Antirusting Anti Rust Agents Market 2026: A Strategic Playbook for Decision-Makers

Executive teaser

As industrial supply chains confront tighter environmental regulation, raw-material volatility and accelerating demand for low-emissions formulations, the antirusting (anti rust) agents market is entering a phase that rewards strategic clarity and operational agility. PW Consulting’s new market research brief synthesizes a seven-year historical run and a seven-year forecast to deliver a practical decision toolkit for corporate leaders preparing budgets and capital plans for 2026 and beyond. The brief intentionally showcases macro trends, competitive dynamics and actionable scenarios while reserving detailed segment-level tables and exact regional/application splits for the full report—designed to drive targeted follow-up and bespoke advisory engagements.

Antirusting Anti Rust Agents Market

Market snapshot: Where the market stands and where it’s headed

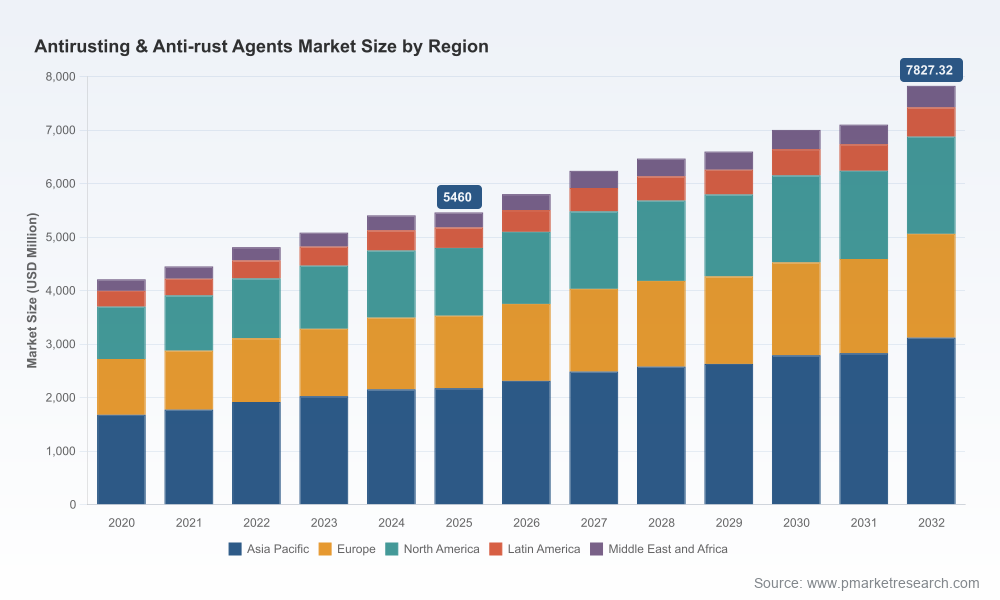

The antirusting agents market has demonstrated steady expansion over the past half decade. Our consolidated series places the market at approximately 5,460 Million USD in 2025, up from roughly 4,210.5 Million USD in 2020, reflecting persistent industrial demand and incremental product upgrading. PW Consulting’s modeling projects continued growth through the forecast window, rising to an estimated 7,827.32 Million USD by 2032—a compound annual growth rate of 5.28% between 2026 and 2032. The 2026 inflection point matters: early adopters of low-VOC water-based chemistries, vapor-phase inhibitors, and supply-chain resilience measures are positioned to capture outsized share as regulations and customer preferences converge.

Antirusting Anti Rust Agents Market

Why this matters for 2026 corporate planning

- Capital allocation: Companies deciding between brownfield upgrades (retrofit corrosion-control processes) and greenfield investments must weigh modest but steady market expansion against tightening regulatory risk—our scenario models quantify mid- and high-regulation outcomes to inform 3–5 year ROI horizons.

- R&D prioritization: Formulation roadmaps that shift toward water-based systems, silane-based coupling agents and non-fluorinated alternatives can mitigate regulatory exposure while addressing customer demand for lower environmental impact products. The report maps technical trade-offs and time-to-market for prioritized chemistries.

- Sourcing and procurement: Raw-material cost pressure—most notably from petroleum-linked feedstocks and amine intermediates—requires structured hedging and supplier diversification. Our price-sensitivity matrices and supplier-ranking templates allow procurement to set defensible threshold prices for contract negotiations in 2026.

- M&A and partnership targeting: A moderately fragmented market structure (top-three companies account for less than a third of market revenue, with top-five under 40%) signals acquisition opportunities among specialty mid-market players and bolt-on technology providers. We identify archetypal targets and synergy levers for strategic buyers.

Key dynamics reshaping the market

- Regulatory tightening and disclosure: Global regulatory movements—from restrictions on phosphate-containing additives in the EU to expanded PFAS reporting obligations in the U.S.—are pushing formulators to reassess chemistries and compliance costs. The regulatory scenario suite in the report isolates commercial impact pathways for 2026 procurement and product lines.

- Raw-material volatility: Petroleum price oscillations and upstream chemical input cost moves materially affect oil-soluble inhibitor economics. For example, Brent crude averaged a level in 2024 that elevated pricing pressure on petroleum-derived sulfonates, while spot triethanolamine prices rose meaningfully toward year-end—events we model to show their pass-through to end-customer pricing.

- Product innovation: Two distinct innovation tracks are converging—improved water-based rust preventives and vapor-phase corrosion inhibitors (VCI) for packaging and storage. These are complemented by silane and pre-treatment chemistries that integrate with coating systems. Our technical-readiness maps score these tracks by cost, scalability and regulatory resilience.

- Trade and tariff exposure: Targeted duties on specific organic chemicals used in formulations elevate the strategic importance of regional sourcing and near-shoring decisions. The full report layers tariff scenarios with supplier-risk ratings to help procurement teams prioritize contingencies.

What the PW Consulting report delivers (practical, implementable tools)

Beyond a narrative, this brief is a toolkit for 2026 operational and strategic choices:

Antirusting Anti Rust Agents Market

- Market model suite: a transparent, auditable model that rolls up historicals and forecasts to support sensitivity testing on price, volume and regulatory shock scenarios.

- Competitive playbooks: granular profiles of incumbent and challenger firms, capability matrices and product-to-application mapping to support go-to-market planning and alliance targeting.

- Regulatory impact matrix: side-by-side cost and timeline implications of major regulatory events (e.g., EU substance restrictions, U.S. PFAS disclosure rules), with prioritized mitigation options.

- Procurement scorecard and hedging templates: supplier evaluation criteria, contractual language recommendations, and short-to-medium term hedging tactics for common feedstocks.

- R&D decision framework: prioritization engine that balances reformulation costs, performance trade-offs and customer preference trajectories to recommend 9–18 month development tracks.

- M&A screening and valuation heuristics: a shortlist of value creation levers (product consolidation, channel integration, geographic adjuncts) together with quick-screen valuation multiples that reflect market fragmentation and technology intensity.

Competitive landscape — core players and strategic implications

The market exhibits a balance of global materials giants and specialized technology providers. Leading chemical and coatings companies remain influential across value chains, while niche innovators advance VCI, silane-based inhibitors and water-based formulations. Notable participants covered in the report include BASF SE (industrial corrosion chemistries), Henkel (manufacturing rust-preventive portfolios), Akzo Nobel (coatings and marine primers), Lubrizol (metalworking fluid additives), Clariant (synthetic rust preventives), Cortec Corporation (VpCI technologies), Quaker Houghton (process-integrated preventives), McGean, Daubert Chemical, Petrofer, Evonik and Lanxess.

Our competitive analysis highlights three actionable takeaways for 2026:

- Scale players continue to compete on integrated solutions and global distribution; partnerships or licensing can accelerate product rollouts for mid-sized formulators.

- Niche specialists focused on packaging VCIs, silane pretreatments or biodegradable preventives are attractive targets for partnerships or acquisitions given their IP and defensible margins.

- Recent commercial moves—such as portfolio extensions into low-VOC formulations and launches of water-compatible VpCI products—indicate that innovation is migrating toward regulatory-compliant, lower-emissions chemistries. Corporates should assess both defensive reformulation and offensive product development strategies.

Regulatory and supply-risk playbook for buyers and producers

In 2026, successful players will combine proactive compliance with supply-chain resilience:

- Establish a regulatory horizon-scanning function to feed engineering and procurement cycles; embed reporting-readiness for substances subject to new disclosure rules.

- Execute dual-sourcing for critical amine and petroleum-derivative inputs and build optionality into formulation designs to substitute constrained feedstocks without requalifying entire product platforms.

- Adopt staged reformulation: prioritize high-exposure SKUs for substitution while staging investments in broader product suites to preserve margin and customer relationships.

Strategic recommendations for 2026 planning

- Reformulate with intent: Prioritize low-VOC and non-fluorinated alternatives where customer end-markets or regional regulators signal enforcement. Use our decision matrix to map product-level commercial impact.

- Targeted M&A: Pursue bolt-ons that provide immediate tech differentiation (VCI, silane coupling, biodegradable additives) rather than scale-only acquisitions, given the market’s moderate concentration profile.

- Operational hedging: Insulate gross margins with a combination of forward purchasing for volatile feedstocks and index-linked pricing mechanisms for long-term contracts.

- Commercial repositioning: Re-sell technical value (storage lifespan, environmental compliance, ease-of-use) to capture higher margin tiers in automotive, aerospace and high-value manufacturing segments.

How PW Consulting supports execution

Our advisory offering ties the market intelligence pack to executable initiatives: bespoke opportunity screens, integration playbooks for M&A targets, pilot-plant design support for reformulation, and procurement transformation programs focused on supplier segmentation and risk mitigation. For teams that prefer rapid external validation, we provide a condensed strategic briefing tailored to specific corporate objectives—delivering prioritized actions for 90-, 180- and 360-day timelines.

Closing and next steps

The antirusting agents market is not a binary bet on growth; it is a multidimensional set of choices that combine chemical science, regulatory real-time monitoring and supply-chain sophistication. PW Consulting’s report equips leaders with the macro view—including a clear trajectory from a 2025 market base of approximately 5.46 billion USD to a projected near-7.83 billion USD by 2032, and a modeled growth rate of 5.28%—while providing the decision frameworks needed to translate insight into action in 2026.

For the full set of segmented data, proprietary scenario outputs, supplier scorecards and the complete list of company profiles and recent transactional intelligence, visit the report landing page. Our public brief intentionally omits granular regional and application-level splits to protect the proprietary models that deliver the greatest strategic advantage; these are available in full through the PW Consulting report and advisory engagements.

For detailed analysis of this topic, please visit the official page:Antirusting Anti Rust Agents Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com