Gas Pressure Regulators for Oil & Gas Market — Strategic Preview for 2026 Decision-Makers

PW Consulting’s latest market research on gas pressure regulators for the oil & gas industry offers a concise, action-oriented briefing designed to arm executives, procurement leads, and product strategists with the signals they need to set course in 2026. This preview highlights the strategic implications of our analysis without disclosing the granular segment tables reserved for the full report.

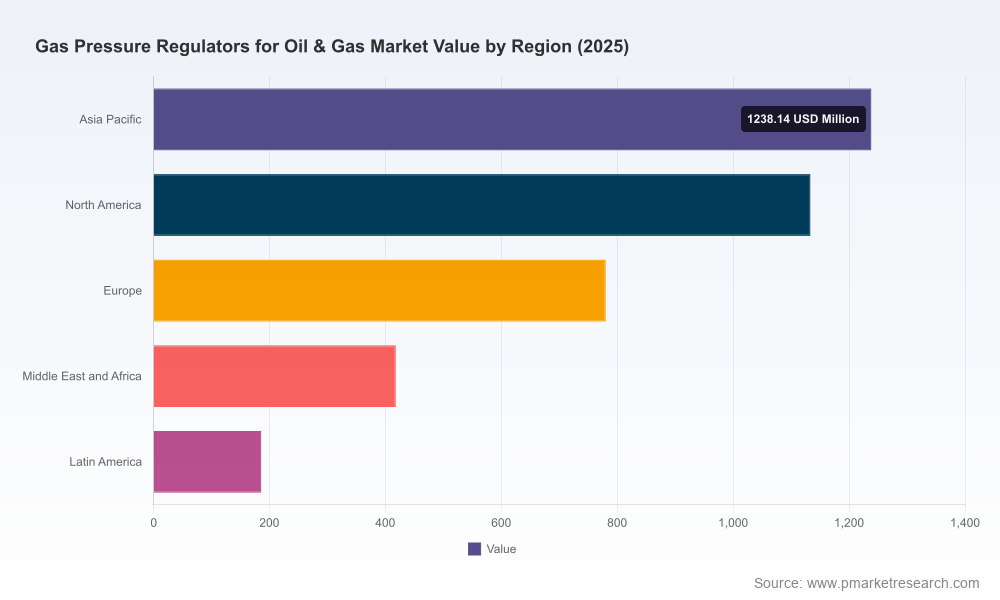

Gas Pressure Regulators For Oil Gas Market

Market snapshot: macro trajectory and what it means

The global market for gas pressure regulators in oil & gas has demonstrated steady expansion through the historical period and is positioned for continued growth in the forecast window. As of the base year 2025 the market reached a multi-billion-dollar scale (measured in USD, revenue in millions), and our modeling indicates a compound annual growth rate of 5.12% for the 2026–2032 forecast period. By the end of the forecast horizon the market is projected to be materially larger than in 2025, reflecting the combined effects of increased pipeline activity, aging infrastructure replacement, and rising deployment of specialized regulators for high-pressure, subsea and hydrogen-ready applications.

Gas Pressure Regulators For Oil Gas Market

For 2026, that growth profile creates a particular set of tactical and strategic choices: how to allocate R&D budgets between ruggedized mechanical designs and digital-enabled regulators; when to consolidate suppliers or lock in long-term raw-material contracts; and where to prioritize geographic and application focus to capture aftermarket share. The full report provides the detailed market model and scenario outputs that translate this macro trajectory into revenue-risk profiles by product family and channel.

Gas Pressure Regulators For Oil Gas Market

Why 2026 is a pivot year

- CapEx cycles are reaccelerating. Operators in transmission and distribution are moving from maintenance-only postures into proactive replacement and upgrade programs, increasing demand for reliable pressure control across a range of duty cycles.

- Standards and compliance are tightening. International and industry standards—covering quality systems, sour-service metallurgy, and performance testing—are shaping procurement specifications. Conformity to IOGP S-739Q, NACE MR0175/ISO 15156 and ISO 23555-2 increasingly appears in bid requests and supplier evaluations, raising the bar for certification and traceability.

- Supply chain sensitivity is material. Stainless steel (notably 316 grade) remains the primary material choice for corrosive and sour environments. Variability in regional supply and pricing for 316 and other alloys is elevating procurement risk; 2026 is the year many buyers will choose longer contracts, dual-sourcing strategies, or local stocking arrangements to stabilize MRO availability.

- Technology bifurcation. The market is splitting into two performance tracks: hardened mechanical regulators optimized for extreme, subsea and sour conditions, and digitally instrumented regulators with diagnostics and remote monitoring for distribution and midstream segments. Each requires a different route-to-market and aftermarket service model.

What the report delivers — practical, actionable components

PW Consulting’s full study is organized to turn market intelligence into executable choices. Highlights include:

- Forward-looking demand scenarios that translate aggregate CAGR into probabilistic revenue bands by application group and product family (suitable for budgeting and M&A screening).

- Supplier benchmarking and capability matrices that map vendor strengths against key procurement criteria: compliance posture, materials traceability, noise and emissions mitigation, high-pressure/subsea capability, and digital enablement.

- Supply-chain stress tests that quantify exposure to alloy-price swings and single-source dependencies, and model the impact of alternate sourcing or inventory strategies on lead times and total landed cost.

- Regulatory-impact assessments aligning IOGP, ISO and NACE requirements to procurement checklists and recommended QMS upgrades for OEMs and specifiers.

- Commercial playbooks for OEMs and distributors: channel segmentation, margin pools, aftermarket service propositions, and a prioritized list of product enhancements that create first-mover advantages in 2026.

Competitive landscape — who matters and why

The market exhibits a moderate concentration: established multinational OEMs coexist with specialized regional manufacturers and niche engineering houses. The top-tier incumbents are notable for integrated portfolios, broad certification footprints, and deep field-service networks; smaller players differentiate on specialization (e.g., hydrogen, subsea, LPG) or local presence.

- Emerson (Fisher/TESCOM/Tartarini) — Strengths: comprehensive portfolio spanning distribution to high-pressure control, strong reputation for reliability, and product features like no-bleed designs and acoustic noise reduction. Strategic advantage: scale in field-service, established relationships with utilities and gas distributors, and the ability to bundle pressure regulation with broader flow-control systems.

- Swagelok Company — Strengths: precision engineering and rigorous testing regimes for high-purity and varied flow rates. Strategic advantage: appeal to process-intense upstream and chemicals customers who prioritize tight tolerances and corrosion-resistant materials.

- Honeywell — Strengths: integration of pressure regulators with control and safety systems, corrosion-resistant components, and smart monitoring options. Strategic advantage: cross-selling into automation and digital operations segments; attractive to operators seeking an integrated safety-control stack.

- BelGAS (Marsh Bellofram) — Strengths: depth in high- and low-pressure regulator models, with legacy products used widely in distribution networks. Strategic advantage: recognized product families for farm taps and rural distribution, and a footprint in aftermarket replacement parts.

- Pietro Fiorentini / FIORENTINI USA — Strengths: focused solutions for transmission and metering integration; strong European engineering heritage. Strategic advantage: well-positioned for large-scale distribution and transmission contracts that demand tight integration between regulation and metering.

- Pressure Tech Ltd — Strengths: engineering for hydrogen, subsea and high-pressure service. Strategic advantage: early mover in alternative-fuel and subsea niches where material and sealing engineering makes the difference.

- Cavagna Group, RegO, Maxitrol — Strengths: specialist portfolios across LPG, natural gas and industrial burners. Strategic advantage: local manufacturing and channel reach for commercial and industrial end-users, plus rapid aftermarket response.

Tactical insight: the market rewards two distinct supplier archetypes in 2026—scale players who can assure rapid global deliveries and certification, and high-specialists who can meet demanding sour-service and hydrogen-ready specifications. Structuring procurement frameworks to use both archetypes reduces operational risk while preserving optionality.

Signals from the field: events and recent developments

- Industry exhibitions in 2025–2026 highlighted a renewed focus on harsh-environment performance and subsea reliability. Participants at major trade shows showcased solutions optimized for extreme duty cycles and improved noise/emissions characteristics.

- Conversations at large engineering events point to increased buyer scrutiny around standards compliance and third-party certification, and a preference for suppliers who can demonstrate traceable metallurgy and fatigue testing for sour-service applications.

Strategic playbook for 2026

Executives reading this preview should consider the following priority moves in the coming 12–18 months:

- Procurement hedging: Establish layered supplier agreements (global OEM + regional specialist) and negotiate raw-material escalation clauses tied to transparent indices. Where inventory carrying cost is justified, pre-buy critical alloy inventories or use consignment models with trusted suppliers.

- Product roadmap alignment: Prioritize two parallel development tracks—ruggedized, certification-heavy mechanical regulators for high-pressure/subsea/sour service, and digitally-enabled regulators for distribution networks with condition-monitoring features to reduce unplanned downtime.

- Certification and QA investment: Accelerate ISO/IOGP/NACE alignment in procurement and QA checklists. Certification readiness will shorten bid-to-award cycles and open doors to larger pipeline transmission contracts.

- Aftermarket differentiation: Build aftermarket service packages (predictive maintenance, spare-parts logistics, rapid swap kits) that convert installed-base into recurring revenue—particularly valuable in power-constrained or remote operations.

- M&A and partnership screening: Use the market’s moderate fragmentation to identify bolt-on acquisitions that close capability gaps (e.g., hydrogen compatibility or subsea pressure control) or provide strategic geographic access.

How PW Consulting’s report helps you act

This research is designed as a pragmatic tool for decision-makers. Beyond the headline market trajectory and competitor overviews, the report contains: granular demand models, supplier heatmaps, contract clause templates for alloy price risk, an ISO-compliance playbook, and scenario-based financial impacts for procurement choices. Each deliverable is packaged to support board-level capital allocation and operational procurement strategies.

We intentionally limit the data shown in this public preview to preserve the tactical value of the full dataset. The complete report contains the detailed regional and application splits, supplier scorecards, and downloadable models you can use directly in 2026 budgeting and sourcing processes.

Next steps

If your organization is preparing procurement cycles, evaluating M&A opportunities, or defining product roadmaps for pressure regulators in oil & gas, the full PW Consulting report provides the prioritized action lists and quantitative templates to put plans into motion. Contact PW Consulting to access the complete dataset, modeling workbooks, and the supplier benchmarking annex referenced throughout this preview.

For detailed analysis of this topic, please visit the official page:Gas Pressure Regulators For Oil Gas Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com