Kitchen Food Garbage Processors Market — 2026 Strategic Preview from PW Consulting

Executive summary

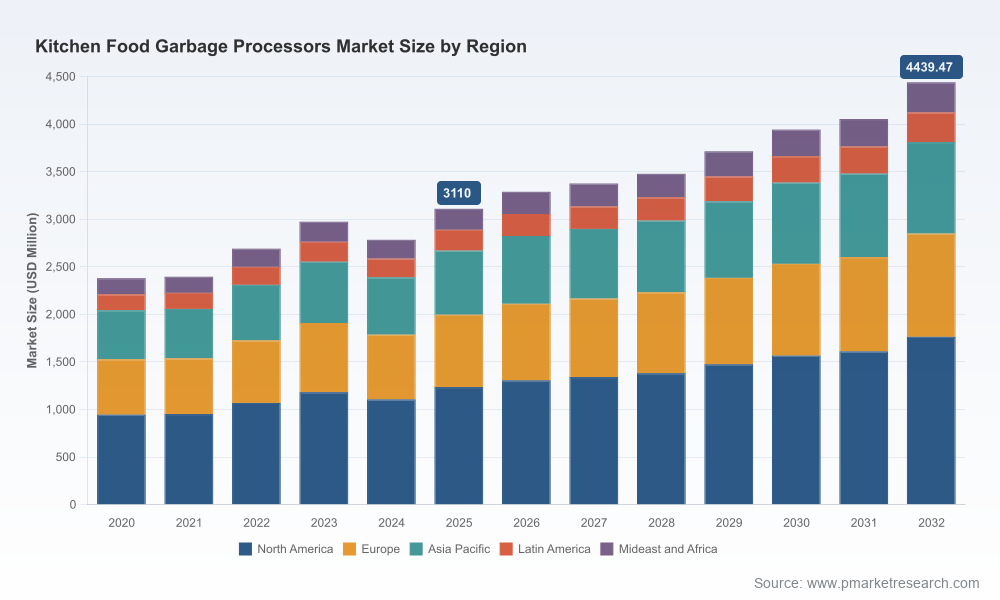

PW Consulting’s latest market study on Kitchen Food Garbage Processors (base year 2025) frames a clear, actionable picture for corporate leaders preparing decisions in 2026. The market has moved from the low‑billions in 2020 to roughly USD 3,110 Million in 2025 and is modeled to expand at a steady compound annual growth rate of 5.21% through the 2026–2032 forecast horizon, reaching mid‑single‑digit billions by 2032. This trajectory reflects both a recovery from supply‑chain and raw‑material shocks and the structural demand drivers tied to urbanization, kitchen modernization, and tightening organic‑waste regulations.

Kitchen Food Garbage Processors Market

Why 2026 matters: inflection points and policy noise

For executives, 2026 is not “more of the same.” Several converging forces will determine winners and losers over the next 3–5 years:

Kitchen Food Garbage Processors Market

- Trade and tariffs: Recent tariff actions have materially increased the landed cost of steel, aluminum and other components commonly used in disposers. Organizations that rely on thin manufacturing margins will feel pricing pressure unless they proactively redesign sourcing or pass through costs in a differentiated product strategy.

- Regulatory tightening: Local and state mandates that divert commercial food waste into alternative streams are accelerating demand for higher‑capacity commercial solutions and for integrated systems in multi‑unit residential developments. These regulations create predictable demand corridors but also raise compliance and certification burdens for suppliers.

- Product & channel innovation: New entrants and product launches showcased at trade events in early 2026 spotlight two vectors — performance that handles a broader range of waste types, and a focus on design/quiet operation aligned with premium kitchen brands. This is prompting incumbent OEMs to consider both defensive product upgrades and selective partnerships.

- Raw‑material volatility: Elevated steel and aluminum prices are not transitory for many manufacturers; firms that lock in forward positions, reengineer material usage, or pursue alternative alloys will enjoy margin resilience.

What the PW Consulting report delivers — practical, transactionable intelligence

We designed the study as a strategic playbook for executives, not just an academic exercise. The report combines rigorous quantitative forecasts with executable guidance:

Kitchen Food Garbage Processors Market

- Top‑line market sizing and trend analysis (2020–2025 historical; 2026–2032 forecast) with scenario variants for tariff and raw‑material outcomes.

- Demand drivers by channel, user cohort and product family — translated into addressable market and prioritized go‑to‑market targets (note: full segment tables and regional splits are available in the full report).

- Supply‑chain stress‑tests and a supplier‑risk heatmap that model input price shocks, logistics constraints and single‑source dependencies.

- Competitive benchmarking and a technology map covering motor technologies, grinding systems, sound suppression and integration with kitchen fixtures.

- Commercial playbooks — pricing elasticity models, channel‑partner incentive structures, retrofit and subscription offerings, and a short list of M&A/partnership targets screened for strategic fit.

- Implementation templates: product roadmap sequencing, pilot KPIs, regulatory compliance checklists, and sample ROI templates for enterprise buyers and installers.

Competitive landscape: how leading suppliers are positioned

The market is characterized by a mix of established OEMs with deep brand recognition and smaller, agile innovators introducing differentiated value propositions. Key profiles and strategic observations include:

- InSinkErator (Mount Pleasant, WI): As a market icon with a broad residential and commercial footprint, their strengths are brand equity, channel reach and proprietary technologies focused on grinding efficiency and noise reduction. They continue to use trade events to reinforce product narratives and to accelerate specification wins with builders and plumbing wholesalers.

- Waste King / Anaheim Manufacturing (North Olmsted / Anaheim): Known for power and installation ease, Waste King remains relevant where performance and fast installation are procurement priorities. Their value proposition is high‑throughput models and installer friendliness — a defensive position in price‑sensitive segments.

- Moen Incorporated (North Olmsted): Moen’s integration of motor technologies with kitchen fixtures is a reminder that OEMs tied to larger kitchen platforms can leverage bundling opportunities — an attractive route to drive attach rates in both new builds and kitchen remodels.

- Franke (Aarburg, Switzerland): Franke occupies the premium European space, emphasizing low noise and durability. Their positioning makes them a natural fit for high‑end kitchens and for markets where brand prestige and long‑term reliability dominate purchase criteria.

- GE Appliances, Whirlpool, Teka: These firms illustrate two strategic realities — (1) appliance groups can profitably cross‑sell disposers as part of a broader kitchen ecosystem, and (2) their scale can be deployed to smooth material cost volatility via centralized procurement.

- New entrants and disruptors: Startups introducing re‑imagined units and approaches to handling “everyday” food waste are creating pressure on incumbents to improve user experience and reduce maintenance costs.

Recent market activity in early 2026 — including notable product launches and major trade‑show demonstrations — confirms that both incremental innovation and bold system re‑designs will shape specification cycles in the coming year.

Strategic implications and recommended actions for 2026

Based on our analysis, companies should prioritize a small number of high‑impact moves in 2026 to protect margin and capture demand:

- De‑risk procurement: Establish multi‑tier sourcing, negotiate longer hedges for critical metals, and consider near‑shoring or regional assembly to mitigate tariff exposure.

- Segmented product strategy: Invest selectively in performance and quietness for premium lines while simplifying value models for cost‑sensitive channels. Design modular platforms that reuse core engines across SKUs to reduce development and inventory costs.

- Channel and installer economics: Rework channel incentives to prioritize installers and plumbing wholesalers who can drive retrofit penetration. Offer bundled programs with kitchen fixture OEMs to accelerate attach rates.

- Regulatory market capture: Map municipal and state mandates to prioritize commercial accounts in jurisdictions where diversion laws create mandatory demand. Build certified kits and compliance documentation to shorten procurement cycles for institutional buyers.

- Service & recurring revenue: Pilot subscription or service bundles (maintenance, extended warranty, replacement parts) in markets with high instrument density to smooth revenue and improve lifetime customer value.

- M&A and partnerships: Use 2026 to scout distressed assets and technology plays — where valuation dislocations exist due to raw‑material stress or constrained working capital — and to partner with startups that offer clear OEM differentiators.

- Sustainability and circularity: Prepare a materials‑recovery narrative that supports ESG reporting and appeals to commercial buyers seeking to reduce landfill contributions; small investments in recyclability and take‑back programs improve buyer economics and brand positioning.

How PW Consulting supports your 2026 agenda

Our team blends industry experience in kitchen and plumbing channels with scenario‑based economic modeling. For 2026 execution we offer:

- Customized scenario workshops that stress‑test product portfolios under alternate tariff and raw‑material paths.

- M&A target assessment and diligence support focused on strategic fit and integration gains.

- Go‑to‑market playbooks for channel segmentation, installer economics, and specification capture in commercial channels.

- Operational playbooks to redesign supply networks for near‑shoring and to implement cost‑of‑goods engineering initiatives.

Closing — act with clarity, not haste

The kitchen food garbage processors market is mature yet dynamic; steady top‑line growth at a ~5% CAGR masks important cross‑currents. Tariff regimes, material prices and local waste‑diversion laws are rewriting the commercial calculus for manufacturers and channel partners. For decision‑makers, the question is not whether the market grows, but who captures value as it does. PW Consulting’s report translates that question into executable steps for 2026 planning cycles.

To review the full dataset, regional breakdowns, segment economics and downloadable financial models that underpin these recommendations, please consult the full report on our website — the complete segment‑level intelligence and granular tables are available there for subscription clients and advisory partners.

For detailed analysis of this topic, please visit the official page:Kitchen Food Garbage Processors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com