How Self-Sovereign Identity Supports Regulatory Compliance

Other |

2026-02-03 07:12:34

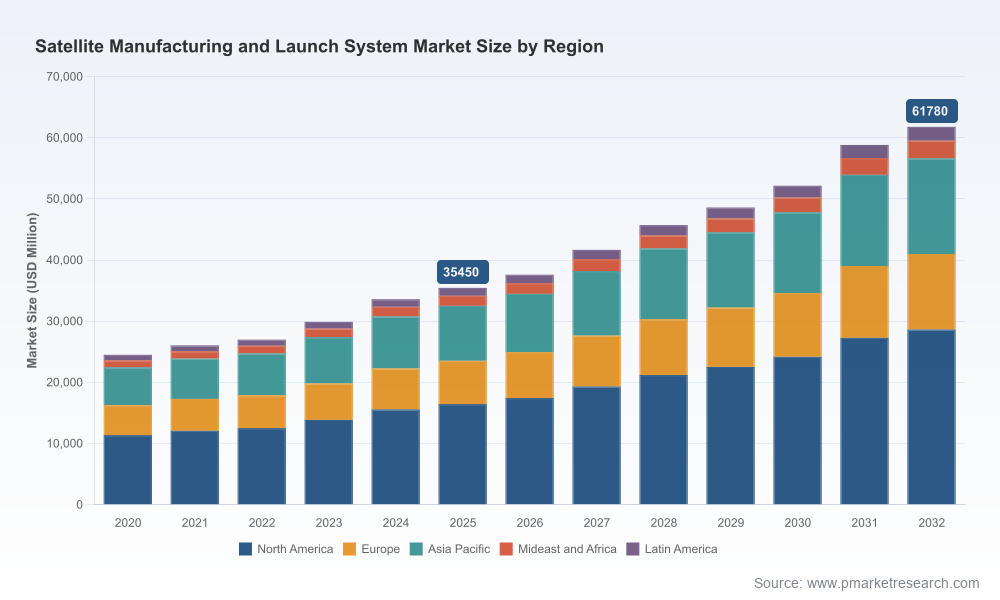

As nations, commercial operators, and new-space entrants accelerate constellation deployments, the Satellite Manufacturing and Launch System market is entering a decisive multi-year growth phase. Our new market study — anchored on a 2025 base year, covering historical performance (2020–2025) and projecting through 2026–2032 — quantifies a robust trajectory driven by commoditization of smallsat manufacturing, increasingly frequent launch cadences, and renewed investment in medium- and heavy-lift capacity. The market is forecast to expand at a compound annual growth rate of approximately 8.26% over the forecast window. By framing the magnitude of opportunity and the structural competitive forces at work, this report is intended as an operational playbook for boards, corporate strategy teams, investors, and government planners preparing decisions in 2026 and beyond.

Satellite Manufacturing And Launch System Market

Timing matters: 2026 is the inflection point for many commercialization plans — from follow-on constellation tranches to inertia-breaking government procurements. Decisions made now about factory capacity, launch procurement, or vertical integration will materially determine unit economics over the next contract cycle.

Satellite Manufacturing And Launch System Market

Capital allocation choices must reflect durable demand: with overall market scale having more than doubled from the start of the decade and a projection of continued expansion through 2032, organizations must move beyond short-term project bidding and adopt portfolio-level investment frameworks.

Satellite Manufacturing And Launch System Market

Competitive concentration is meaningful: market-share measures show that a small set of vertically integrated and legacy players control a large share of supply and launch logistics. That concentration creates both barriers and acquisition opportunities; discerning which route to take is a 2026 strategic imperative.

Our objective was to produce an immediately actionable document for executives making capital, M&A, and operational decisions next year. Highlights include:

Forward-looking financial model: an integrated revenue and cost model calibrated to industry KPIs, sensitivities around launch cadence, unit cost improvements from manufacturing automation, and alternate fuel/propulsion adoption curves.

Scenario-based demand forecasts: three demand paths tied to constellation refresh rates, government procurement cycles, and high-throughput broadband deployments, enabling risk-adjusted valuation of new projects.

Manufacturing playbook: blueprints for factory scaling, cleanroom throughput optimization, automation ROI thresholds, and transfer-of-technology checklists for rapid capacity expansions.

Launch procurement framework: decision matrices to evaluate fixed-price vs. manifest-based launch deals, trade-offs between ride-share and dedicated launches, and contingency hedging strategies.

Supply-chain risk map: supplier concentration heatmaps, critical materials exposure (including semiconductor-grade and specialty compound inputs), and mitigation options ranging from dual-sourcing to inventory financing.

M&A and partnership pipeline: a curated list of target archetypes, entry valuations, and integration playbooks specific to satellite subsystems, in-orbit services, and launch support businesses.

Regulatory and compliance annex: practical checklists for spectrum coordination, debris mitigation compliance, and export-control pathways, aligned to the latest rule updates through 2025.

The competitive map is a mix of high-volume new entrants, legacy primes, national agencies, and specialized manufacturers. The report provides line-of-sight into each profile's strategic levers — manufacturing scale, launch queuing, government relationships, and vertical scope — enabling executives to model competitive moves. Notable industry positions include:

SpaceX — a high-volume manufacturer and launch integrator whose production and ride-provisioning capabilities have reset pricing and cadence expectations; its integrated offering remains the benchmark against which industrial-scale constellations are evaluated.

Boeing — a legacy prime with strengths in geostationary platforms and defense-oriented payloads; proven systems-integration capabilities make it a partner of choice for complex, mission-critical programs.

Lockheed Martin — deep experience in military and positioning constellations, leveraging long-term government relationships and systems engineering to capture higher-margin, mission-assured business.

Northrop Grumman — strong in spacecraft buses and medium-class payloads, with dedicated small-launch options that support rapid tasking for DoD and commercial customers.

Airbus Defence and Space and Thales Alenia Space — European heavyweights emphasizing telecom platforms and partnership-led launch access; they are central nodes in cross-border industrial cooperation.

Blue Origin — focused on medium/heavy-lift capability and industrializing production of large launch vehicles; investments in 2025 accelerate its readiness posture for 2026–2027 market entry.

Rocket Lab — a specialist in smallsat manufacturing and high-frequency launch services, pushing the envelope on rapid deployment and hosted in-orbit manufacturing demonstrations.

United Launch Alliance (ULA) and Arianespace — reliable launch providers with strong GTO and government mission records, acting as backbone suppliers for time-sensitive and assured-access missions.

Maxar, Ball Aerospace, OHB, SSTL, ISRO, and CASC — each occupies a niche from high-resolution imaging to low-cost government launches, representing acquisition targets or strategic partners depending on corporate ambition.

Recent operational events through 2025 — increased Starlink deployments, smallsat manufacturing demonstrations, Ariane 6 flights, and capital injections into heavy-lift programs — are reshaping manifest competition and delivery timelines. Our analysis translates these signals into competitive scenarios that matter to negotiators and planners in 2026.

Spectrum and orbital policy: regulatory changes introduced through 2024–2025 increase planning complexity for LEO mega-constellations, with new requirements for interference mitigation and debris mitigation timelines. These create program design constraints that can materially affect launch scheduling and product lifecycles.

Export controls: export-control regimes remain a gating factor for cross-border component sourcing and platform exports. Our compliance playbook maps practical licensing pathways and risk thresholds for procurement teams.

Critical materials: supply restrictions on specialty materials used in solar cells and infrared detectors have concentrated risk in certain supply chains. The report identifies which subsystems are most exposed and provides hedging and substitution playbooks.

Manufacturing infrastructure: global cleanroom capacity suitable for satellite assembly is limited to a relatively small number of major sites. For firms needing rapid scale, options include greenfield construction, co-location agreements, or contract manufacturing partnerships — each with distinct cost and time trade-offs.

Below are prioritized moves we advise senior teams to consider as part of their 2026 strategic planning cycle. Each recommendation is supported in the full report by quantitative thresholds and implementation roadmaps.

Lock down launch capacity early. Use blended procurement (firm manifests + options) to balance price and schedule certainty; prioritize providers with demonstrated cadence or secured production funding.

Prioritize modular manufacturing investments that reduce unit cycle time. Investments in automation pay back rapidly when amortized over multi-year production runs; build-to-print suppliers can bridge short-term gaps but raise long-term cost exposure.

Establish strategic raw-material relationships. For critical compounds with constrained supply, combination approaches — direct supply agreements, stockpiling, and substitution programs — are necessary to safeguard manufacturing continuity.

Adopt a portfolio approach to revenue streams. Combine commercial constellations, government contracts, and in-orbit services to smooth revenue volatility; the report includes revenue-mix optimization tools calibrated to risk appetite.

Evaluate targeted M&A and JV opportunities where rapid capability acquisition is cheaper than organic build — especially in optics, propulsion, and on-orbit servicing segments.

Develop regulatory engagement strategies. Early engagement with spectrum and licensing authorities reduces time-to-orbit risk and unlocks favorable coordination outcomes.

The market shows a meaningful tilt toward a few large-cap providers: three firms account for a substantial portion of supply-chain value, and the top five firms together command a controlling share. This concentration raises both strategic risks (supply lock-in, pricing pressure) and opportunities (consolidation, bespoke partnership advantages) — all explored with deal-level case studies in the report.

Download the full data pack to run sensitivity analyses on your specific program assumptions; the pack includes customizable P&L templates and launch manifest simulators.

Commission a 48-hour advisory sprint with PW Consulting to stress-test your 2026 capital plan against the scenarios in the report; we provide prioritized intervention roadmaps for each scenario.

Use our supplier heatmap and M&A shortlist to build a 12–24 month procurement and investment pipeline that preserves optionality while ensuring mission assurance.

We prepared this study to be more than an academic exercise: it is a decision-useful tool for executives who must choose where to commit capital and which partnerships to form as the market scales into the next decade. With a clear growth trajectory, concentrated competitive dynamics, and non-trivial execution risks from policy and materials, 2026 will reward leaders who combine analytical rigor with decisive operational moves. For complete datasets, granular segmentation, and the interactive forecast model, access the full PW Consulting report and data pack on our publication page — the detailed intelligence you need to support 2026 board-level decisions is contained there.

For detailed analysis of this topic, please visit the official page:Satellite Manufacturing And Launch System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com