to population-health scaling — plus recommended KPIs to govern vendor relationships and internal programs.

- Risk matrices addressing energy policy, data-transfer constraints, and AI governance, with legal and regulatory checkpoints tailored to U.S., European, and cross-border operational models.

Strategic imperatives for 2026 — practical recommendations

- Prioritize outcome-linked procurement: Shift contracts toward measurable quality or cost outcomes and include clauses that share the burden of infrastructure volatility (e.g., energy-related surcharges or force majeure tied to grid constraints).

- Make data governance investment non-negotiable: Enact cross-functional control towers that unify clinical, legal, and security teams; revise data-transfer policies to comply with the latest national restrictions and to preserve collaborative analytics with global partners under constrained regimes.

- Model total cost of compute: Include the real economic impact of data-center and AI compute costs — both direct pricing and social/environmental externalities — when comparing on-premise versus cloud-first strategies.

- Adopt vendor composability: Favor architectures and commercial models that allow rapid substitution of analytics modules. Given moderate market concentration, specialization will persist; avoid vendor lock-in that impedes innovation adoption or second-source entry.

- Invest in clinical validation and change management: Technical accuracy is necessary but not sufficient. Scale requires validated clinical pathways, clinician-facing workflows, and measurable rollback plans where outcomes diverge from expectations.

How to use the full report

PW Consulting’s full market study is designed as a working tool for 2026 planning: finance leaders can extract budget scenarios and TCO calculators; CIOs and CMIOs can use vendor scorecards and deployment templates; corporate development teams can prioritize M&A targets and partnership sets. Importantly, the report’s granular segmentations, country-level dynamics, and vendor scorecard data are intentionally gated: they are provided in the full report to preserve analytical value and to support buyer confidentiality during procurement cycles.

Conclusion and next steps

The clinical-analytics landscape entering 2026 is defined by rapid growth, technical opportunity, and rising systemic risk. PW Consulting’s preview underscores that success will go to organizations that align investment with outcomes, internalize infrastructure and regulatory impacts, and select vendors through a lens of composability and validated clinical effect. For teams that need to convert this preview into an executable 2026 plan — with detailed segment breakouts, vendor benchmarking, and TCO models — the full It Spending On Clinical Analytics Market report is available through PW Consulting. Contact us to schedule a briefing and download the full dataset, supporting appendices, and procurement-ready tools.

For detailed analysis of this topic, please visit the official page:It Spending On Clinical Analytics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com