Neem Oil and Concentrates Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-18 10:07:29

As apparel executives and investors plan capital allocation and sourcing strategies for 2026, an evidence-based view of the polyester fiber landscape is essential. PW Consulting’s latest market study — covering historical performance through 2025 and a forward-looking forecast into 2032 — distills the commercial, regulatory, and technology dynamics that will drive competitive advantage in polyester-based apparel. This briefing highlights the report’s decision-useful takeaways and explains how leadership teams can convert the study’s insights into executable 2026 strategies. (Note: this release intentionally omits granular segment-level figures; the full intelligence package on PW Consulting’s report page contains those data and proprietary scorecards.)

Polyester Fiber In Apparel Market

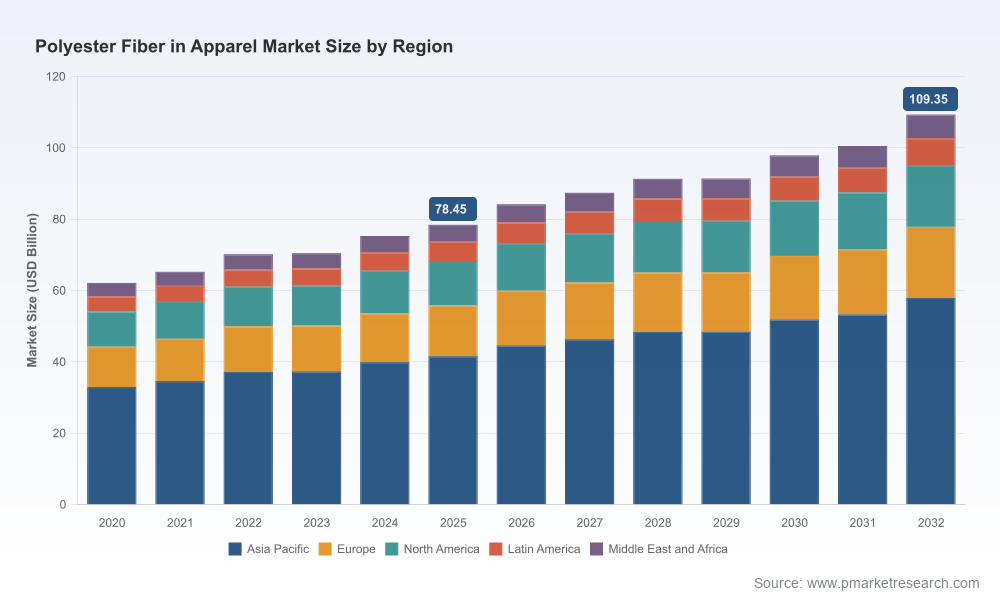

Polyester fiber for apparel is mid-cycle but structurally expanding. After growing through the early 2020s, the apparel-oriented polyester market reached approximately USD 78.45 billion in 2025. PW Consulting’s base-case forecast shows a steady expansion at a compound annual growth rate (CAGR) of roughly 4.86% over the 2026–2032 horizon, underpinning a market size above USD 100 billion by the early 2030s. This trajectory reflects ongoing demand resilience in sportswear, athleisure, and casualwear categories, even as fashion cycles and sustainability imperatives reshape sourcing and product design.

Polyester Fiber In Apparel Market

Regulatory and compliance timelines crystallize. Several regulatory milestones — including product-level chemical restrictions and material composition rules in major markets — become binding during 2026. These rules will require immediate changes to manufacturing specifications, supplier contracts, and labelling practices for many apparel businesses.

Polyester Fiber In Apparel Market

Input cost volatility creates procurement risk. Feedstock price swings and supply tightness for polyester intermediates have shown sharper, more frequent moves in recent quarters, increasing the cost risk for vertically integrated players and contract manufacturers alike.

Sustainability commitments are becoming operational targets. What had been “brand marketing” goals are now procurement metrics and product requirements for large retailers and institutional buyers; recycled and traceable polyester is moving from niche to mainstream supply-chain criteria.

The full report is designed as an operational playbook for 2026 decision cycles. Key components include:

Market sizing and scenario forecasts (base, upside, downside) that quantify demand under varying macroeconomic, regulatory, and feedstock cost scenarios.

Value-chain maps and cost curves showing where margin compression is most likely to occur under feedstock volatility — and which nodes offer the most leverage for margin recovery.

Supplier benchmarking and a modular supplier scorecard template covering capacity, traceability, chemical compliance, and recycled-content traceability — intended for rapid integration into supplier risk management systems.

Regulatory impact matrices that translate new chemical restrictions and trade-policy shifts into product-change roadmaps and compliance timelines for sourcing, R&D, and production teams.

Commercial playbooks for procurement: hedging strategies, long- vs short-term contracting models, and criteria for nearshoring vs global sourcing considering tariff and logistics dynamics.

Investment and M&A scorecards identifying attractive targets across the polyester value chain (e.g., recycling-focused assets, specialty fiber manufacturers, integrated PTA/PET platforms) with quantified upside levers and integration risks.

Technology watch and adoption roadmaps for emerging materials (e.g., biodegradable polyesters, bio-based feedstocks, and CO₂-derived intermediates) and for manufacturing technologies that reduce microplastic shedding.

The polyester fiber ecosystem combines global integrated petrochemical champions, regional-scale specialists, and an expanding set of recycling-focused entrants. Market concentration is moderate: the top three players account for a meaningful share of capacity, and top-five concentration increases further — a profile that supports continued investment by scale players while leaving niches for specialized and sustainability-focused challengers.

Reliance Industries Limited (Mumbai) — A globally integrated heavy hitter with multi-million-tonne capability. Reliance’s strategy mixes scale polyester production with a push into traceable recycled products and specialty fibers. Recent launches of a verified 100% post-consumer recycled fabric and thermal/specialty fiber showcases indicate a coordinated product-plus-traceability play that targets premium performance and sustainability-focused apparel customers.

Indorama Ventures (Bangkok) — A global leader in both staple fiber and filament yarn, actively deploying recycling capacity through joint ventures and strategic partnerships. Indorama’s recent JV to add substantial textile-rPET spinning capacity underscores a corporate strategy to lock in circular feedstocks at scale, reducing exposure to virgin feedstock volatility.

Toray Industries (Tokyo) — A technology- and specialty-oriented competitor focused on high-performance and recycled grades for technical apparel. Their product orientation provides margin resilience where commodity producers face pressure.

Large Chinese integrated groups (Tongkun, Hengyi, Hengli, Sinopec Yizheng) — These firms leverage vertical integration into PTA/PET to manage raw material exposure and deliver cost-competitive apparel-grade polyester at scale. Their role is critical to global pricing dynamics and availability in Asia-focused supply chains.

Regional and recycling-focused players (FENC, Nan Ya, Alpek, Thai Polyester, Rashni Poly, Everra, William Barnet & Son, Stein Fibers) — This set includes both legacy suppliers and specialist recyclers. They are pivotal enablers for brands seeking verified recycled content or regional supply security, and they are common acquisition targets for brands and larger industrial players seeking circularity credentials.

Scaling circularity through JV capacity: Strategic joint ventures to expand textile-rPET spinning capacity materially change the economics of recycled polyester at scale and shorten the timeline for recycled-content compliance in apparel specifications.

Product launches targeting traceability and performance: New commercialized traceable post-consumer recycled fabrics and specialty fibers enable brands to combine performance claims with sustainability narratives, opening premium pricing paths for early adopters.

Emergent biodegradable polyester blends: Debuts of biodegradable polyester technologies aimed at luxury and home-textile segments signal a longer-term route to address microplastic concerns, but commercial adoption timelines remain dependent on cost parity and regulatory incentives.

Raw-material and trade-policy noise: Recent years have seen material production increases globally alongside episodes of PTA/MEG price volatility and tightening. Coupled with higher apparel import tariff profiles in some major markets, these dynamics make supply-chain mapping and tariff-aware sourcing critical to avoid margin erosion.

Regulatory deadlines: New chemical restrictions with enforcement dates in 2026 require immediate operational compliance actions, from supplier audits to changes in equipment and material specifications.

Implement a two-track sourcing strategy: secure short-term price and availability through tactical contracts while negotiating long-term offtake and JV opportunities for recycled feedstock to insulate against upstream volatility.

Fast-track supplier compliance and traceability audits: prioritize suppliers with third-party verification of recycled content and documented chemical compliance to meet impending regulatory milestones.

Reassess product mixes and value pools: deploy the report’s price/elasticity models to determine where premiumization (performance/recycled claims) will justify higher input costs and where cost-optimization is imperative.

Consider targeted M&A or strategic partnerships: buyers should prioritize recycling assets, specialty fiber capabilities, or integrated PTA/PET platforms that offer insulation from feedstock shocks and speed-to-market for circular products.

Embed regulatory scenario planning into product roadmaps: align R&D and sourcing timelines with known compliance dates to reduce forced redesigns and rushed procurement in 2026.

This brief surfaces the strategic contours that will matter in 2026, but the value to corporate decision-makers lies in the proprietary datasets, supplier scorecards, and scenario-models contained in PW Consulting’s full study. The report’s granular modules translate headline market growth into regionally differentiated procurement impacts, supplier-level risk matrices, and quantified M&A case economics — elements we intentionally withhold in this public summary to preserve their operational value.

For leadership teams preparing budgets, negotiating supplier contracts, or evaluating acquisition targets in 2026, the full PW Consulting Polyester Fiber in Apparel market report provides the evidence base, tools, and checklists to convert market trends into defensible, time-sensitive actions. Access to the full dataset and modular playbooks will enable quicker, less error-prone decisions at a moment when margin pressure, compliance deadlines, and sustainability commitments collide.

Executives wishing to translate these insights into 2026-ready plans should engage PW Consulting for a tailored briefing and interactive workshop. Our team can deploy the report’s scenario models against a company’s specific product portfolio and supply base to produce an actionable 90-day roadmap.

For detailed analysis of this topic, please visit the official page:Polyester Fiber In Apparel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com