Breaking: E-Bike Drive Market Poised for Unprecedented Growth

Other |

2026-05-20 08:52:48

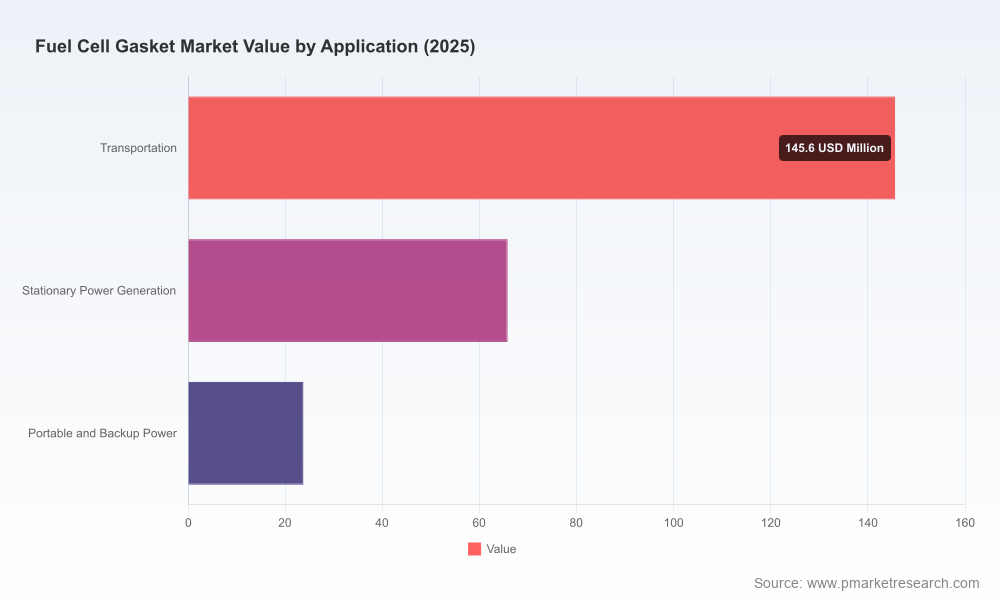

As fuel cell deployments accelerate across mobility, stationary power and backup applications, gasket technology is emerging as a critical enabler of system reliability, efficiency and cost-of-ownership. PW Consulting’s latest Fuel Cell Gasket Market study (base year 2025, historical 2020–2025, forecast 2026–2032) synthesizes market sizing, technology trajectories and commercial playbooks tailored for executive decisions in 2026. The study models the global gasket market rising from an estimated USD 235.09 Million in 2025 to USD 684.72 Million by 2032, tracking at a robust 16.5% CAGR over the forecast period — a growth profile that will materially affect supplier strategies, OEM procurement and investor appetite this year.

Fuel Cell Gasket Market

Actionable growth signals: The quantified market expansion and scenario modeling identify where volume growth will outpace component-level value capture — information executives need to prioritize capacity investments, allocate R&D, and set pricing guardrails.

Fuel Cell Gasket Market

Supply-side stress testing: Our analysis evaluates raw-material cost volatility, manufacturing constraints and automation levers, helping procurement and operations teams design hedging strategies and capital plans that preserve margin under varying hydrogen commercialization trajectories.

Fuel Cell Gasket Market

Regulatory and standards foresight: The study integrates recent shifts in regulatory frameworks and material policy (including the rise of PFAS-free initiatives and updated hydrogen lifecycle models) to align product development, certification pathways and go-to-market timing with anticipated compliance milestones.

Competitive playbooks: Rather than an inventory of vendors, the report decodes supplier capabilities, strategic moves and partnership archetypes that will determine winners in 2026 — guiding M&A, JV and sourcing decisions.

Top-line forecast and scenario analysis (base year 2025): a three-tier forecast model (baseline, accelerated adoption, supply-constrained) that reconciles system-level fuel cell deployments with per-stack gasket demand drivers.

Unit and revenue modeling: component-level build-up from stack counts to gasket formats and material mixes, presented in USD Million and unit demand across 2026–2032.

Materials and cost-to-serve mapping: engineering-grade profiles for commonly used elastomers and thermoplastics, assessment of material availability and substitution pathways, and sensitivity testing of margin impact under realistic raw-material price swings.

Manufacturing and quality playbook: process design options from die-cutting to high-pressure molding, inline automation examples (including high-speed dispensing and UV-curing integration), cycle time economics and QC test matrices for hydrogen permeation, compression set and thermal aging.

Commercial and aftermarket strategies: OEM qualification roadmaps, channel economics for Tier-1 vs commodity suppliers, spare-part lifetime modeling and serviceable-aftermarket revenue pools.

Risk register and mitigation playbook: supplier concentration, single-source exposures, critical mineral dependencies and recommendations to de‑risk through geographic diversification, dual-sourcing and strategic inventory sizing.

The market is neither a pure commodity nor a closed oligopoly. Our concentration analysis shows meaningful scale among leading suppliers — the three largest firms together hold a significant share of installed expertise and qualification relationships, while the top five control a majority of identified revenue in the sector. This dual reality means that partnerships with a handful of established sealing specialists can accelerate OEM qualification, yet there remains room for agile, differentiated entrants focusing on material innovation, process automation and aftermarket capture.

Key incumbents and specialized suppliers are actively repositioning to capture fuel cell opportunities, and their moves offer clear lessons for 2026 strategy-setting.

Freudenberg Sealing Technologies (Weinheim, Germany): Following a recent organizational integration that folded hydrogen components into core sealing operations, Freudenberg is leveraging elastomer mixing and process scale to tighten its value chain. The company’s investments in localized elastomer capacity and stack-level integration signal a play to own more of the assembly economics — a blueprint for suppliers willing to vertically integrate.

NOK Corporation (Tokyo, Japan): NOK’s focus on integrated separator-and-gasket architectures demonstrates the margin lift possible from systems thinking. Their approach underscores that technical differentiation — not only material selection — wins long qualification cycles with OEMs.

Trelleborg Sealing Solutions (Trelleborg, Sweden): With hydrogen-validated material platforms, Trelleborg is emphasizing validated H2-ready compounds and comprehensive testing dossiers. This highlights how third-party validation and material branding can reduce perceived risk for conservative automotive and stationary power buyers.

Parker Hannifin Corporation (Cleveland, USA): Parker’s broad product portfolio — from injected elastomer to PTFE seals — positions it as a flexible supply partner for both fuel cells and electrolyzers, an advantage for OEMs seeking supplier consolidation across hydrogen subsystems.

ElringKlinger AG (Dettingen an der Erms, Germany): The firm’s metal-elastomer hybrid gaskets and public showcases at mobility events demonstrate migration pathways from established combustion and battery sealing technologies into fuel cells, making ElringKlinger an attractive partner for OEMs that value cross-powertrain commonality.

Stockwell Elastomerics (Philadelphia, USA) and regional specialists: Firms focused on high-consistency silicone formulations and thin-sheet die-cutting present a different playbook — targeted material performance leadership and manufacturing nimbleness that serve as attractive acquisition or supply targets for larger groups seeking speed-to-market.

Regional rubber specialists (Japan, Denmark, China): A cadre of specialized suppliers remains critical for local OEMs and tiered supply chains. Their technological know-how in EPDM, FKM and silicone compounds and their proximity to hydrogen deployments keep them strategically relevant.

Automation advances: The October 2025 launch of an automated high-speed dispensing system combining fast-curing liquid gaskets with UV technologies signifies that sealing cycle times — historically a bottleneck — can be reduced while improving process repeatability. For manufacturers, this makes near-shore and high-mix, low-volume production economically viable.

Organizational consolidation: Structural moves by large sealing houses to consolidate hydrogen components under sealing divisions indicate an industry trend toward integrated hydrogen product platforms; firms should evaluate whether to compete on components, subsystems or both.

Market signals from trade showcases: Public demonstrations of metal-elastomer and validated hydrogen materials at mobility events reinforce the point that proven performance in harsh environments is becoming table stakes for partners to supply automotive OEMs.

Policy tailwinds: Updated hydrogen lifecycle models and expanded recognition of diverse hydrogen production pathways are lowering systemic policy risk for component suppliers, indirectly supporting demand for fuel cell gaskets as hydrogen projects enter procurement phases.

Material cost and substitution pressure: Volatility in specialty elastomer supply will continue to pressure margins. Suppliers who can qualify lower-cost equivalents or proprietary PFAS-free alternatives while maintaining tight performance tolerances will gain negotiating leverage.

Qualification cadence and lead times: Gasket qualification for automotive and stationary power players remains lengthy. Firms that invest in standardized test protocols and pre-qualification packages will shorten sales cycles and capture early-spec opportunities.

Integration vs. specialization: The market rewards both vertically integrated players that deliver system-level solutions and niche specialists that provide breakthrough materials or manufacturing techniques. Choose your competitive posture deliberately and align capital allocation accordingly.

Aftermarket and service economics: As fleets and stationary assets scale, aftermarket gasket replacements and serviceable components will create annuity-style revenue streams that can double down on initial system sales.

Prioritize dual sourcing for critical elastomers and implement input-cost pass-through mechanisms to protect margins against feedstock shocks.

Invest selectively in automation that reduces cycle time and increases first-pass yield; consider partnerships with dispensing and curing system providers to accelerate implementation.

Develop PFAS-free material roadmaps and secure early OEM co-validation to turn regulatory pressure into competitive advantage.

Use qualification accelerators — standardized test packs, field demo programs and shared validation labs — to shorten OEM time-to-spec while maintaining IP protection.

Evaluate M&A targets not just for revenue but for access to material chemistries, qualification dossiers and regional OEM relationships that can be scaled quickly.

Our study provides the quantitative scaffolding and tactical playbooks to convert the market’s 16.5% CAGR trajectory into executable 24–36 month roadmaps. For leadership teams evaluating manufacturing investments, supplier alliances or M&A, the report offers a granular yet operationalized assessment tuned to 2026 decision calendars: market sizing by component and scenario, supplier scorecards, process-cost models and a prioritized list of near-term actions that materially reduce procurement and qualification risk.

PW Consulting’s Fuel Cell Gasket Market report is deliberately data-rich but selective in what we publish publicly — we present high-confidence strategic conclusions and illustrate methodologies here while reserving the granular subsegment tables, regional build-ups and bespoke supplier scorecards for the full report package. For companies that must act in 2026, that granularity is the difference between informed risk-taking and costly hindsight.

Contact PW Consulting to request the full Fuel Cell Gasket Market report and receive an executive briefing tailored to your role — whether you lead procurement, manufacturing, product engineering or corporate development. The full report includes detailed segmentation, supplier profiles, unit economics and a prioritized implementation roadmap that will support fast, confident decision-making in 2026.

For detailed analysis of this topic, please visit the official page:Fuel Cell Gasket Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com