Powdered Glass Market 2026 Strategic Brief: Pathways to Competitive Advantage and Risk Mitigation

Executive summary

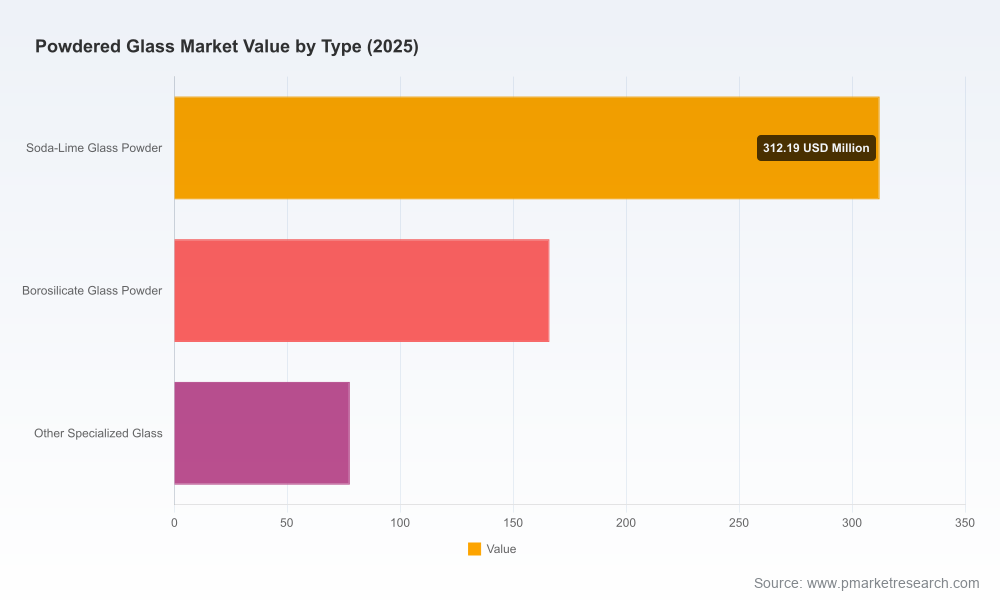

PW Consulting’s latest Powdered Glass Market report (base year 2025; historical analysis 2020–2025; forecast 2026–2032) delivers a decision-grade view for executives planning allocations, M&A, or technology investments in 2026. The market reached USD 556.04 Million in 2025 and, under our base forecast, expands to roughly USD 795.5 Million by 2032, representing a mid-single-digit compound annual growth profile (CAGR 5.25% for 2026–2032). The expansion is structural — reflecting demand for low-carbon construction materials, specialty electronics substrates, advanced biomedical powders, and enhanced functional fillers — but it is also nuanced, with pockets of rapid premiumization and areas of price-competitive commoditization.

Powdered Glass Market

Why this matters for 2026 strategy

- Market momentum is measurable yet uneven: steady overall growth masks divergent value capture between high-purity specialty powders and recycled/commodity fillers. Executives who misread this balance risk over-investing in low-margin segments or missing premium niches enabled by advanced processing.

- Sustainability and regulation are reshaping purchase criteria. Recycled glass solutions are no longer just cost-driven alternatives — they are strategic inputs to low-carbon concrete and circular-product value propositions. Simultaneously, investigations and trade scrutiny around certain quartz surface products are creating policy and market risk that buyers and suppliers must actively model into 2026 procurement and sales plans.

- Technology and scale are differentiators. Proprietary milling, ultrafine particle control, and full-process chain mastery are the competitive moats for suppliers selling into high-value electronics, medical, and optical markets.

What the report contains (practical, executable intelligence)

PW Consulting’s report is purposely tactical for 2026 decision makers. It combines quantitative market-sizing and forward scenario projections with actionable frameworks and tools:

Powdered Glass Market

- Verified historical sizing (2020–2025) and a 2026–2032 forecast built on bottom-up capacity, demand-by-application modeling, and macro-supply assumptions.

- Segment-level playbooks (by product type, application family, and supply model) that translate market dynamics into route-to-market and pricing options without requiring in-house modeling teams.

- Supplier scorecards and a procurement negotiation toolkit that cover technical KPIs (particle-size distributions, specific surface area, free silica content), sustainability credentials (cullet share, embodied CO2), and logistics risk.

- Manufacturing and capex decision matrices comparing milling technologies, process chain integration, and unit economics for virgin vs recycled feedstock lines.

- Regulatory monitoring templates and a risk matrix for trade actions, standards adoption, and product safety testing relevant to 2026 compliance planning.

- Customized M&A and partnership playbooks: target filters, valuation sensitivities, and integration checklists for buyers seeking vertical integration or recycled feedstock control.

Market dynamics and structural drivers

The powdered glass market is being reshaped by three intersecting dynamics:

Powdered Glass Market

- Sustainability-led demand: The construction sector’s pivot to low-carbon materials is elevating recycled glass powders from commodity filler to engineered supplementary cementitious material in specified applications. New consensus standards for glass pozzolans have reduced technical barriers, making recycled streams attractive to downstream formulators focused on carbon intensity and circularity claims.

- Advanced-application premiumization: Electronics, medical, and advanced optical applications continue to require ultra-high-purity and tightly controlled particle distributions. Suppliers who can offer ultrafine, low-impurity powders with reliable supply chains are capturing premium pricing and long-term OEM agreements.

- Supply-chain and feedstock risk: Virgin high-purity silica feedstocks remain geographically concentrated. Conversely, cullet-based supply requires investment in sorting and processing infrastructure to achieve consistent quality. Each ton of cullet used upstream materially reduces raw-material demand and energy intensity versus virgin routes — a structural advantage but one that depends on local collection and processing economics.

Competitive landscape — strategic positions and implications

The competitive map is a mix of specialty incumbents, recycled-material leaders, and regional producers. Key observations:

- Integrated specialty producers with process control and proprietary milling technology hold asymmetric advantage in high-value niches. Their capabilities — from sub-micron particle engineering to functionalized surface chemistries and full-process-chain control — drive stickier commercial relationships with OEMs in electronics, medical, and energy applications.

- Recycled-focused players and precision recyclers are leveraging sustainability mandates and standards acceptance to expand into construction and industrial filler markets. These firms are winning projects where embodied carbon and recycled content are procurement criteria.

- Large glass manufacturers and diversified chemical groups are extending supply agreements and making targeted investments (including capacity and upstream cullet acquisition) to secure feedstock and protect margin in growth segments.

Profiles in the report synthesize each major player’s strategic assets — from proprietary ultrafine grinding and patented processes to geographic footprint and product breadth — and translate them into opportunity maps for buyers, suppliers, and investors.

Notable recent industry moves (implications, not confidential figures)

- Capacity strategic plays: A North American recycled-glass producer recently commissioned a new processing line to increase its ability to serve low-carbon concrete demand. For buyers, this signals improved availability of qualifying recycled powders in regional markets; for competitors, it raises the bar on feedstock integration and logistics.

- Product innovation: A leading specialty glass manufacturer launched an advanced bioactive powder range with improved ion-release profiles and tighter particle uniformity for dental and regenerative applications — underscoring that R&D-driven differentiation remains a clear route to premium segments.

- Commercial tie-ups: Suppliers of ultra-fine virgin grades have secured multi-year agreements to serve next-generation display and substrate programs. These arrangements highlight the strategic importance of guaranteed supply for high-spec OEMs and the willingness of buyers to lock in long-term partners for technical-critical inputs.

- M&A and consolidation: Established players have completed acquisitions to broaden access to cullet and accelerate entry into construction-grade recycled powders — a trend likely to continue as firms pursue secure feedstock and scale economics.

Risks executives must model in 2026

- Policy and trade actions: Ongoing investigations and trade scrutiny into certain surface products and silica-containing imports increase regulatory tail risks. Companies with export-exposed supply chains should prioritize scenario planning and legal counsel.

- Feedstock concentration: Dependence on high-purity virgin raw materials or on localized cullet streams creates vulnerability to regional supply shocks or logistic bottlenecks.

- Technological obsolescence: Suppliers that fail to invest in ultrafine milling and quality consistency risk being squeezed out of premium applications by competitors with tighter specifications.

- Reputational and safety exposures: Product formulations containing crystalline silica or poorly characterized fines invite both regulatory and liability risks; robust materials characterization and chain-of-custody practices are now table stakes.

Recommendations — a prioritized 2026 playbook

For senior leaders, PW Consulting recommends a three-horizon set of actions designed to capture upside while insulating operations from downside shocks:

- Short term (0–12 months): Conduct a rapid procurement audit focusing on feedstock quality variability, logistics lead times, and supplier concentration. Initiate pilot qualification runs with recycled powder suppliers to validate performance and sustainability claims.

- Medium term (12–36 months): Invest selectively in ultrafine milling capability or contract long-term with specialty suppliers to secure high-spec product lines. Build a regulatory watch function tied to trade investigation outcomes and standards adoption to preempt compliance disruptions.

- Long term (36+ months): Evaluate vertical integration or targeted acquisitions of cullet processors and strategic recycling assets to lock in low-carbon feedstock. Consider geographic diversification of manufacturing to reduce single-region exposure for critical high-purity grades.

Key metrics to track in 2026

- Feedstock mix (virgin vs recycled) and its impact on unit CO2 intensity;

- Particle-size distribution compliance rates for premium product lines;

- Order-book visibility for high-value OEM contracts and the share of revenue under multi-year supply agreements;

- Regulatory developments and trade probe timelines affecting surface products and silica-containing imports.

Conclusion — positioning for profitable growth

The powdered glass market presents a clear growth runway, anchored by sustainability transitions and advanced-application demand. But the landscape rewards specialization, supply-chain foresight, and regulatory agility. PW Consulting’s report equips decision makers with the quantitative market context (historical and forecast sizing), a map of competitive strengths, and a suite of transaction-ready playbooks to act confidently in 2026 — while protecting against policy and feedstock shocks.

Next steps

Executives seeking the detailed segmentation, proprietary supplier scorecards, and downloadable scenario models that underpin this brief are invited to access the full report or contact PW Consulting for a tailored executive briefing. The full report contains the granular datasets and interactive dashboards necessary to operationalize the strategies summarized here.

For detailed analysis of this topic, please visit the official page:Powdered Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com