Electronic Clinical Outcome Assessment (eCOA) Market Performance Review and Future Industry Trends

Other |

2026-06-15 10:54:45

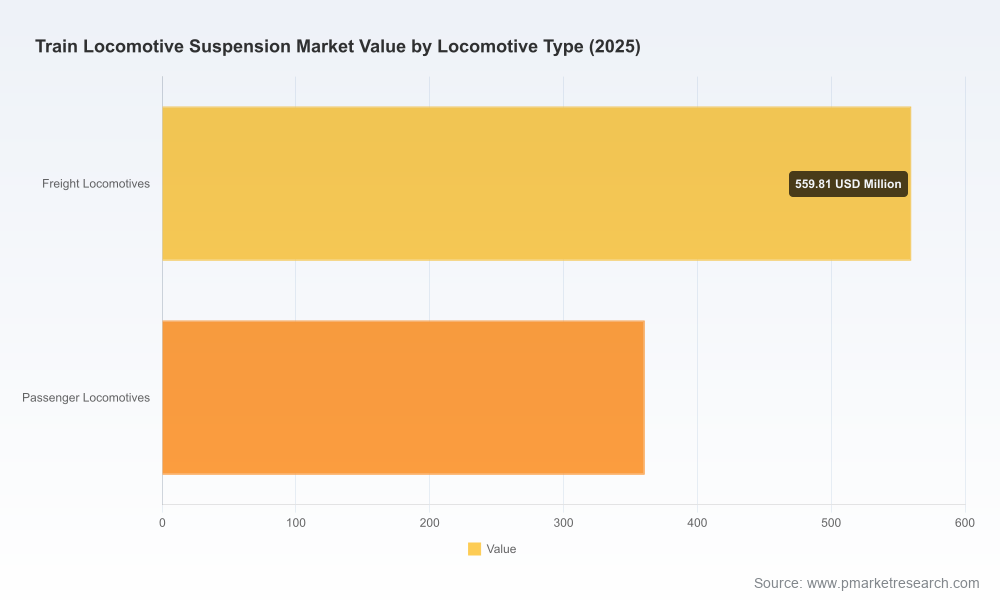

PW Consulting’s latest market study on the Train Locomotive Suspension Market provides a forward-looking, action-oriented blueprint for executives, procurement leaders, and engineering chiefs preparing strategic moves in 2026. Anchored on a robust historical review (2020–2025) and a detailed forecast period (2026–2032), the research quantifies the industry’s trajectory—with the market valued at USD 920.45 Million in the base year (2025) and projected to expand at a compound annual growth rate (CAGR) of 4.62% through 2032, reaching approximately USD 1.26 billion by 2032. This briefing summarizes the strategic implications we expect to matter most next year and provides a concise guide to the report sections that deliver executable intelligence.

Train Locomotive Suspension Market

Several convergent forces make 2026 a decision-rich year for companies involved in locomotive suspension systems. First, continued fleet modernization programs among major rail operators are driving demand for upgrades in bogie-level dynamics and secondary suspension technologies. Second, aftermarket and lifecycle service models are maturing into predictable revenue streams, creating margins and valuation uplifts for suppliers that can combine hardware, refurbishment and long-term service contracts. Third, regulatory pressure—particularly inspection and safety standards—continues to tighten, requiring manufacturers and operators to invest in certification and test regimes. In aggregate, these dynamics create a window for strategic investment, consolidation, and product differentiation.

Train Locomotive Suspension Market

Measured growth with predictable upside: The market’s mid-single-digit CAGR (4.62%) signals a steady expansion—sufficient to support targeted capital allocation but not large enough to assure broad-based margin expansion without operational leverage or differentiated offerings.

Train Locomotive Suspension Market

Moderate concentration: The market displays a moderate degree of vendor concentration; the top-tier suppliers collectively control a meaningful share of supply (top-five suppliers account for roughly 48% of market revenue). That split creates both partnership opportunities for scale players and entry points for specialists focused on niche components or retrofit services.

Aftermarket and lifecycle services as value drivers: Recent large-scale fleet modernization and new-contract awards underscore that suspension-related upgrades are frequently embedded in wider locomotive refresh programs. Suppliers that can guarantee refurbishment quality, traceable testing and long-term performance warranties stand to capture outsized aftermarket revenues.

Material and certification risk: Production depends on high-grade steels, advanced elastomers, and hydraulic fluids. Price volatility and supply disruptions can compress margins and lengthen lead times; compliance with ISO/EN norms and national inspection standards (e.g., U.S. FRA requirements) is non-negotiable for entry into regulated tenders.

The report is designed as a decision-support toolkit for commercial and technical teams. Highlights include:

A validated market sizing and growth model (2020–2025 historic review and 2026–2032 forecast) that supports scenario planning under different capex and procurement cycles.

Segment-level mapping by component families, locomotive types and geographic markets, with supplier share matrices and channel economics to inform go-to-market strategies (note: detailed segment share tables are available in the full report).

End-to-end supply chain risk assessment highlighting raw material exposure, critical single-source components, and mitigation options including dual-sourcing, stock strategies and regional hedging tactics.

Regulatory and certification playbook that aligns product development roadmaps to compliance timelines and testing protocols—reducing bid risk for major procurement cycles.

Competitive landscaping with capability heatmaps, R&D intensity scoring, aftermarket readiness assessments, and M&A/partnership opportunity matrices focused on acceleration paths for 2026.

Practical commercial templates: tender-response strategies, lifecycle service contracting models, and retrofit pricing frameworks tailored to both rolling-stock integrators and OEM suppliers.

The market is characterized by an interplay between diversified industrial suppliers, specialized suspension OEMs, and regional spring manufacturers. Our benchmarking highlights the strategic postures of leading players:

Continental AG (ContiTech) — Plays to its systems capability: combines primary and secondary spring solutions with refurbishment services that appeal to operators seeking OEM-quality life extension. Strength: integrated solutions and global service footprints.

Enidine (ITT Enidine) — Differentiates through engineered motion-control products (friction snubbers, rotary hydraulic units). Strength: application-specific damper engineering and durability in high-stress vertical/lateral control roles.

Amsted Rail — Focuses on heavy-haul springs and bogie assemblies, leveraging deep engagement with freight markets. Strength: scale in freight applications and heavy-duty coil spring systems.

KONI (ITT KONI) — Recognized leader in dampers with product lines designed for longevity and customization. Strength: proven product lifecycles and tailored performance engineering for vertical/horizontal bogie control.

Hutchinson (TotalEnergies group) — Offers broad product coverage across both primary and secondary suspension with long-established rail credentials. Strength: historical track record and global manufacturing footprint.

Lesjöfors, Dendoff Springs and other specialists — Provide custom spring solutions and niche manufacturing capacity, typically serving retrofit and regional supply needs. Strength: manufacturing flexibility and responsiveness.

Sumitomo Electric & Delkor Rail — Represent strategic regional and technology-specific offers (e.g., air springs, composite rubber-metal systems), often used in passenger comfort and vibration mitigation roles. Strength: materials expertise and local OEM partnerships.

For buyers, understanding which supplier brings systems integration versus component specialization is critical. Suppliers built around lifecycle services or refurbishment are best positioned for long-term aftermarket value; those focused on engineered dampers or springs can command higher margins in performance-sensitive retrofit programs.

Large fleet agreements and modernization deals are reshaping procurement patterns: major locomotive contracts and retrofit packages announced in the past 12–18 months are increasing the share of suspension upgrades embedded in bundled service contracts.

R&D pauses in some alternative-fuel train programs can temporarily reduce demand for associated suspension optimizations; however, electrification and hybridization remain structural trends that will reshuffle component specifications over the medium term.

Regulatory updates—especially inspection and safety standards—are tightening acceptance criteria, elevating the value of certified refurbishment and validated components in competitive bids.

Prioritize aftermarket and service models: convert one-time hardware sales into multi-year service revenues through refurbishment guarantees, predictive maintenance offerings, and performance-based contracts.

Invest selectively in certification readiness: aligning product validation timelines to major operator procurement calendars reduces bid rejection risk and shortens time-to-revenue.

Hedge raw material exposure: build sourcing flexibility for high-grade steels and elastomers, and quantify the P&L impact of material shocks in pricing models.

Target partnerships for capability gaps: suppliers looking to enter new locomotive segments should favour joint engineering or acquisition of niche damper or air-spring specialists rather than greenfield R&D when speed-to-market matters.

Focus R&D on modularity and retrofit friendliness: simpler integration into existing bogies and clear upgrade paths for operators increases tender competitiveness.

Our full Train Locomotive Suspension Market report contains the granular data and decision tools executives need to act in 2026: downloadable financial models, supplier scorecards, tender risk matrices, and regional go-to-market playbooks. The report purposefully balances public strategic takeaways with proprietary tables and scenario models reserved for subscribers and licensees. If your team is assessing market entry, M&A targets, or a service-led transformation of your suspension business, PW Consulting’s deliverables will reduce execution risk and compress time-to-value.

For access to the complete dataset, downloadable models, and a tailored briefing, visit our report page. The full intelligence package is designed to be directly executable by strategy, commercial, and engineering teams preparing 2026 plans.

For detailed analysis of this topic, please visit the official page:Train Locomotive Suspension Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com