The Rise of Sustainable Practices in the Bottle Filling Machine Market

Other |

2026-05-25 13:19:33

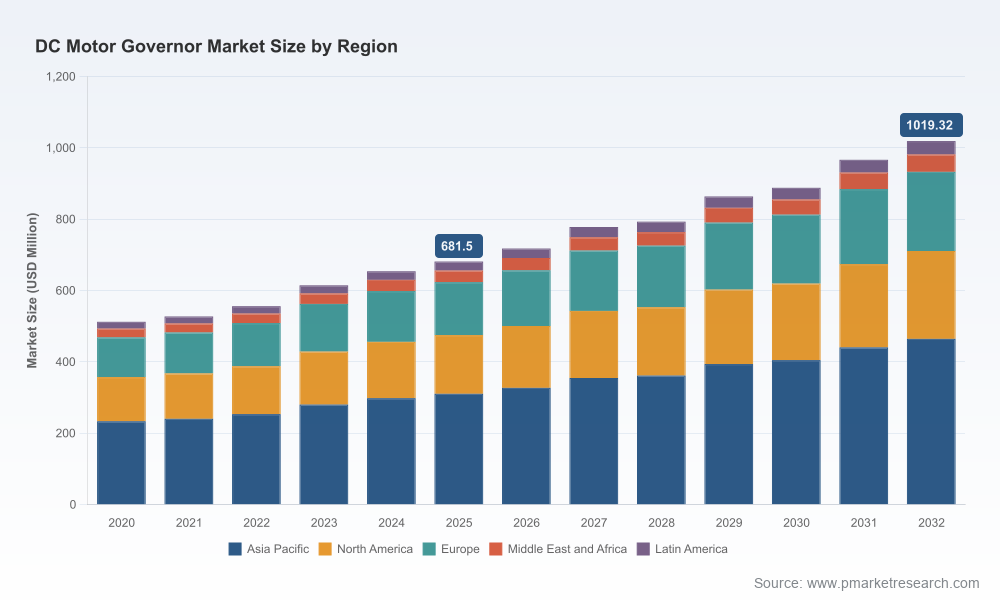

As capital allocation cycles reset and equipment roadmaps are rewritten in 2026, decision-makers in industrial OEMs, automation integrators, and power-electronics suppliers need an actionable, risk-calibrated view of the Dc motor governor market. PW Consulting’s latest market research synthesizes five years of historical dynamics with a seven-year forecast horizon to deliver precisely that. Our analysis shows a market that expanded steadily from the early 2020s and reached USD 681.5 million in 2025. Driven by ongoing industrial automation projects, energy-efficiency mandates, and selective product modernization, the market is projected to grow at a compound annual growth rate (CAGR) of 5.92% over the 2026–2032 forecast period, reaching roughly USD 1,019.3 million by 2032.

Dc Motor Governor Market

Investment prioritization: The projected mid-single-digit CAGR indicates sustained demand but not runaway expansion—companies must distinguish opportunities that drive margin expansion (e.g., intelligent governors and service models) from volume-based, low-margin acts.

Dc Motor Governor Market

Portfolio rationalization: Legacy power-electronics platforms remain important in heavy industry, but digital and integrated governor solutions are gaining strategic value for lifecycle services and energy optimization.

Dc Motor Governor Market

Supply chain resilience: Component-level pressures—most notably semiconductors and power-stage discrete components—will influence time-to-market and BOM economics throughout 2026.

Regulatory compliance and product positioning: Updated efficiency standards for small electric motors (notably recent U.S. Department of Energy changes) create near-term compliance requirements and medium-term demand for governors that can demonstrate measurable energy savings.

The market has shown consistent expansion from 2020 through 2025, reflecting a mix of retrofit activity and steady OEM demand. We quantify a clear path from a constrained post-pandemic recovery toward a structurally larger market by the end of the forecast horizon. The market concentration metrics underscore the competitive landscape: the top three players account for under one-fifth of global revenues (CR3 ~18.4%), and the top five remain modestly concentrated (CR5 ~25.8%). In practical terms, this is a fragmented market with localized leadership, leaving room for regional champions, technology specialists, and service-led scale plays.

PW Consulting’s report is designed as an operational toolkit for executives and strategists. Highlights include:

Granular market model: A bottom-up sizing and forecasting engine by year (historical 2020–2025, forecast 2026–2032) calibrated to primary interviews and supply-side data.

Technology and product taxonomies: Clear definitions and adoption timelines for pulse width modulation (PWM), silicon controlled rectifier (SCR), and digital intelligent governors—mapped to typical use cases and upgrade cycles.

Commercial playbooks: Channel and OEM GTM strategies, value-based pricing frameworks, and service-bundling templates tailored to tier and geography.

Supplier and component risk matrix: Probabilistic scenarios for semiconductor availability, power-stage supply, and commodity price volatility with mitigation playbooks.

Regulatory impact analysis: Practical steps for product compliance, test-plan implications, and cost-to-certify estimates under the latest energy-efficiency rules.

Competitive benchmarking and M&A radar: Profiles, capability maps, and shortlists of potential targets based on technology, channel access, and margin profiles.

Our desk and primary research focused on a cross-section of established multinationals, specialist drive-makers, and regional manufacturers. Key takeaways for 2026:

ABB (Zurich) continues to leverage its industrial-drive portfolio, emphasizing high-capacity field-supplied drives suitable for heavy-industry governors; recent product availability notes highlight enhanced field-supply options designed for high-current applications—an important factor for large-motor retrofit projects.

Sprint Electric (UK) is doubling down on simplicity and installation efficiency for its PL/X series; its visible presence at regional trade events signals a go-to-market strategy aimed at maintenance-led upgrades and machine builders seeking low-friction replacements.

American Control Electronics / Minarik Drives (USA) remains a supplier of choice for automation-focused applications in North America, with a broad portfolio that supports OEMs and aftermarket channels.

Parker Hannifin’s DC drive lineage (including SSD/Eurotherm heritage) positions it as a systems-level supplier for integrators seeking not just drives but process control and life-cycle support.

Chinese manufacturers such as DZ Gear Motors and C-lin are increasingly competitive on cost and localized service—important variables for regional OEMs and price-sensitive aftermarket volume.

Collectively, these players illustrate a market where product differentiation—through installation simplicity, service capability, and energy-saving credentials—drives competitive advantage more reliably than scale alone.

Regulation: The recent DOE standard updates sharpen the commercial case for governors that can demonstrably reduce motor-system energy consumption. Compliance timelines create both retrofit demand and near-term product development pressures.

Technology substitution: Digital intelligent governors capture value through analytics, remote diagnostics, and predictive maintenance; however, adoption remains phased, as retrofit cycles and CAPEX constraints slow enterprise-wide rollouts.

Component supply and input prices: Semiconductor tightness and shifting electronics manufacturing footprints will create staggered delivery risks and periodic margin compression unless firms implement hedging, dual-sourcing, or design-for-alternative-component strategies.

Market fragmentation: The modest concentration ratios mean consolidation opportunities exist, but acquirers must be selective—technology fit and service footprint matter more than headline revenue.

Based on our scenario analysis, PW Consulting recommends a set of priority actions for executives crafting 2026 roadmaps:

Prioritize modular, software-enabled governors for new product programs. These deliver higher-margin software subscriptions and enable energy-savings proofs that ease procurement approvals.

Accelerate retrofit propositions in regions and industry verticals where horsepower-heavy equipment and energy-efficiency mandates intersect—packaged retrofit kits plus local installation services shorten sales cycles.

Fortify procurement and supply-chain strategies focused on semiconductor alternatives, long-lead components, and second-source qualification to reduce time-to-market variability.

Use targeted M&A to acquire complementary digital control capabilities or regional service networks rather than broad revenue consolidation—aim for tactical tuck-ins that improve margin or distribution reach.

Invest in certification and test labs now to reduce product-to-market delays associated with new efficiency standards; early compliance also creates a shelf-advantage in tender processes.

Executive teams and business units can integrate our findings into 90–180-day planning cycles by:

Plugging our market model into your revenue planning to stress-test product launches and aftermarket service scenarios against the quantified CAGR and scenario outcomes.

Using the supplier risk matrix to inform tier-1 and tier-2 sourcing strategies, and to quantify potential margin impacts from supply shocks.

Adopting the go-to-market playbooks for trial programs and pilot deployments—especially where digital governors can be sold as proof-of-value with short payback claims.

Referencing the competitive bench to prioritize surveillance and opportunistic partnership conversations with regional champions and technology specialists.

This briefing intentionally highlights the strategy-significant findings while preserving the full depth of our segmentation matrices, primary interview transcripts, and downloadable modeling workbooks for subscribers. The complete report contains the granular regional, technology, and application splits, as well as Excel-based scenario models you can adapt to your product or geographic play. For teams preparing capital plans, product roadmaps, or M&A screeners for 2026, the full dataset and consulting appendices will materially shorten decision cycles and reduce execution risk.

Dc motor governors are at an inflection point: stable demand growth paired with technological and regulatory infusions that reward companies able to convert control hardware into measurable energy and uptime outcomes. PW Consulting’s research reframes the market from a collection of component sales into a services-augmentable, software-empowered ecosystem. For 2026 strategy cycles, that reframing is the difference between incremental performance and step-change commercial outcomes.

For detailed analysis of this topic, please visit the official page:Dc Motor Governor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com