Best Websites to 03 purchase Verified PayPal Accounts ...

Film |

2026-05-26 00:13:16

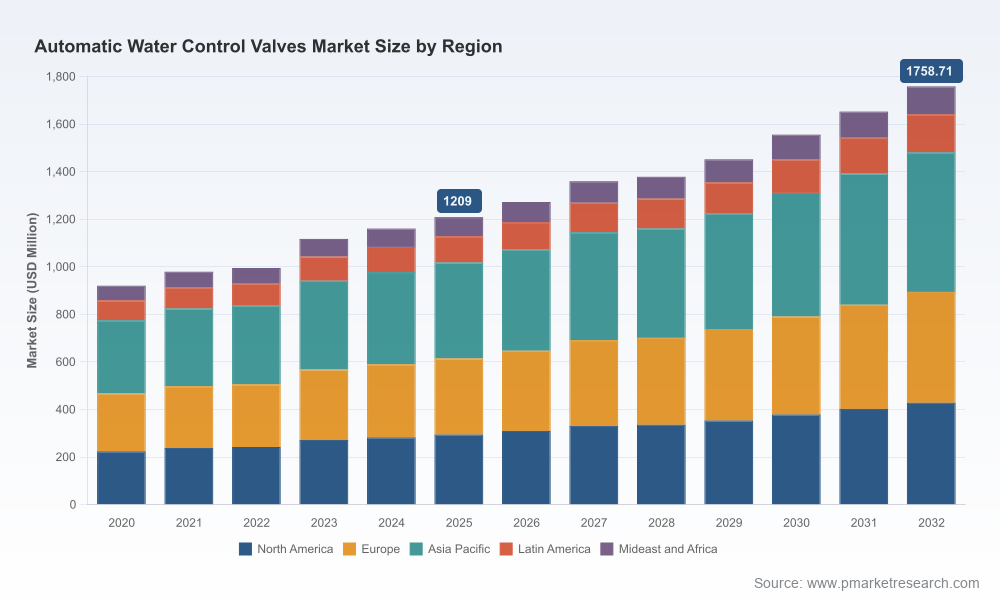

PW Consulting’s latest market intelligence brief on the Automatic Water Control Valves market provides a decision-grade, executive-level briefing designed to shape capital allocation, product strategy, procurement and M&A decisions in 2026. Anchored in a robust time series (2020–2025 base) and a seven-year outlook (2026–2032), the study shows the global market reached approximately USD 1,209.0 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 5.5% through 2032 to reach the mid‑USD 1.7 billion range. This note highlights the strategic value of the full report and outlines the specific ways it will materially affect corporate choices in the year ahead.

Automatic Water Control Valves Market

Transition from recovery to steady-state growth — after the volatility of the early 2020s, the market is entering a period characterized by predictable, mid-single-digit CAGR expansion. That shift alters prioritization from short-term revenue capture to sustainable margin expansion and selective investment in capabilities that will compound over the next investment cycle.

Automatic Water Control Valves Market

Regulatory and procurement thresholds are shifting. New compliance requirements and public procurement preferences are driving spec changes and supplier qualification processes that will materially affect near-term tender outcomes.

Automatic Water Control Valves Market

Supply-chain and raw-material dynamics are reintroducing cost volatility into historically stable product categories; buyers and manufacturers who understand the operational levers will protect margins and competitive positioning.

The report is intentionally designed for operational use by senior executives, product and procurement leaders, and investors. Highlights include:

Forward-looking market sizing and scenario models — base, upside and downside cases — enabling stress testing of revenue and return projections against 2026 capital budgets.

Demand drivers and adoption curves by end-market and application (presented in drillable models). Note: this preview intentionally refrains from publishing detailed regional or application splits — those granular tables and interactive models are available in the full report.

Unit economics and total cost of ownership (TCO) calculator templates that quantify life‑cycle service, energy and maintenance costs for electric, pneumatic and hydraulic valve platforms.

Procurement playbook and supplier evaluation framework — a checklist for AIS/BABA, NSF compliance, lead-time risk and quality assurance, structured for use in RFPs and vendor scorecards.

Risk heatmaps and mitigation strategies (supply chain, raw materials, regulatory compliance, and technology obsolescence), tied to quantified P&L impacts under our scenarios.

Competitive landscaping with strategic profiles and capability matrices for the principal OEMs and system suppliers operating globally.

Deal screening templates and synergy assessment heuristics for M&A and partnership evaluation, calibrated to the sector’s current consolidation profile.

Regulatory traction: Compliance to potable-water health standards (e.g., NSF/ANSI family) and the increasing use of Buy America / American Iron & Steel conditions in municipal projects remain a gating factor for contract award. These requirements are not binary; product certification timelines and factory audit schedules create adoption lags that materially affect supplier selection in 2026 tenders.

Standards-driven specification shifts: Industry standards such as AWWA C530 for pilot-operated control valves are actively shaping technical roadmaps and will advantage suppliers with robust test and certification pipelines.

Input cost environment: Metal valve manufacturers are operating with elevated producer-price indices relative to recent history — raw-material cost dynamics are translating into periodic price resets and OEM tiering strategies. Buyers should expect a combination of indexed pricing clauses and limited-scope hedging programs to proliferate.

The market displays moderate concentration: the top three global players account for a meaningful share of sales, and the top five approach a majority foothold. That structure creates a landscape where regional specialists and niche innovators can coexist with global incumbents by focusing on certification velocity, aftermarket services, or specialized valve technologies.

Key players reviewed in the full report include:

Cla‑Val (Costa Mesa, CA, USA) — a long-standing specialist in pilot-operated and pressure-management control valves with deep penetration in waterworks and fire protection systems.

Flomatic Valves (Glens Falls, NY, USA) — a US manufacturer noted for municipal and wastewater valves and recent product refreshes and certifications that increase its tender-readiness in AIS/BABA-sensitive projects. Notable near-term activity includes updated catalogs and AIS/BABA-compliant product introductions and NSF certifications issued in late 2025 and early 2026, accelerating procurement eligibility for US public works programs.

Singer Valve (Surrey, BC, Canada) — a specialist in pressure management, surge control and distribution automation components for municipal networks.

Watts Water Technologies (North Andover, MA, USA) — broad commercial plumbing and industrial product portfolio with capability in packaged solutions and service contracts.

Zurn (Milwaukee, WI, USA) — strong position in industrial/commercial epoxy-coated automatic valves and surge protection offerings.

BERMAD (Evron, Israel; global operations) — hydraulic valve technologies with strong presence in irrigation and building water systems and global delivery capabilities.

Each profile in the report includes capability maps, recent product and certification developments, order-book indicators, and readiness scores against municipal procurement criteria.

CEOs & CFOs: Rebalance capital deployment between aftermarket service expansion and product certification capital. The growth profile supports higher recurring‑revenue models via service contracts — an opportunity to increase valuation multiples without relying exclusively on new unit sales.

Product & Engineering Leaders: Prioritize modular architectures and certification roadmaps. Investments in design-for-certification, and in data-capture features that enable predictive maintenance, will shorten sales cycles and improve tender competitiveness.

Procurement & Operations: Adopt the report’s supplier-scorecard and TCO models to move beyond unit-price decisioning. Plan for staged qualification timelines where AIS/BABA, NSF/ANSI, and manufacturer factory audits can create multi-month gating impacts.

Private Equity & Strategic Buyers: Use the provided deal-screening templates to differentiate value accretion from mere top-line aggregation. The consolidation metric highlighted in the report demonstrates both acquisition scarcity and opportunity via bolt-on technical capabilities.

Immediate (0–90 days): Use our supplier-readiness checklist to prioritize vendors for 2026 RFPs and to identify certification gaps that could delay awards.

Near term (3–9 months): Run the TCO and scenario models against candidate investments (manufacturing automation, lab certifications, digital retrofit kits) to quantify payback under the three forecast scenarios provided.

Medium term (9–18 months): Execute on service-led value capture — retrofit programs and predictive‑maintenance offerings outlined in the report include templated commercial models and pricing heuristics.

This preview emphasizes strategic insight and actionable guidance while withholding granular regional, application and type-level splits and proprietary price tables that are central to execution planning. Those detailed segmentation models, supplier scorecards, and the interactive financial model are available in the full PW Consulting report and accompanying Excel toolkit. The full suite provides the exact data points procurement teams and M&A groups need to operationalize strategy.

Download the full report and model to access: (1) region- and application-level demand curves; (2) unit-cost and margin ladders by valve type; (3) supplier scorecards and certification calendars; and (4) client‑customizable TCO and M&A models.

Engage PW Consulting for a 90-minute executive briefing tailored to your organization’s exposure — we will run your RFP pipeline through our procurement playbook and highlight 90‑day priority actions.

With predictable mid-single-digit growth ahead, 2026 is the year for pragmatic moves that increase resilience: tighten procurement processes, accelerate certification roadmaps, and convert installed-base relationships into recurring revenue. PW Consulting’s full Automatic Water Control Valves Market report provides the granular modeling and operational tools required to translate those strategic priorities into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Automatic Water Control Valves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com