Europe Alternative Proteins Market Overview: Key Drivers and Challenges

Networking |

2026-03-25 01:52:12

PW Consulting’s latest market research on Tyre Pyrolysis Oil (TPO) synthesises five years of historical data and a forward-looking forecast to 2032, delivering the strategic intelligence executives need to convert regulatory change and early commercialisation into durable competitive advantage. Built on a 2025 base year and projecting through 2032, the study models the market’s growth trajectory (CAGR 5.29% over the forecast window) and provides practical decision tools for corporate strategy, project finance, and commercial operations in 2026 and beyond.

Tyre Pyrolysis Oil Market

Regulatory inflection points are crystallising market access. RED III’s mid‑2025 alignment of the biogenic portion of TPO with advanced biofuel frameworks and recent national decisions recognising TPO as a chemical feedstock (notably France in early 2026) materially improve predictability for offtake and product qualification.

Tyre Pyrolysis Oil Market

Technology and project milestones are moving from pilots to industrial scale. The first large-scale plant inaugurations and reactor additions seen in early 2026 mark the transition from demonstration risk to deployment risk — a shift that alters capital allocation, contracting structures, and insurance requirements.

Tyre Pyrolysis Oil Market

Market structure remains fragmented. Market concentration metrics in our study show a low top‑tier share (CR3 ~18.4%, CR5 ~25.15%), signalling opportunity for new entrants, roll‑up strategies, and geographies where first‑mover scale will deliver outsized commercial advantage.

Market sizing & scenario modelling — Our model reconciles historical 2020–2025 observations with multiple demand and policy scenarios to generate a base-case forecast and stress cases through 2032. Readers will find year‑by‑year market size projections (the study tracks market growth from the 2020 baseline through 2025 and into the 2026–2032 forecast window), with sensitivity runs for feedstock availability, regulatory treatment, and product uptake in chemicals and fuels.

Feedstock and yield analytics — We map end‑of‑life tyre (ELT) availability and typical conversion metrics (typical crude TPO yields on a steel‑free basis and key physicochemical properties), enabling realistic feedstock sourcing strategies and break‑even calculations for plant deployments.

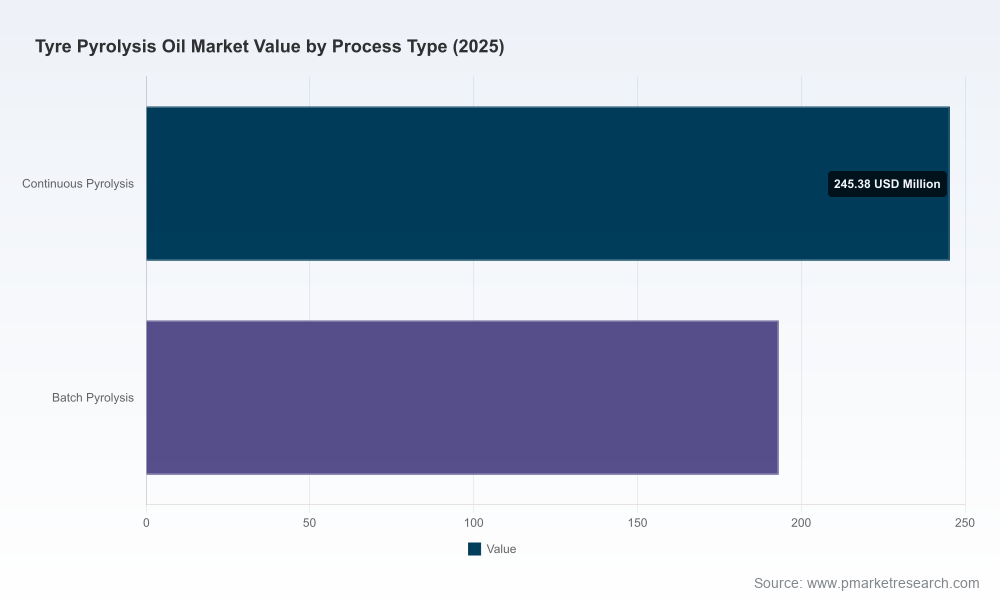

Techno‑economic playbooks — Comparative capital and operating cost frameworks for continuous vs batch pyrolysis routes, modularisation options, and retrofit pathways. Practical decision checklists cover reactor sizing, integration scope (recovered carbon black handling, steel separation), and product upgrading necessities required for chemical‑grade or fuel‑grade offtakes.

Certification & market‑access roadmaps — Step‑by‑step guidance on ISCC, REACH-related registration pathways, and documentation needed to monetise biogenic credits or RCF‑like value streams under EU frameworks. The report maps what certification unlocks for offtake conversations with refiners, petrochemical players, and biofuel aggregators.

Commercial contracting templates & negotiation guides — Standardised term sheets, quality specifications, risk‑allocation clauses, and pricing indexation strategies for TPO offtake, feedstock supply, and co‑product sales (recovered carbon black, steel). These are designed for rapid adaptation by legal and commercial teams.

Risk matrices & capital allocation tools — A focused investment prioritisation matrix that helps boards and investment committees decide between greenfield scale, bolt‑on capacity, licensing, or strategic partnerships based on expected returns, time to revenue, and regulatory exposure.

Competitive benchmarking and M&A scouting — Company profiles, capability assessments and a ranked universe of near‑term M&A candidates or licence partners tailored to different strategic archetypes: pureplay technology providers, integrated recyclers, and commodity traders.

The early commercial wave is anchored by a small but active set of technology and project companies whose moves in 2025–2026 set practical benchmarks for scale, certification, and market access. PW Consulting’s report provides a qualitative and tactical appraisal of the leading actors to inform partner selection, due diligence scope, and alliance strategies.

Circtec — Circtec’s Delfzijl project in the Netherlands, inaugurated in January 2026, represents one of Europe’s first large‑scale ELT pyrolysis plants moving into commercial production. The phased expansion roadmap (initial capacity with line‑of‑sight to significant scale‑up within the same site) is instructive: it demonstrates how stepwise commissioning and offtake layering can de‑risk financing while securing feedstock catchment areas. For investors and strategic offtakers, Circtec’s model is a template for staged balance‑sheet exposure and offtake hedging.

Pyrum Innovations AG — Pyrum’s regulatory wins in early 2026, including national recognition and ISCC EU certification for thermolysis oil, highlight the value of proactive regulatory engagement and certification-first commercial strategies. Pyrum’s approach demonstrates how aligning technology deployment with certification milestones can create premium market access to biofuel and chemical markets.

Klean Industries — A physically global builder and licensor, Klean’s project footprint and partnerships (including licence routes) illustrate the two-pronged strategy of project delivery plus intellectual property monetisation. For corporates seeking rapid capacity expansion or turnkey project execution, licensing relationships reduce lead time but require strict quality control regimes to preserve end‑product value.

New Energy Kft. — An early adopter of continuous charge chemistry recycling, New Energy’s certification achievements and continuous process focus underscore operational choices that favour throughput and steady product specs; valuable for buyers demanding consistent compositional quality for petrochemical feedstocks.

Enespa AG — Acting as a bridge between producers and industrial consumers, Enespa’s trading, analytical and regulatory support services reveal a fast‑emerging role: professionalising TPO into a reliable traded commodity through lab verification, REACH advisory, and logistics optimisation. Buyers and sellers should consider partnering with such intermediaries to reduce settlement and quality disputes.

Understanding the multi‑fraction nature of TPO is essential to commercial strategy. Typical crude TPO yields and properties (density, calorific value and a moderate sulphur band) determine downstream handling, upgrading needs and price differentials between fuel and chemical routes. Under RED III, the biogenic share of TPO is now contractually monetisable under certain advanced biofuel pathways, while the fossil portion may qualify for value as Recycled Carbon Fuel where GHG savings reach the necessary thresholds — a bifurcated market logic that informs whether a project targets fuel markets, chemical co‑processing, or blended industrial heat customers.

Prioritise certification early — Projects that sequence ISCC/ISCC PLUS and relevant national approvals prior to large‑volume offtake negotiations gain commercial leverage and price premium opportunities.

De‑risk with staged capacity rollouts — The financing landscape rewards staged commissioning (pilot → commercial line → phase‑out expansion); this reduces technology delivery risk while permitting early revenue capture.

Lock feedstock via diversified sourcing — Contract structures that blend long‑term ELT supply with spot procurement reduce single‑supplier exposure and support throughput optimisation across pyrolysis routes.

Define product pathways before plant design — Engineering choices (degree of upgrading, desulphurisation, stabilisation) should follow the target market (refinery co‑processing vs chemical precursors vs fuel) to avoid costly retrofits.

Evaluate partnering over owning in unfamiliar geographies — Licensing or joint ventures with local ELT managers and established technology vendors can accelerate market entry while capping capex exposure.

Build trading and quality assurance capabilities — Even producers benefit from third‑party trading expertise to manage logistics, QC, and contract enforcement in nascent TPO markets.

To preserve the strategic utility of this executive brief — and to follow our “trailer” principle — we have intentionally summarised core insights while withholding granular subsegment shares, region‑level percentages and company‑level financials. The full report includes complete regional and application segmentation, plant‑level techno‑economic models, downloadable scenario spreadsheets, and editable commercial templates. These proprietary datasets are critical for precise capex modelling, price curve construction and target screening.

PW Consulting’s Tyre Pyrolysis Oil Market Report is designed for boards, corporate strategy teams, project developers, and investors preparing binding commitments in 2026. If your team is preparing an FID, negotiating a long‑term offtake, or structuring a licensing partnership, the full dataset and playbooks will materially shorten your time to contract and reduce execution risk.

Request the full report and model package to run bespoke scenarios against your asset base and preferred commercial architecture.

Book a strategic workshop with PW Consulting to convert report recommendations into a 90‑day implementation plan — covering feedstock contracts, certification sequencing, and capital mobilisation priorities.

In a market growing on a compound trajectory and moving from demonstration to commercial scale, 2026 will reward organisations that couple regulatory foresight with pragmatic operational sequencing. PW Consulting’s study equips decision makers to do exactly that — turning policy signals, plant‑level learnings, and certification pathways into executable strategy.

For detailed analysis of this topic, please visit the official page:Tyre Pyrolysis Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com