On-Page SEO Optimization Service Strategies That Improve User Experience

Other |

2026-06-12 06:34:18

PW Consulting today publishes a strategic preview of our comprehensive Coal-to-Liquids (CTL) Market Research Report, calibrated to guide corporate leaders, investors, and public-sector planners making critical decisions in 2026. Built on a rigorous base year of 2025 and a forecast horizon running through 2032, the study maps the CTL landscape across technology routes, commercial-scale activity, regulatory inflection points, and financing pathways. At the macro level, the CTL market exhibited steady expansion from USD 6,050.2 Million in 2020 to USD 7,250.4 Million in 2025, and our scenario-led forecast tracks a compound annual growth rate (CAGR) of approximately 3.92% over the 2026–2032 period, with modeled market size trajectories extending into the low-to-mid USD 9,000 Millions by the end of the forecast window. This preview synthesizes the report’s practical value while preserving detailed subsegment tables and proprietary Excel models for report subscribers.

Coal To Liquid Ctl Market

2026 is shaping up to be a consequential year for CTL stakeholders. The industry is no longer a niche set of pilot projects — commercial-scale capacity expansions, strategic shifts toward hybrid decarbonization pathways, and the rising presence of integrated coal-to-chemicals schemes are reshaping investment calculus. For executives weighing capex approvals, forftake agreements, technology licensing, or decarbonization roadmaps, the report provides actionable frameworks to:

Coal To Liquid Ctl Market

Our analysis identifies three structural drivers sustaining CTL activity into the late 2020s: energy security imperatives in resource-rich markets, industrial demand for high-density liquid fuels and chemical feedstocks, and technology advances enabling scale efficiencies in both indirect and direct liquefaction routes. These drivers are counterbalanced by rising environmental scrutiny, evolving carbon policy frameworks, and the capital intensity of modern CTL installations when paired with decarbonization technologies such as CCS and green hydrogen.

Coal To Liquid Ctl Market

Important empirical markers reinforce the strategic stakes: by recent industry estimates, national CTL capacity in top deploying markets exceeded 12 Mt/a as of 2023, and historical feedstock utilization shows that in one illustrative year, approximately 40 Mt of coal were consumed to produce roughly 11 Mt of liquid products via CTL processes. Such scale underscores both the economic opportunity and the environmental exposure for project sponsors and incumbent operators.

Policy levers are emerging as the decisive variable. Our scenario work indicates that carbon price signals materially alter CTL project economics: a carbon-price floor calibrated appropriately improves investment probability for CTL projects coupled with CCS, while downstream carbon prices in the low tens of USD per ton range materially enhance the cost-effectiveness of CCS deployment. In practice, policy design — from carbon floors to targeted incentives for low-carbon hydrogen — will determine which commercial models are viable in 2026 and beyond.

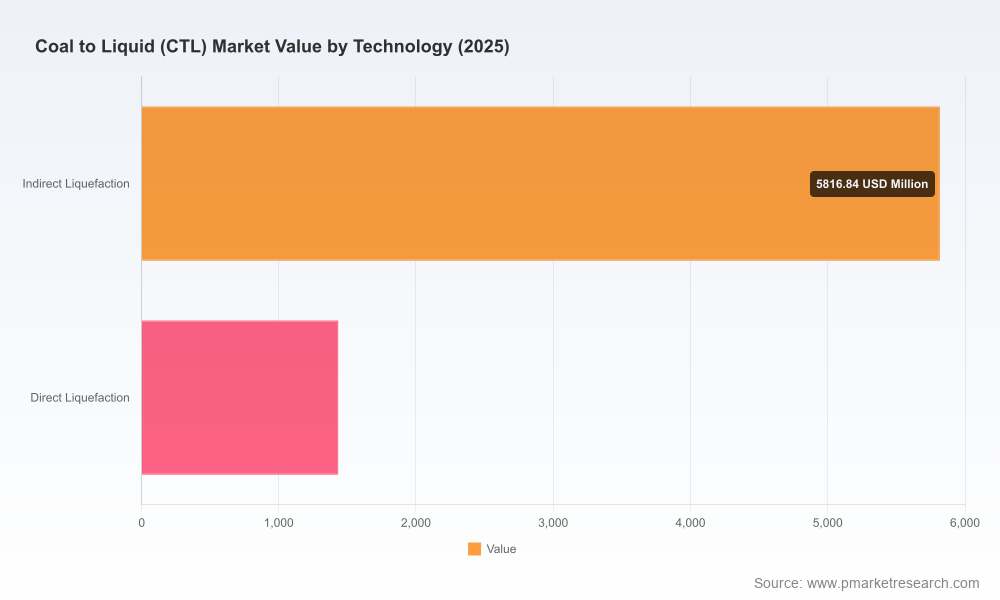

Differences between indirect and direct liquefaction pathways remain central to strategic decision-making. Indirect routes are typically advantaged at larger scales when integrated with gasification and Fischer–Tropsch synthesis, while direct routes can offer modularity and different feedstock flexibilities. The commercial landscape is also being reshaped by hybrid configurations: CTL platforms integrating green hydrogen for synthesis or deploying CCS on both syngas and flue streams are moving from demonstration toward early commercial operation.

Notable operational milestones captured in our monitoring include the start of commercial operations for the industry’s first coal-to-chemicals scheme that integrates green hydrogen, and large greenfield CTL investments commencing construction with multi-billion-dollar first-phase allocations. These projects serve as practical blueprints for engineering, procurement, and financing plans — but they also carry execution complexity that demands meticulous contractor selection, long-lead equipment planning, and hedging strategies for feedstock and carbon liabilities.

The CTL arena is concentrated, and a small set of integrated energy groups and technology providers account for the lion’s share of output and project momentum. Our competitive review highlights the strategic posture of incumbents while distilling implications for potential entrants and partners.

Market concentration metrics further clarify strategic realities: the top three operators capture roughly two-thirds of the market, and the top five command over four-fifths of production — a profile that favors JV structures, targeted M&A, and selective supplier partnerships as the primary routes for new commercial entrants to access scale.

This PW Consulting report goes beyond high-level forecasting to deliver practical, decision-ready content for 2026. Key deliverables include:

Importantly, the report contains granular segmentation tables and interactive Excel models that delineate regional capacity deployment, technology mix, and product breakdowns. In keeping with our “trailer” approach, we surface strategic highlights here while reserving full proprietary segmentation and company-level data for report purchasers and client engagements.

For boards and senior management preparing 2026 agendas, PW Consulting recommends a three-track approach:

PW Consulting’s Coal-to-Liquids (CTL) Market Report provides the detailed data, project-level models, and contractual templates needed to operationalize the insights summarized in this preview. Corporate leaders, project developers, technology licensors, and lenders seeking the full dataset and workbook-driven scenario models should consult the report landing page for subscription options and advisory engagements. Our clients receive tailored briefings that map the report’s findings to company-specific strategy and capital planning processes.

As CTL markets enter a phase where commercial scale, decarbonization commitments, and public policy intersect, the right intelligence in 2026 will determine who captures value and who bears systemic risk. PW Consulting’s new report equips decision-makers with the practical tools to navigate that junction — providing the strategic clarity needed to convert horizon-level opportunity into executable plans.

For detailed analysis of this topic, please visit the official page:Coal To Liquid Ctl Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com