Asia-Pacific Automotive Soft Trim Interior Materials Market Competitive Landscape, Growth Analysis & Forecast

Other |

2026-05-29 07:14:40

PW Consulting’s latest market study on Fully Wrapped Carbon Fiber Composite Cylinders delivers a concentrated, decision-ready intelligence product for corporate leaders planning capital allocation, product development, and market-entry strategies in 2026. The global market has evolved from a niche engineering solution into a high-growth industrial ecosystem: total industry revenues expanded markedly over the 2020–2025 period and, under our base assumptions, the market is projected to continue a robust expansion through 2032 at a compounded annual growth rate (CAGR) of approximately 12.45% for the 2026–2032 forecast window. By way of scale, the market crosses important revenue thresholds in the mid-2020s and is modeled to approach nearly one billion USD (in millions) by the end of the forecast horizon — a signal that strategic moves made in 2026 will compound in value.

Fully Wrapped Carbon Fiber Composite Cylinders Market

Timing of investment: The sector is past early-adopter dynamics and entering a commercialization and scale phase. Manufacturers, Tier-1 gas system integrators, and industrial gas purchasers need to align investment timing with capacity ramp and certification cycles to avoid either stranded capacity or missed order books.

Fully Wrapped Carbon Fiber Composite Cylinders Market

Technology and product roadmap alignment: Advanced filament-winding processes, liner materials (notably HDPE for Type IV solutions), and automated QA are the differentiators shaping cost-to-weight and certification timelines. Our analysis identifies which manufacturing and material choices matter most to 2026 product positioning.

Fully Wrapped Carbon Fiber Composite Cylinders Market

Regulatory inflection points: Certification wins and approvals are gating factors for market access. Recent regulatory milestones have accelerated adoption in select use-cases; companies that map certification pipelines into their 2026 roadmaps will capture first-mover operational advantages.

Supply-chain risk management: Carbon fiber feedstock, resin systems, and polymer liners create distinct sourcing and logistics risk profiles — actionable mitigation strategies in the report are tailored to procurement cycles and contractual structures common in this market.

Between 2020 and 2025 the fully wrapped carbon fiber composite cylinder market demonstrated strong expansion, reflecting growing adoption across alternative fuel, industrial gas, and safety applications. Our topline model forecasts continuation of this trend into 2032, with an average growth rate of about 12.45% in the 2026–2032 period. That trajectory translates into meaningful scale for OEMs, composite producers, and system integrators: investment decisions made in 2026 regarding manufacturing footprint or strategic partnerships will see multi-year payback horizons informed by this sustained growth.

Importantly, the market concentration metrics indicate a moderately consolidated landscape. The three largest firms account for a significant share of market revenues, and the top five improve that concentration further. This structure creates a dual dynamic for challengers and incumbents alike: incumbents can exploit scale to lower unit costs and accelerate certifications, while focused challengers can win niche segments with differentiated technology, regional access, or faster time-to-certification.

Regulatory and certification momentum: Approvals and governmental safety clearances remain prerequisites for large-scale commercial offtake, particularly in hydrogen and commercial aerospace use-cases. Recent approvals and public filings show active certification programs are rewarding early movers; 2026 will be a decisive year for those who need Type IV and Type 3 certifications to enter new verticals.

Material engineering is a competitive lever: Type IV architectures employing HDPE liners wrapped with aerospace-grade carbon fiber offer substantial weight reductions versus metal cylinders — technical metrics published by leading producers indicate up to 60–70% weight savings compared to steel equivalents. That performance delta is driving uptake in weight-sensitive applications like transportation and airborne systems.

Commercialization pathways differ by application: Hydrogen transport & storage, compressed natural gas (CNG) fleets, and specialized breathing apparatuses each exhibit distinct maturity curves and procurement behaviors. Buyers in each vertical prioritize different trade-offs — cost-per-kg stored, lifecycle maintenance, and certification history — which should inform product and go-to-market segmentation.

Supply chain and localization: Recent order announcements and production expansions underscore a move toward localized manufacturing to meet regulatory and logistical requirements. Strategic investors should evaluate regional partners and consider co-investment to accelerate market entry while hedging currency and tariff exposures.

The market features a mix of global incumbents and specialized regional players. Key firms profiled in our work include Luxfer Gas Cylinders, Hexagon Composites, Faber Industrie, Time Technoplast, Carbon Cylinder Srl, and AMS Composites. These companies exemplify the strategic archetypes in the space: global-scale integrators, regional champions pursuing local approvals, and specialist niche suppliers optimizing filament-winding and liner integration.

Hexagon Composites (Ålesund, Norway) — A global leader in Type 4 high-pressure cylinders, notable for scale and extensive production of fully wrapped solutions. Recent milestone deliveries and inaugural aerospace orders reflect a capability to convert R&D into volume business and to cross-apply products into adjacent high-value segments.

Luxfer Gas Cylinders (Riverside, California, USA) — Known for Type 3 carbon composite solutions, focusing on aerospace-grade carbon fiber and alternative fuel storage applications. Their product engineering approach highlights materials and liner integration as differentiators.

Faber Industrie S.p.A. and Carbon Cylinder Srl (Italy) — European specialist manufacturers with diversified Type 2–4 portfolios and a strong emphasis on design-for-certification and EU market access.

Time Technoplast Ltd (Mumbai, India) — Illustrative of the regional champion model. Strong regulatory momentum (including recent PESO approvals) and large-scale supply contracts position it as a key supplier for regional gas-distribution projects.

AMS Composites (Taiwan) — A design-led player focusing on lightweight filament-wound cylinders for medical and specialty gas markets, representing the high-margin, low-volume end of the value chain.

Collectively, recent corporate developments — milestone deliveries, large order wins, and certification announcements — demonstrate concurrent moves to scale production and broaden addressable markets. Our competitive playbook in the report maps those moves to value-creation opportunities and defensive countermeasures.

Executive market model and scenario analysis: Topline historicals, our 2026 base case, and two stress scenarios to help shape capital planning under different demand and certification timelines.

Go-to-market blueprints: Channel strategies by end-use vertical, pricing and total-cost-of-ownership frameworks for fleet buyers, and partnership templates for OEMs seeking to secure supply.

Technology and manufacturing playbook: Process optimization roadmaps for filament winding, QC regimes for liner bonding, and automation investment profiles keyed to throughput thresholds.

Regulatory navigator: Roadmaps for major certification pathways, key tests to prioritize, and a matrix of regulatory dependencies by end market.

Supply-chain resilience strategies: Sourcing scorecards for carbon fiber and HDPE liners, inventory sizing recommendations, and contractual constructs to mitigate raw-material price volatility.

Competitive risk assessment: Profiles of the leading incumbents, entry barriers for challengers, and M&A archetypes that could alter concentration dynamics.

Investment and partnership decision framework: Prioritization criteria and KPI templates for evaluating greenfield plants, joint ventures, and technology licensing deals.

Prioritize certification-linked investments: Allocate capital to projects that align with immediate certification windows; these unlock market access and facilitate volume growth faster than general capacity expansions.

Secure critical inputs through diversified contracts: Lock in carbon fiber and liner supply via multi-supplier agreements and strategic inventory to dampen raw-material exposure during rapid demand ramps.

Adopt modular manufacturing design: Flexible cell-based production allows producers to shift outputs between Type 3 and Type 4 architectures as market demand evolves.

Form regional partnerships: For companies without local certifications or regulatory familiarity, consider manufacturing partnerships or licensed manufacturing to accelerate market entry while complying with local standards.

Invest in safety and lifecycle analytics: Differentiation will come from demonstrated lifecycle performance and digital provenance of each cylinder — consider embedding sensors and establishing data-backed maintenance services.

This PW Consulting brief is designed as a decision-support layer for boards, corporate strategy teams, and investors. Use the report to validate capex timing, evaluate partner ecosystems, and stress-test product roadmaps under alternate certification timelines. Our models and frameworks tie forecasted market scale to tactical moves that can be executed inside a 12–24 month planning horizon.

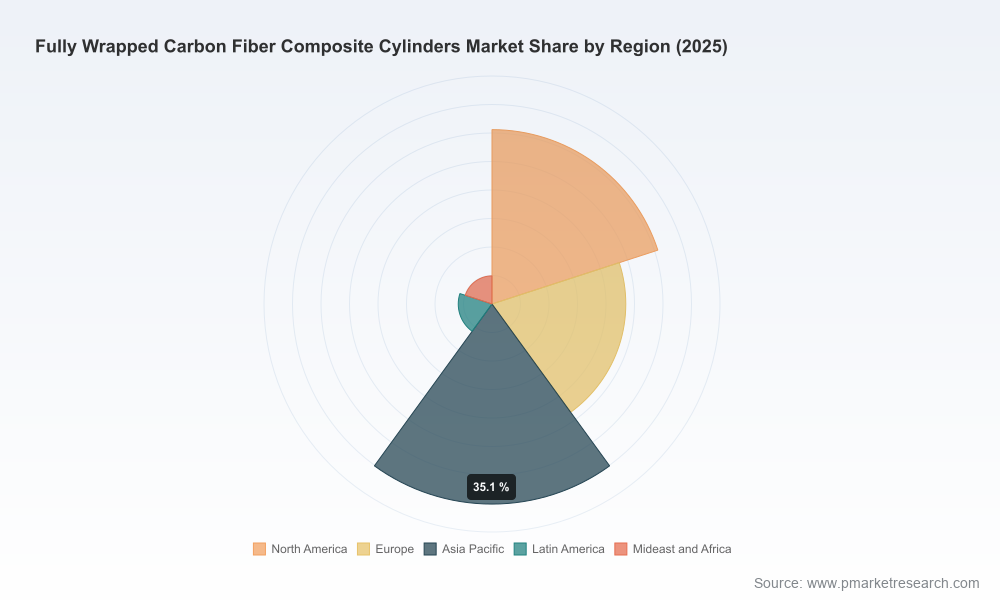

For teams requiring forward-looking, executable intelligence — including the detailed regional, type, and application splits that inform segmentation decisions — please consult the full market report. The extended dataset and proprietary segmentation models are intentionally gated to preserve competitive value while enabling clients to operationalize these insights.

PW Consulting remains available for bespoke workshops to translate the report’s findings into 2026 operating plans, supply-chain redesigns, and M&A screening criteria.

For detailed analysis of this topic, please visit the official page:Fully Wrapped Carbon Fiber Composite Cylinders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com