Reliable Online Assignment Assistance to Boost Your Grades

Other |

2026-05-29 09:56:10

As health systems, device OEMs, and laboratory networks enter a new phase of capital allocation and regulatory scrutiny, calibration services for medical devices have shifted from a compliance line item to a strategic capability. PW Consulting’s latest market research on the Medical Device Calibration Service Market synthesizes macro growth, competitive dynamics, regulatory inflection points, and practical go‑to‑market options that senior leaders will need to act on in 2026.

Medical Device Calibration Service Market

Robust, sustained expansion: Global market value has more than doubled over the past half‑decade, expanding from the low‑billions in 2020 to an estimated USD 2.16 billion in 2025. Our base‑year calibration and a 2026–2032 forecast horizon show continued upside, with the market expected to approach USD 4.01 billion by 2032 under a projected compound annual growth rate of approximately 9.25%.

Medical Device Calibration Service Market

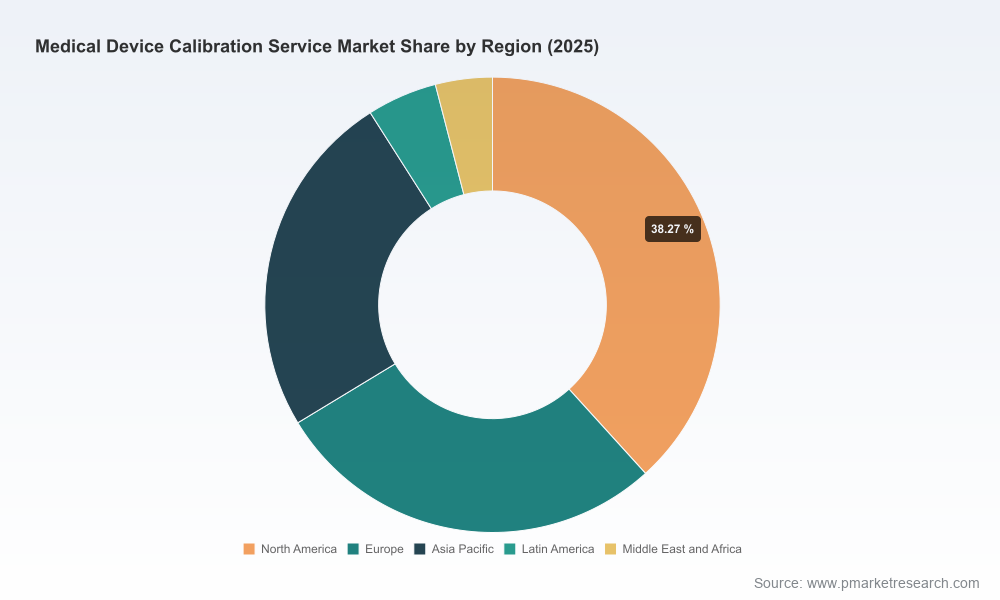

Fragmented provider landscape: The market remains decentralized — leading providers together control well under one third of the total market — creating distinct opportunities for consolidation, geographic roll‑outs, and service differentiation.

Medical Device Calibration Service Market

Service model diversity: Third‑party providers, OEM service arms, and in‑house biomedical engineering teams coexist and compete on speed, traceability, accreditation, and cost. The balance among these models is shifting as regulatory expectations and outsourcing economics evolve.

PW Consulting’s Market Research Report is designed as an operational playbook for strategy, procurement, and compliance leaders. It goes beyond narrative to provide:

Actionable market sizing and high‑level outlooks that align with fiscal planning cycles for 2026–2032.

A provider benchmarking framework that rates suppliers on accreditation, on‑site capability, multi‑brand competence, responsiveness, and service economics (note: detailed segment-by‑segment revenue breakdowns are reserved for the full report).

Regulatory overlay and decision trees mapping ISO/IEC 17025, ISO 13485, FDA Quality System requirements (including equipment control clauses) and the FDA’s ASCA pathway — clarifying where accredited calibration data materially changes submission and purchasing risk profiles.

Six practical playbooks for stakeholders: outsourcing vs. insourcing, hybrid staffing models, regional capacity buildouts, M&A screening, accreditation investments, and digitalization (asset management + calibration scheduling + evidence automation).

Implementation tools: supplier scorecards, SLA templates, sample capex/opex models, and a phased roadmap to achieve operational and regulatory readiness within 6–18 months.

The competitive map blends global calibration specialists, instrument manufacturers, and regionally focused service providers. Key names commanding attention in boardroom conversations include:

Trescal (France) — A global calibration specialist offering ISO 17025‑traceable services and broad on‑site/lab capabilities aimed at supporting ISO 13485 and other healthcare quality regimes. Trescal’s model exemplifies a full‑service third‑party play focused on compliance and scale.

Transcat, Inc. (United States) — An established calibration and laboratory services provider that has accelerated regional coverage through targeted acquisitions, enhancing its footprint for healthcare and life‑sciences clients.

Tektronix (United States) — Leveraging instrumentation heritage to deliver multi‑brand calibration services with an emphasis on traceability and test accuracy for biomedical and pharmaceutical instruments.

Fluke Biomedical (United States) — A hybrid OEM/service player that pairs proprietary test equipment with repair and calibration services — an attractive option for clinical operators prioritizing rapid turnaround and brand integration.

Specialized regional and niche providers — including accredited labs and service firms focused on imaging, ultrasonic diagnostic equipment, and hospital fleet maintenance — which collectively form the backbone of local service capacity.

For buyers and investors, the implication is clear: scale matters for national programs and large hospital systems, while localized expertise and accreditation are decisive in regulated pre‑market and clinical environments. The full report provides the competitive scoring matrix and recommended partner shortlists tailored by enterprise archetype.

Standards and accreditation: ISO/IEC 17025 accreditation continues to be the de facto quality signal for calibration providers. While accreditation may not be legally mandated in every jurisdiction, it materially affects the defensibility of test data in regulated submissions and clinical audits.

FDA pathways: The ASCA program and traditional QSR requirements (including routines for calibration, inspection, and maintenance) are pushing manufacturers and CROs to prefer labs that can deliver traceable, auditable data packages aligned with FDA expectations.

National capabilities matter: Recent investments in national and mobile calibration facilities in emerging markets demonstrate how infrastructure upgrades can change cost curves and access. These developments recalibrate where global players choose to invest and which customers elect to outsource versus build in‑house capability.

Selective examples that inform our 2026 scenarios:

Acquisition activity continues to be a primary vehicle for scaling regional coverage and technical breadth — exemplified by multi‑lab buyouts that integrate capacity into national service networks.

Public‑sector and academic institutions are deploying mobile calibration units and high‑level national facilities, expanding access to accredited services and compressing lead times in underserved regions.

Technology adoption — from asset telemetry to calibration workflow automation — is gaining traction among providers seeking to reduce downtime and deliver auditable evidence packages that satisfy both clinical operations and regulatory reviewers.

Our analysis translates market signals into nine prioritized moves for corporate leaders:

Reassess insourcing economics: Run a two‑year TCO and risk model comparing in‑house competence development vs. third‑party outsourcing, factoring in accreditation costs, staff training, and regulatory timelines.

Prioritize accredited partners for submission‑critical equipment: For devices tied to regulatory filings, only providers offering traceable data and clear audit trails should be considered.

Targeted M&A: For service firms and financial sponsors, pursue bolt‑on labs that deliver immediate accreditation credentials or geographic access rather than broad horizontal roll‑ups.

Invest in digital evidence chains: Hospitals and OEMs should accelerate deployment of asset management and calibration scheduling tools that reduce manual recordkeeping and speed regulatory responses.

Design hybrid delivery models: Combine OEM field service for brand‑critical devices with third‑party providers for commoditized maintenance to balance cost and uptime.

Build a regulatory playbook: Integrate ISO/IEC 17025 and ASCA criteria into procurement and audit checklists, and map the escalation path for non‑conforming calibration events.

Regional footprint strategy: Rebalance supplier portfolios where national infrastructure improvements exist — leveraging local accredited labs to reduce lead times and import costs.

Operational rigor: Standardize SLAs that include turnaround time, traceability documentation, uncertainty reporting, and corrective action timelines.

Scenario planning: Model demand shocks (device recalls or surge events) to stress‑test provider capacity and contingency routing across suppliers.

Senior executives can leverage our study in three specific ways: (1) incorporate the market projections and service cost models into capital and headcount plans for 2026–2027; (2) use the supplier evaluation framework to qualify vendors ahead of regulatory submissions or major equipment rollouts; and (3) adopt the playbook steps when considering acquisitions or launches of calibration services as a commercial offering.

True to the "trailer" principle, this release highlights the report’s strategic value and operational content while withholding granular segmental allocations, regional share tables, and a complete provider scorecard. Those detailed tables, transaction models, and supplier shortlists are included in the full PW Consulting report and are necessary for transaction execution and detailed procurement decisions.

PW Consulting is offering a limited number of executive briefings and tailored workshops through Q2 2026 to help institutional clients convert insights into 90‑day action plans. To request a briefing or to obtain the full report (which includes the detailed segmentation, annotated supplier matrix, and downloadable implementation templates), contact PW Consulting’s market research team or visit our website.

PW Consulting provides strategy and transaction advisory services to life sciences, medical device, and healthcare infrastructure clients. Our Medical Device Calibration Service Market report combines quantitative forecasting, provider benchmarking, regulatory mapping, and practitioner playbooks designed for executives making decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Medical Device Calibration Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com