Fairdeal - Trusted Platform Offering Online Cricket ID and Live Cricket Betting Opportunities Daily

Games |

2026-06-30 14:31:21

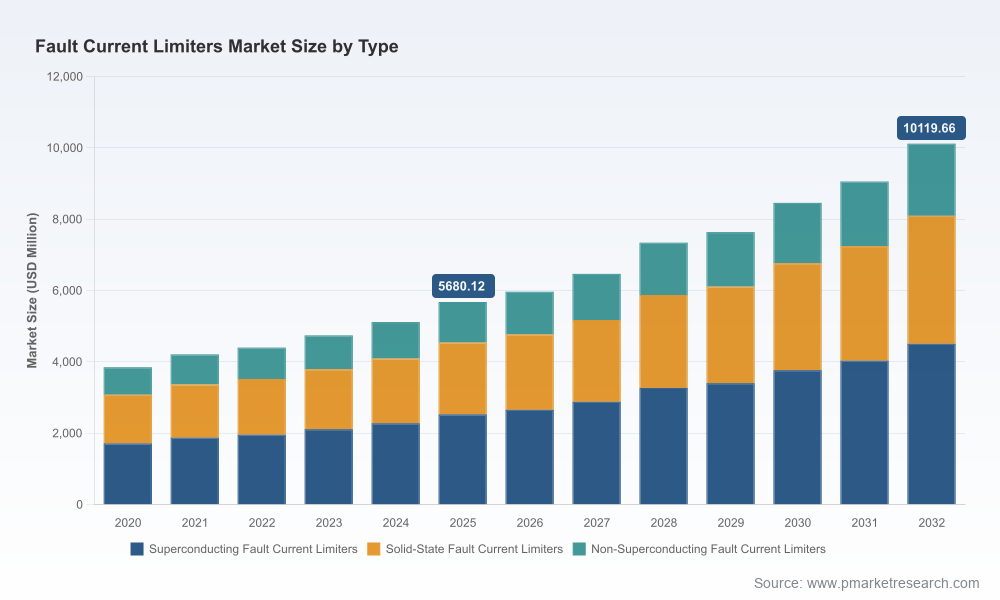

As power systems bend under the combined pressures of rapid renewable integration, electrification of transport, and aging distribution infrastructure, fault current limiters (FCLs) have moved from experimental niche to essential mitigation technology. PW Consulting’s latest Fault Current Limiters Market report — with a 2025 base year and a 2026–2032 forecast horizon — provides the actionable intelligence that executive teams, asset owners, and investors need to set priorities in 2026. The market is forecast to sustain an approximate 8.58% compound annual growth rate through the forecast period, expanding from a multi-billion-dollar global market in 2025 to more than ten billion USD by 2032. This release explains why timing, technology choice, and supply-chain risk management will define winners and losers in the next two years.

Fault Current Limiters Market

Strategic timing: Procurement cycles, grid upgrade budgets and regulatory milestones converge in 2026. The report models multiple adoption timing scenarios so stakeholders can align pilot, scale-up and capex decisions with realistic delivery windows and price-learning curves.

Fault Current Limiters Market

Technology selection under uncertainty: With competing approaches — superconducting, solid-state, and non-superconducting/resistive options — buyers face trade-offs across performance, maintenance complexity, and lifecycle cost. Our analysis provides comparative techno-economic pathways and a clear decision framework for 2026 pilots versus longer-term rollouts.

Fault Current Limiters Market

Supply-chain and materials readiness: High-temperature superconducting (HTS) tape availability and cryogenics remain key enablers for SFCLs. The report quantifies exposure to HTS supplier concentration and identifies mitigation strategies for procurement teams evaluating long-lead components in 2026.

Regulatory alignment and compliance playbook: Ongoing standardization efforts (including IEEE work for testing of FCLs above 1,000 V AC) and increasing grid-code requirements for inverter-dominated resources make regulatory risk a core commercial consideration. We translate standards evolution into procurement and test-spec milestones for 2026 tenders.

Market sizing and scenario forecasts: A clear baseline (base year 2025) and iterative scenario modeling to 2032, driven by adoption curves tied to renewable curtailment risk, interconnection projects, and distribution automation programs.

Technology roadmaps and ROI templates: Comparative lifecycle cost models for SFCLs, solid-state FCLs, and conventional resistive/transformer-based limiters, including sensitivity to HTS price reductions and cryogenics complexity.

Vendor scorecards and procurement playbooks: Objective vendor assessments that synthesize technology maturity, field deployments, service ecosystems, and partnership networks into procurement-ready evaluation criteria and RFP language.

Pilot design and test protocols: Practical specifications for utility pilots, including key performance indicators, fault-testing sequences aligned with emerging IEEE guidance, and acceptance criteria for interconnection to inverter-based resources.

Regulatory risk matrix and compliance timelines: Mapping of grid-code changes, regional safety standards, and railway electrification requirements into concrete compliance actions through 2026.

Supply-chain risk mapping: Identification of critical material nodes (e.g., YBCO/HTS tapes), concentration risks among suppliers, and recommendations for hedging strategies and dual-sourcing approaches.

Commercial playbook for integrators and OEMs: Go-to-market approaches for utilities, data centers, rail operators and industrial end-users, including bundling strategies with switchgear and protection systems to accelerate adoption.

The market is characterized by a blend of diversified electrical equipment majors, superconducting specialists, regional manufacturers, and niche technology challengers. Market concentration is meaningful but not prohibitive: a handful of established suppliers capture a substantial share of commercial-scale deployments, while a long tail of specialized suppliers competes in targeted verticals such as rail traction and data centers.

ABB Ltd. (Switzerland) — Strength lies in integration: ABB pairs solid-state FCLs with transmission and distribution offerings and leverages a broad service network. Their play is optimized for utilities integrating high shares of renewables and multiple interconnection points.

Siemens AG (Germany) — Technology breadth and systems integration capability give Siemens an advantage for large, utility-scale projects. Siemens’ portfolio spans superconducting and conventional technologies, which positions them for multi-technology competitive tenders.

Schneider Electric (France) — Deep presence in medium-voltage distribution and industrial segments makes Schneider a preferred partner for facility-level deployments and distribution automation programs, especially where integration with energy management systems matters.

Nexans (France) — A leader in superconducting FCLs with focused rail deployments, Nexans is distinguishing itself with dedicated traction network solutions. Recent scheduled rail deployment highlights its position in cross-border rail electrification projects.

American Superconductor Corporation (AMSC, United States) — AMSC’s Amperium HTS wire and SFCL systems target utility substations and resilience projects, offering a verticalized superconducting value chain that reduces integration friction for buyers seeking high-performance, low-loss solutions.

Eaton Corporation (Ireland) — Eaton’s strength is in integration of FCL functionality with switchgear and distribution assets, creating compelling total-cost-of-ownership propositions for industrial and utility-scale distribution projects.

GE Grid Solutions (United States) — Broader grid protection portfolios and global reach enable GE to offer FCL technologies as part of modernization packages, often bundled with protection relays and digital grid services.

Regional and niche players — Companies such as Rongxin (China), GridON (Israel), Wilson Transformer (Australia), LS Electric (South Korea), SuperOx (Russia), SuperPower (US), and Furukawa (Japan) deliver differentiated options — from resistive-type and saturable-core FCLs to HTS components — that are particularly relevant in vertically specialized markets (rail, data centers, wind farms).

Recent vendor activity underscores the market’s maturation: Nexans has scheduled a rail SFCL deployment on a cross-border traction link, signaling regulatory and operational acceptance for superconducting solutions in rail; LS Electric showcased a customized superconducting package for data centers, highlighting the technology’s appeal in mission-critical private networks. These moves foreshadow a broader shift from pilot projects to procurement-ready offerings in specific verticals during 2026.

Standards and testing — Ongoing IEEE efforts to establish testing protocols for FCLs rated above 1,000 V AC will reduce certification uncertainty and shorten procurement lead times once finalized. Utilities and integrators should bake these expected standards into 2026 test plans and acceptance criteria.

Renewables and grid-code pressures — Grid-code requirements for fault ride-through and dynamic current contribution by inverter-based resources are accelerating FCL adoption at renewable interconnection substations. Our adoption models quantify the rate at which those requirements translate into procurement volumes under different policy scenarios.

Materials and technology evolution — The trajectory of HTS tape cost and cryogenic complexity is the principal determinant of SFCL competitiveness. Advances that reduce cryogenics footprint materially alter lifecycle economics and expand viable applications beyond niche high-voltage projects.

Rail and urban grid deployment momentum — European safety standards and national electrification initiatives are making SFCLs an increasingly practical alternative to infrastructure-heavy fault mitigation measures in rail and dense urban networks.

Move from pilots to portfolio staging — Organizations that executed early pilots should use 2026 to define staged procurement frameworks that align pilots to network-wide deployment triggers (e.g., interconnection agreements, inverter-penetration thresholds, or regulatory milestones).

Adopt a dual-track procurement strategy — Combine short-term, lower-complexity solid-state or resistive FCL purchases for immediate risk mitigation with targeted SFCL investments where lifecycle benefits justify longer adoption lead-times.

Hedge HTS exposure — Include material-sourcing clauses, second-source qualification, and strategic inventory cushions for HTS tapes and cryogenic components in 2026 contracts.

Use standards as de-risking levers — Demand IEEE-aligned test certificates and include acceptance test protocols that reflect anticipated regulatory updates to reduce retrofit risk.

Prioritize vendor ecosystem fit over single-product metrics — Evaluate suppliers on installation capability, O&M network, and digital integration rather than purely on prototype performance figures.

This briefing surfaces the macro trajectory of the global FCL market, including base-year sizing (2025), a robust forecast trajectory to 2032, and the headline compound annual growth rate (approx. 8.58%). It synthesizes competitive positions, recent commercial milestones, and the critical regulatory and material constraints that buyers must address in 2026. In keeping with our “trailer” principle for this public release, detailed segmentation splits across regions, voltage levels, and application-specific revenue shares are withheld here. Readers will find those detailed segment-level analyses, region-application matrices, vendor quantitative scorecards, and downloadable procurement templates within the full report and data annex available on the PW Consulting website.

Schedule a strategy session: Use the report’s vendor scorecards and ROI templates to create a 12–24 month roadmap aligned to your capex cycle.

Initiate dual-sourcing pilots: Begin supplier qualification for both superconducting and solid-state options in 2026 to shorten time-to-deployment.

Embed standards readiness: Update tender documents and pilot acceptance tests to reflect anticipated IEEE and national standard timelines.

PW Consulting’s Fault Current Limiters Market report equips decision-makers to convert complexity into a concrete 2026 action plan. For the full data tables, segmented forecasts, and procurement-ready annexes, visit the full report page to unlock the complete intelligence set needed to operationalize your 2026 FCL strategy.

For detailed analysis of this topic, please visit the official page:Fault Current Limiters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com