Navigating the Cosmos: How HorosTalk is Revolutionizing Online Astrology Consultations

Other |

2026-06-18 04:25:13

As retail leadership teams prepare their 2026 roadmaps, the imperative is clear: omni‑channel commerce is no longer an optional layer—it is the backbone of modern retail strategy. PW Consulting’s latest market research on the Retail Omni‑Channel Commerce Platform market (base year 2025; historical period 2020–2025; forecast 2026–2032) delivers the forward‑looking intelligence organizations need to align investment, technology and operating choices with resilient growth. The study synthesizes multi‑year trajectory analysis, vendor benchmarking, and practical deployment guidance designed for CIOs, CMOs, CFOs and Heads of Digital Commerce who must translate uncertainty into differentiating advantage.

Retail Omni Channel Commerce Platform Market

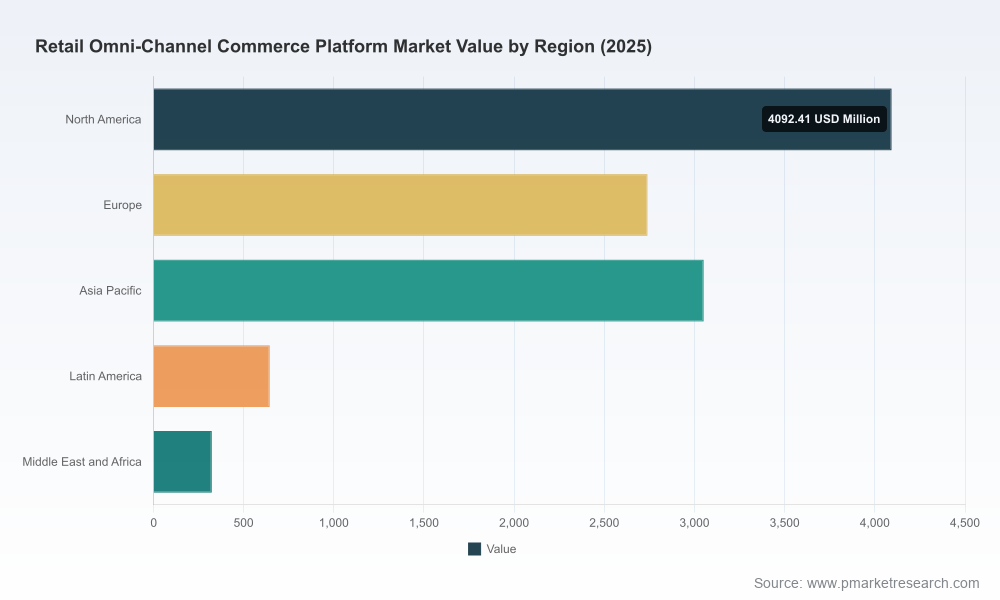

From 2020 through 2025 the global omni‑channel commerce platform market demonstrated accelerated adoption, evolving from early omnichannel experiments to mission‑critical platforms that orchestrate online, in‑store and marketplace touchpoints. Our analysis documents robust expansion across the historical window and forecasts sustained momentum through 2032. Over the forecast period PW Consulting models the market to grow at a compound annual growth rate (CAGR) consistent with double‑digit digital infrastructure and software adoption trends, reflecting rising demand for unified inventory, composable architectures, and AI‑driven personalization.

Retail Omni Channel Commerce Platform Market

For executives deciding on platform consolidations, partnership models or greenfield deployments in 2026, two realities should shape choices: (1) scale matters—but so does composability. The market shows moderate concentration among leading suppliers, yet the mid‑market and specialist vendors continue to capture niches where agility and vertical specialization trump scale. (Our report quantifies concentration and competitive dynamics for board‑level decision making.) (CR3 ~38.5%; CR5 ~52.1%).

Retail Omni Channel Commerce Platform Market

Actionable adoption frameworks: a staged roadmap (assess → pilot → scale) that maps technical choices—headless vs. monolithic, cloud vs. on‑premise, composable APIs—into concrete business milestones and KPI targets for the first 24 months of deployment.

Vendor playbooks: side‑by‑side capability matrices that highlight integration velocity, commerce + CRM synergy, POS and inventory orchestration strengths, and managed services options—scored for enterprise size, geographic footprint and vertical requirements.

Integration and migration patterns: pragmatic templates for migrating catalogs, orders and customer records while preserving continuity of service and minimizing data risk—addressing common pitfalls observed in cross‑border rollouts and replatforming programs.

Commercial models and TCO: scenario‑based total cost of ownership modeling that incorporates software licensing, cloud infrastructure, integration services and ongoing operations—designed to support board and procurement negotiations.

Risk & compliance playbook: a compliance checklist and data architecture patterns that align with evolving privacy regimes and cross‑border data sovereignty constraints, helping legal, privacy and IT teams operationalize regulatory requirements without derailing commerce velocity.

Executives rarely need more data; they need the right translation of data into choices. Our report blends the market’s topline trajectory with scenario analysis to inform three immediate 2026 decisions:

Platform consolidation vs. best‑of‑breed: For retailers targeting aggressive omnichannel parity, the report evaluates the tradeoffs between integrated suites and composable, API‑first stacks—linking each option to payback timelines under realistic revenue and cost uplift assumptions.

Cloud posture and resilience budgeting: Given rising data center costs and ongoing cloud consumption growth, the study provides guidance on optimizing hybrid architectures and negotiating colocation and cloud contracts to preserve margin while meeting latency and sovereignty constraints.

AI and personalization investments: We quantify where incremental personalization capability (product recommendations, search, dynamic pricing) yields measurable lift for different verticals and customer lifetime value cohorts—helping prioritize pilot investments in 2026).

Our analysis profiles the ecosystem that matters for enterprise omni‑channel programs. The competitive map includes global systems integrators, cloud hyperscalers, legacy enterprise suites and purpose‑built commerce platforms. Key vendor profiles in the report assess enterprise readiness across integration, scalability, industry specialization and partner ecosystems.

Shopify Inc. — Recognized for Shopify Plus and its headless capabilities that streamline online‑to‑offline inventory synchronization and POS integration; attractive for brands seeking rapid commerce velocity with modern storefront frameworks.

Salesforce, Inc. — Salesforce Commerce Cloud’s strength is CRM and marketing orchestration combined with embedded AI for personalization, making it a compelling option where unified customer engagement is the priority.

Adobe Inc. — Adobe Commerce continues to be chosen where content‑driven commerce and experience management are central to the value proposition, especially where commerce and CMS consolidation is required.

Oracle, SAP and Microsoft — These enterprise suites remain the default for large scale retail operations that require deep back‑office unification, inventory optimization and complex B2B/B2C hybrids.

Composable and specialist players (commercetools, Elastic Path, VTEX, BigCommerce, Manhattan Associates, Lightspeed, and others) — Offer focused advantages around MACH architectures, marketplace integrations, and verticalized functionality that accelerate time‑to‑value for specific segments.

Each vendor has distinct strengths and constraints: from Shopify’s developer‑friendly headless tools to Salesforce’s cross‑cloud convergence, to Adobe’s content depth and the traditional ERP alignment of SAP/Oracle. Our vendor playbooks do more than list features—they map those capabilities into procurement scenarios, partnership models and transitional risk profiles for 2026 initiatives.

The market continues to evolve through rapid integrations and ecosystem partnerships. Recent platform updates and partnerships—announced during early 2026—underscore two tactical themes:

Globalization made operational: native integrations that simplify multi‑region, multi‑currency, and multi‑language management reduce friction for retailers expanding internationally. For 2026 planning, this means earlier go‑to‑market launches with less custom engineering overhead.

Channel breadth matters: partnerships that expand product feed and marketplace reach increase the marginal effectiveness of omnichannel stacks—making channel orchestration a crucial capability rather than a “nice to have”.

Operational takeaways for 2026 include prioritizing API‑first vendors where quick regional launches are strategic, and locking in channel feed and marketplace partners early to capture peak season advantages.

Regulation and infrastructure cost are no longer background noise; they actively shape feasibility and economics. New privacy laws and data sovereignty pressures—both at the state level in the U.S. and internationally—necessitate redesigned customer data architectures that limit unnecessary replication and impose stricter controls on cross‑border transfers. The report includes a pragmatic compliance sequencing guide to help teams meet legal obligations without sacrificing personalization efficacy.

On the infrastructure side, contemporary data center dynamics—rising construction and colocation costs coupled with sustained cloud demand—mean that cloud consumption should be architected for cost predictability. We provide cloud rightsizing templates, multi‑region latency maps and vendor negotiation playbooks that finance and cloud teams can deploy immediately.

Immediate (0–3 months): perform a platform risk/opportunity triage that maps revenue impact against migration complexity. Use our rapid assessment worksheet to prioritize 1–2 high‑value pilots.

Near‑term (3–12 months): select an integration pattern (suite vs. composable) and begin a single‑market pilot, instrumented for measurable KPIs—conversion, store fulfillment rate, and customer lifetime value uplift.

Medium term (12–24 months): scale the winning pattern across regions while deploying the report’s compliance and data sovereignty blueprint to prevent regulatory friction during expansion.

Boards and executive committees can use the report to: (1) validate the economics of platform investment with scenario modeling; (2) assess competitive positioning relative to peers and suppliers; and (3) set governance guardrails that balance speed with risk. The research is intentionally structured to support board decks with executive summaries, financial impact tables, recommended KPIs and vendor negotiation checklists.

This briefing is a strategic teaser—designed to equip leaders with immediate, high‑confidence directional insight while preserving the detailed segment matrices, vendor scoring, and downloadable TCO models that form the core of PW Consulting’s market offering. For procurement teams, integration leads and strategy committees seeking the underlying datasets, segmented demand models, and executable templates, the full report and accompanying toolkits are available through our market research portal.

PW Consulting’s Retail Omni‑Channel Commerce Platform Market research provides the combination of empirical trend analysis, vendor insight and tactical playbooks required to make defensible, opportunity‑focused decisions in 2026. For leaders who must move from aspiration to delivery, the report is both a map and a set of tools—enabling faster, safer and more profitable omni‑channel transformation.

For detailed analysis of this topic, please visit the official page:Retail Omni Channel Commerce Platform Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com