Space Lithium‑Ion Batteries Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

As space programs diversify across commercial, defense, and scientific missions, lithium‑ion battery systems have become strategic assets — not merely components. PW Consulting’s forthcoming Space Lithium‑Ion Batteries Market report (base year 2025, forecast period 2026–2032) crystallizes how this sector will evolve and what decisions enterprise leaders must prioritize in 2026 to capture value and manage risk. The report projects a compound annual growth rate (CAGR) of 14.0% across the forecast window and maps a clear trajectory from 2025’s market base into robust expansion through 2032. This preview outlines the report’s strategic takeaways, competitive dynamics, and operational guidance while preserving the detailed datasets and segment-level numbers for subscribers and qualified purchasers.

Space Lithium Ion Batteries Market

Why this market matters in 2026

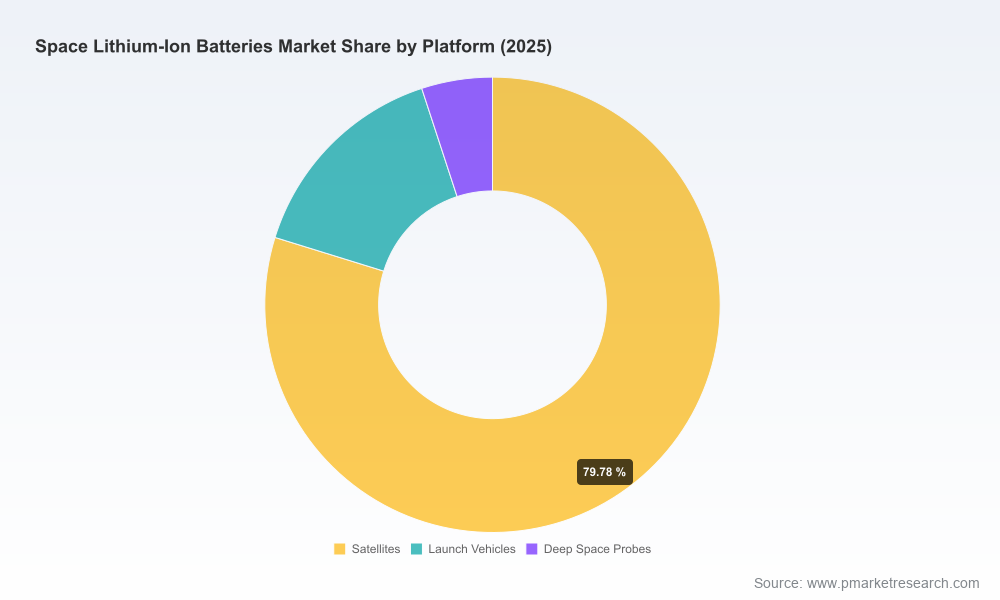

Space lithium‑ion batteries sit at the intersection of accelerating demand (satellites, launch vehicles, deep‑space probes), rapid technological progress (energy density, low‑temperature chemistries, solid‑state alternatives), and heightened geopolitical focus on critical minerals and supply chains. For executives planning 2026 capital allocation, technology partnerships, or procurement pathways, understanding the macro growth profile (14.0% CAGR on a 2026–2032 forecast base) and the market’s competitive concentration is table stakes.

Space Lithium Ion Batteries Market

- Scale and momentum: The sector’s market size in 2025 establishes a firm baseline from which the high‑teens to mid‑teens CAGR drives material demand for cells, battery management systems (BMS), and qualified integration services during the 2026–2032 window.

- Concentration and supplier power: Market concentration metrics indicate a moderately consolidated supplier landscape (CR3 and CR5 levels), implying that a small set of specialized vendors will continue to command meaningful share and influence on price, qualification cycles, and lead times.

- Policy and supply risks: Recent trade, export control, and raw material developments have amplified sourcing risk for high‑energy‑density chemistries and key cathode/anode materials. Buyers and integrators must embed policy‑risk assumptions into 2026 sourcing decisions.

What the PW Consulting report delivers (practical, procurement‑ready intelligence)

PW Consulting designed the full report to be operationally relevant for decision makers across satellite OEMs, prime integrators, defense acquisition teams, and investment committees. Highlights include:

Space Lithium Ion Batteries Market

- Market sizing and scenario forecasts (2026–2032) with transparent assumptions and sensitivity testing to alternative demand scenarios;

- Supplier assessment frameworks and scorecards that translate technical and programmatic attributes into procurement scores (qualification maturity, flight heritage, manufacturing depth, supply‑chain resilience, and cost competitiveness);

- Qualification and testing playbooks aligned to prevailing agency standards (including automated testing pathways for crewed and uncrewed missions), plus recommended timelines to de‑risk launch schedules;

- Technology roadmaps comparing incumbent Li‑ion chemistry evolutions with emergent alternatives (li‑sulfur, solid‑state, low‑temperature electrolytes), focused on TRL, on‑orbit performance, and integration constraints;

- Supply‑chain and raw‑materials risk matrices that model price volatility, export policy shocks, and reshoring options — each tied to actionable mitigation strategies such as dual‑sourcing, strategic inventory, and long‑term offtake arrangements;

- Commercial contracting templates and negotiation playbooks for multi‑year supply, qualification milestones, and warranty/flight‑failure liabilities;

- Financial modeling modules that convert battery‑subsystem choices into program‑level CAPEX/OPEX and lifecycle replacement costs, enabling board‑level tradeoffs;

- Concise executive checklists for procurement, engineering, and compliance teams to align 2026 programs with the most likely technology and policy outcomes.

Competitive landscape: who matters and why

The report’s company profiles combine heritage flight data, manufacturing footprint, and strategic posture to help buyers prioritize partners. Firms with decades of space heritage remain critical anchors in the ecosystem because they combine cell know‑how with space‑grade system integration and qualification experience. Key considerations we analyze for each supplier include manufacturing verticality, cell form‑factor specialties, flight heritage, and strategic customer relationships.

- EaglePicher Technologies LLC (United States): Renowned for large Li‑ion cell design and assembly with deep heritage powering hundreds of satellites. Their specialization in high‑energy, long‑cycle cells positions them for missions prioritizing energy density and lifecycle performance.

- Saft Groupe SA / TotalEnergies (France): A vertically integrated producer across electrodes to systems with extensive flight heritage; strong where end‑to‑end control and integrated safety electronics matter for extreme thermal and radiation environments.

- GS Yuasa Corporation (Japan): Significant on‑orbit energy deployed and recent milestone achievements that reinforce capability claims. Their cells are commonly selected by major integrators and national agencies.

- EnerSys / ABSL Space Products (United States): Pioneers in space Li‑ion deployments with a track record spanning SmallSats to flagship telescopes; their ABSL line is often favored for mixed‑mission portfolios.

- Mitsubishi Electric Corporation (Japan): Focused on spacecraft‑exclusive high‑energy‑density cells and long‑term supplier relationships with major integrators; attracts programs requiring bespoke cell performance ranges.

- Airbus (Europe): Develops module‑level offerings leveraging qualified COTS cells, delivering competitive pricing and module integration expertise for certain classes of satellites.

- Arotech, Bren‑Tronics (United States): Suppliers notable for defense and aerospace portfolios, delivering qualified solutions for mission segments where cross‑domain supplier capability is advantageous.

Recent market developments underscore the pace of change: industry milestones in on‑orbit energy deployment validate provider claims; targeted government awards accelerate low‑temperature and high‑energy-density research; demonstration selections for alternative chemistries indicate a near‑term window for technology disruption; and module qualifications by major primes signal competitive pressure on pricing and procurement models. PW Consulting maps these events into a dynamic supplier heatmap to guide 2026 partner selection.

Policy and raw‑material drivers that must shape 2026 decisions

Three structural forces will shape procurement and investment choices in 2026:

- Raw‑material price dynamics: Lithium and other critical mineral price swings materially affect cell economics. A rebound in lithium carbonate pricing in 2025 highlighted the potential for rapid cost escalation and the need for hedging strategies and long‑lead supply agreements.

- Export controls and trade policy: New controls on high‑energy‑density technologies and materials change qualification and sourcing risk profiles. Designers and procurement officers must test alternate supplier pathways and ensure export‑compliance expertise is embedded in contracts and program timelines.

- Regulatory and agency qualification regimes: NASA and other major agencies continue to raise qualification thresholds for crewed and strategic missions, driving automated testing, increased safety electronics, and longer qualification timelines — all of which affect supplier selection and schedule buffers.

How 2026 leaders should act — five practical recommendations

- Integrate policy scenarios into supply decisions: Stress‑test sourcing, especially for high‑energy chemistries, under different export‑control and tariff scenarios. Prefer flexible contracts that allow substitution under defined conditions.

- Prioritize qualification roadmaps over lowest‑price bids: A supplier’s ability to meet agency standards and compress qualification schedules often yields higher program value than marginal unit‑cost savings.

- Adopt hybrid sourcing and strategic inventory: Dual‑sourcing across heritage vendors and newer entrants, combined with targeted inventory buffers for critical cell families, reduces launch risk while preserving cost flexibility.

- Invest in near‑term demonstrations for differentiated chemistries: Allocating modest budgets to on‑orbit demonstrations of alternative chemistries or low‑temperature electrolytes can create asymmetric advantage if these technologies mature faster than the market expects.

- Embed battery economics into program lifecycle models: Use PW Consulting’s CAPEX/OPEX templates to quantify lifecycle replacement and warranty exposure, ensuring procurement and engineering tradeoffs are financially rationalized.

Concluding note — the decision horizon for 2026

For program managers, procurement leads, and corporate strategists preparing decisions in 2026, the Space Lithium‑Ion Batteries Market presents a classic high‑growth, high‑complexity opportunity: growth is predictable at the macro level, supplier concentration creates focal points for negotiation, and policy and material shocks can rapidly rewire competitive advantage. PW Consulting’s full report translates these macro realities into actionable procurement frameworks, supplier evaluations, qualification playbooks, and financial models that your organization can operationalize immediately.

To access the detailed datasets, vendor scorecards, and downloadable procurement templates referenced in this preview, please consult the full PW Consulting Space Lithium‑Ion Batteries Market report available on our website. The full research package contains the segment‑level breakdowns, model assumptions, and appendices required to implement the strategies summarized here.

For detailed analysis of this topic, please visit the official page:Space Lithium Ion Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com