Why Acne Treatment Is One of the Best Ways to Restore Clearer, Healthier Skin in Viera

Health |

2026-06-24 11:47:43

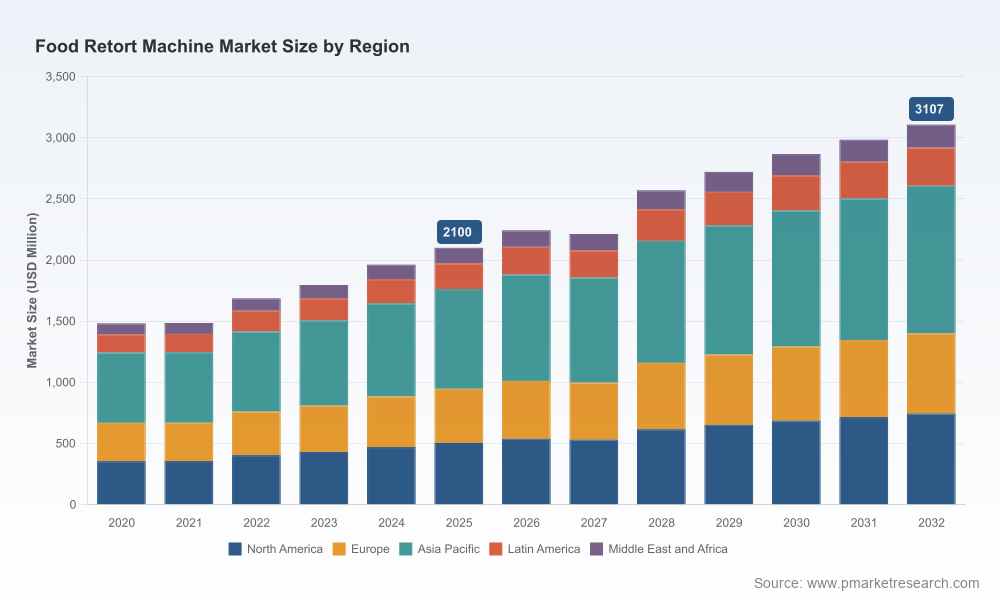

As food manufacturers and equipment suppliers prepare capital and product roadmaps for 2026, understanding where the food retort machine market is headed is no longer optional — it is a determinant of competitive survival. PW Consulting’s new Food Retort Machine Market report synthesizes seven years of historical performance and a multi‑scenario forecast to deliver decision‑ready intelligence. In short, the market has expanded from roughly USD 1.48 billion in 2020 to an estimated USD 2.10 billion in 2025 and is forecast to approach USD 3.11 billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.75% over the forecast period. The implications for capex planning, service strategy, M&A, and regulatory compliance are profound — and this briefing explains why.

Food Retort Machine Market

Shelf‑stable and ready‑to‑eat product demand is maturing into predictable volume growth, pushing processors to revisit sterilization capacity and flexibility. The steady market expansion signals both replacement cycles for legacy equipment and fresh investments for new product formats.

Food Retort Machine Market

Regulatory scrutiny is intensifying: validated thermal processes are not only a food‑safety requirement but a commercial imperative. FDA guidance under 21 CFR Part 113 and USDA FSIS requirements (e.g., on‑file process schedules and Processing Authority engagement) are shaping procurement criteria and supplier selection.

Food Retort Machine Market

Technology and aftermarket services are becoming the primary battleground. Advances such as optimized water immersion processes, rotary and continuous sterilizers, and automation for bag, can, bottle, and pouch formats create differentiation beyond simple equipment specs.

Supply‑chain and input‑cost dynamics — notably stainless steel price volatility and tariff exposure — are altering the TCO calculus. Procurement teams must fold alloy sourcing, local fabrication alternatives, and lifecycle serviceability into investment models.

Market structure remains neither fully consolidated nor atomized: the largest vendors command meaningful share but there is room for focused specialists and regional champions, creating both competitive and partnership opportunities.

This study is designed for executives who must act in 2026. Beyond headline sizing and macro trends, the report contains operational tools and executable playbooks that transform insight into action without exposing the granular segmentation tables in this summary. Key deliverables include:

Validated market sizing and high‑resolution forecast models (2026–2032) with scenario toggles for demand shocks, regulatory tightening, and material cost swings.

CapEx and TCO models that embed tariff scenarios, lifecycle maintenance, energy and water consumption, and validation/Processing Authority costs — enabling finance teams to stress‑test investment cases.

Supplier benchmarking templates and a reproducible scorecard for technical fit, aftermarket capability, software/data readiness, and regulatory support.

Go‑to‑market and sales enablement playbooks for equipment OEMs and service providers, including sample RFP language and retrofit commercialization paths.

M&A playbook and shortlists tailored to acquirers seeking technology bolt‑ons (e.g., immersion optimization, continuous retort capabilities) or aftermarket network expansion.

Regulatory compliance matrix and validation checklists aligned to FDA and FSIS requirements, plus practical templates for process schedules and audit readiness.

The competitive field is evolving in two dimensions: technology consolidation and service‑led differentiation. Key players profiled in the report illustrate divergent strategies that matter to potential partners and buyers.

Allpax Products, LLC — a U.S. OEM known for a broad portfolio of batch retort systems including advanced water‑immersion and dual‑mode designs, automated handling, and R&D units. Allpax’s demonstrations of immersion‑optimized processes and its presence at trade events underscore an emphasis on process efficiency and validation support for customers.

DTS Machinery Technology Co., Ltd. — a large China‑based manufacturer with deep experience in automated batch systems for multiple pack types. Their focus on automated batch retort systems and broad product reach is indicative of how volume manufacturing and aggressive pricing pressure global incumbents.

Sumpot (Zhucheng Jinding) — a long‑tenured sterilizer maker with a full suite of autoclave and retort solutions, representing the dependable regional supply options available to processors seeking local serviceability.

STOCK America / DFT Technology — together they illustrate the strategic value of proprietary process innovations: ImmersaFlow and related immersion technologies are being scaled into new product lines and promoted through shared channels, increasing the premium on process performance.

JBT Corporation — delivers retort and sterilization as part of integrated processing suites, emphasizing system‑level solutions and global service networks that appeal to larger processors seeking single‑vendor integration.

Innovaster and Surdry — examples of focused innovators: Innovaster advances high‑efficiency retort designs and rotary systems; Surdry emphasizes pilot and R&D‑grade retorts that accelerate NPD and packaging validation cycles.

Recent market moves underscore the tempo of change: strategic acquisitions and product showcases through late 2025 and early 2026 reflect both consolidation and innovation. Notably, the acquisition activity and product launches in the sterilization space are materially reshaping capability maps for buyers and the aftermarket service economics for sellers.

Compliance as competitive advantage: Under 21 CFR Part 113 and USDA FSIS guidance, processors must maintain documented, validated thermal processes. Vendors that bundle process validation, digital record‑keeping and Processing Authority liaison services will win share with risk‑averse customers.

Tariff and raw‑material pressure: With stainless steel forming the structural core of retort vessels, import tariffs and alloy price swings meaningfully affect delivered equipment costs and margins. Local fabrication strategies, modular designs that reduce exotic alloy use, and supplier hedging are practical mitigants.

Sustainability and utility constraints: Energy and water consumption are now procurement criteria; equipment that demonstrably reduces cycle energy or enables water recapture drives not only OPEX savings but faster procurement approvals in corporates with ESG mandates.

Reprice investments with a TCO lens that includes validation, Processing Authority engagement, and tariff exposure. Short‑term OPEX wins can mask long‑term validation and retrofit costs.

Invest in modular pilot capacity and R&D retorts to accelerate NPD cycles and shorten time‑to‑market for new packaging formats — an approach that rewards both brand owners and co‑packers.

Build or buy aftermarket service networks and digital monitoring capabilities; recurring service revenue is a multiplier on hardware margins and a core retention lever.

Pursue focused M&A to acquire process innovations and service footprints rather than broad product portfolios. Acquisitions that bring proprietary process gains (e.g., immersion optimization) or dense regional service networks compound value quickly.

Embed regulatory validation into product design: offer equipment with pre‑validated recipes, integrated data logging, and migration paths to digital process control — a marketable differentiator in highly regulated segments.

Executives tell us they need not only market directionality but executable deliverables: models to build business cases, playbooks to commercialize retrofit programs, and validated lists of acquisition targets and suppliers. The PW Consulting Food Retort Machine Market report packages these items into an operational toolkit, including interactive spreadsheets, supplier scorecards, sample RFPs, and compliance checklists. To preserve competitive value for subscribers, we have intentionally withheld certain granular segmentation tables from this public briefing — these are included in the full report and client dashboards.

If your 2026 planning includes capex approvals, M&A diligence, product roadmaps, or service expansion in thermal processing, this study will save months of work and materially de‑risk your decisions. For access to the full dataset, segmentation breakdowns, and the downloadable toolkit, please contact PW Consulting through our corporate channels to request the complete report and a tailored briefing.

For detailed analysis of this topic, please visit the official page:Food Retort Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com