Track Etched Membrane Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-04 11:50:53

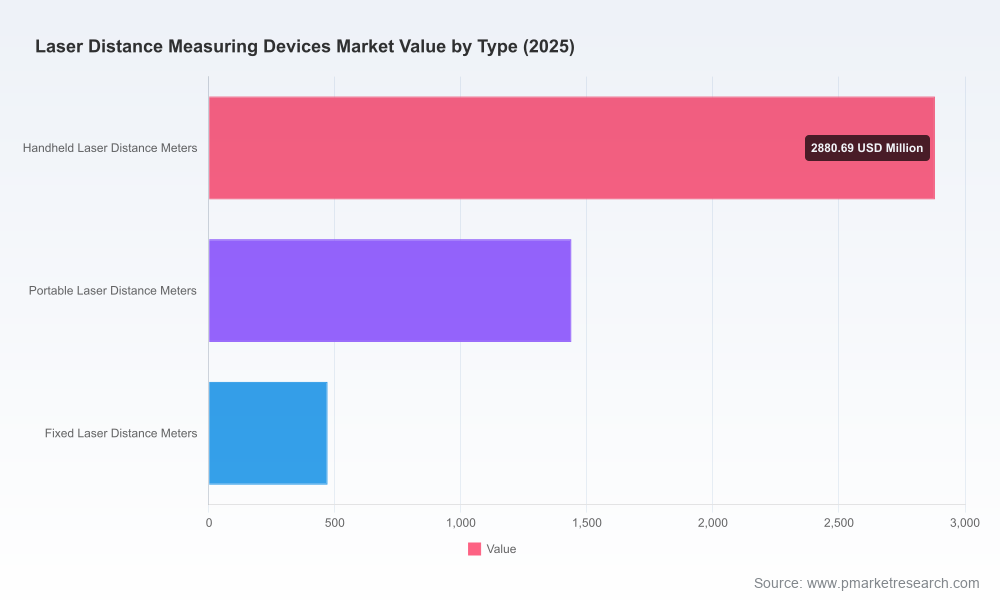

PW Consulting’s latest market intelligence on Laser Distance Measuring Devices (LDMs) provides a pragmatic roadmap for executives preparing for 2026. Built on a comprehensive base-year assessment (2025) and a seven-year forecast (2026–2032), the study combines a historical time series (2020–2025), market modelling and executable strategy workstreams to bridge insight and action. The global market reached approximately USD 4.79 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.15% through the forecast period, reaching roughly USD 7.28 billion by 2032. This release is designed to inform portfolio prioritization, commercial planning, regulatory readiness and M&A screening — while reserving the granular segment tables for the full report.

Laser Distance Measuring Devices Market

The recent five-year period shows durable recovery and technological adoption across both professional and industrial pockets of demand. From 2020 through 2025 the market expanded materially as construction activity normalized, industrial automation adoption accelerated, and measurement devices rapidly integrated digital connectivity. With a mid-single-digit CAGR of 6.15% forecast for 2026–2032, the industry trajectory reflects a mix of replacement demand, new-build measurement use cases (including BIM and site digitization), and product premiumization (connectivity, green lasers, ruggedization).

Laser Distance Measuring Devices Market

Two structural realities shape near-term strategy: first, the market exhibits moderate concentration — the top three vendors account for under half the market while the top five capture a clear majority — creating room for both scale players and specialized challengers. Second, unit economics are being altered by software and services: vendors that convert devices into recurring revenue nodes (data capture, cloud services, construction workflows) materially change valuation profiles and competitive dynamics.

Laser Distance Measuring Devices Market

Regulatory noise is no longer an incidental risk. An update to the IEC 60825-1 laser safety standard in early 2025 tightened labeling and documentation requirements for Class 2 devices sold in Europe. The practical implications are immediate: packaging, instructional materials, and compliance testing become part of product launch timelines and cost models. Companies that treat regulatory updates as a mechanical cost will be outpaced by those that incorporate them into product design and channel planning (e.g., pre-approved SKUs for key markets).

Recommended near-term actions for compliance and product teams:

Several technology vectors are changing product roadmaps and buyer preferences:

These trends favor vendors who can combine hardware excellence with software and channel partnerships. Notable vendor plays exemplify this shift: companies offering professional-grade GLM series devices with app ecosystems; established geospatial instrument providers with construction-centric offerings; and industrial-test firms producing rugged units for harsh environments. Collectively, these vendors illustrate how product feature sets are now tightly coupled with distribution and service models.

The competitive set is diverse, with different players occupying clear strategic roles. Our qualitative assessment highlights the following profiles (full vendor scorecards are available in the report):

These firms illustrate the spectrum from scale incumbents to specialized professional suppliers. Competitive opportunities for challengers include software-enabled differentiation, deeper channel partnerships, and niche positions (e.g., industrial sensors, high-accuracy surveying, or low-cost consumer tiers). Recent product news — such as Bosch's June 2025 launch of a green-laser model with extended range — underlines supplier emphasis on range and visibility as near-term differentiators.

Given the market’s moderate concentration, M&A is an attractive lever for players seeking scale or portfolio breadth. Acquisition targets that move the needle typically fall into three buckets:

Our report contains a practical M&A due-diligence checklist covering product validation, regulatory liabilities, customer concentration, channel overlap and integration cost modelling. We also provide valuation sensitivity tables that reflect different integration scenarios — useful when assessing how software-enabled assets should be priced relative to pure-hardware plays.

For companies making decisions in 2026, we recommend a prioritized operational agenda:

This release is the executive briefing. The full PW Consulting report provides the operational tools necessary to act in 2026, including:

To preserve the strategic value of the dataset and encourage direct engagement, this press release intentionally omits the detailed segmentation tables and region/application percentages — those are included in the full report and the associated data package.

Executives should treat the study as both a planning input and an operational checklist. Begin by aligning product roadmaps and channel plans to the macro demand scenarios presented; then prioritize compliance and software-as-a-differentiator initiatives. For corporate development teams, the vendor concentration metrics and M&A checklist in the report will accelerate target screening and valuation alignment.

PW Consulting is available to run tailored workshops that translate the report’s scenarios into a 12–18 month operating plan, including KPI design and a prioritized investment roadmap. For access to the full dataset, vendor scorecards and bespoke advisory engagements, please visit our report page or contact your PW Consulting representative.

Prepared by: PW Consulting — Senior Strategy & Industry Analysis Team

For detailed analysis of this topic, please visit the official page:Laser Distance Measuring Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com