Smart Broadcasting Technologies Accelerating FM Broadcast Transmitter Industry Growth

Other |

2026-05-08 10:47:11

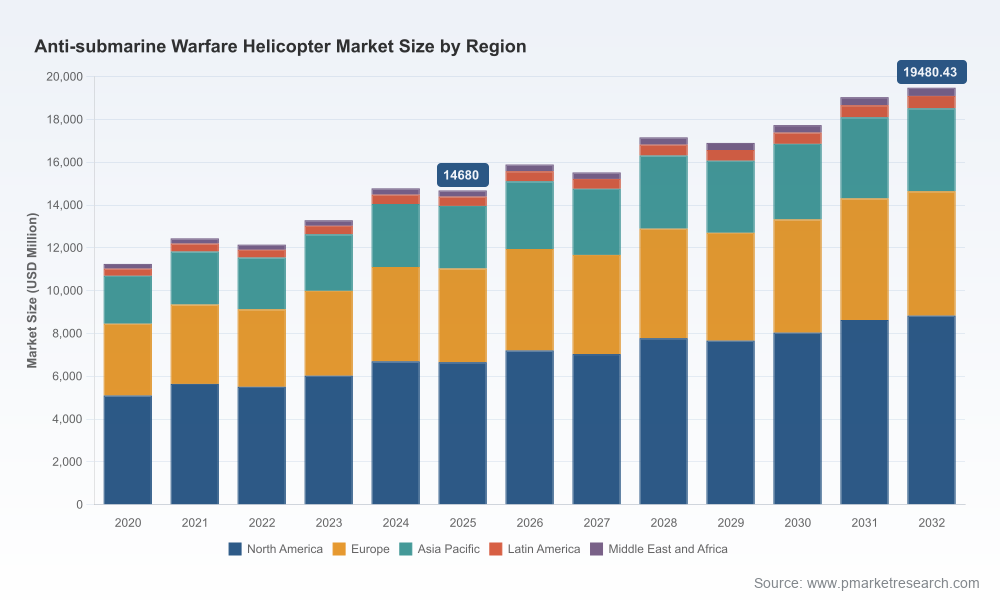

PW Consulting’s latest market study on Anti-Submarine Warfare (ASW) helicopters delivers a concentrated, decision-oriented intelligence package designed for defense planners, primes, OEM suppliers, and investors preparing strategic action in 2026. The global ASW helicopter market — with a 2025 baseline of USD 14,680 Million — is projected to re-accelerate in 2026 and grow at a steady compound annual growth rate (CAGR) of 4.12% through the 2026–2032 forecast window, reaching an overall market size approaching USD 19,480 Million by 2032. This trajectory reflects a combination of recapitalization programs among allied navies, expanding export opportunities, and parallel investments in sensors, weapons, and unmanned adjuncts that collectively reshape procurement and sustainment priorities.

Anti Submarine Warfare Helicopter Market

Timing: 2026 is a pivotal procurement year for multiple navies whose recapitalization and modernization programmes are moving from concept to contracting. Our analysis synthesizes the operational, industrial and geopolitical inflection points that will dictate contracting windows, financing structures, and offset strategies.

Anti Submarine Warfare Helicopter Market

Actionability: The study is built around tools that support near-term decisions — modular acquisition checklists, procurement timing matrices, lifecycle cost-of-ownership models, and risk-adjusted supplier shortlists — enabling defensible choices on platform selection, sustainment posture, and industrial participation.

Anti Submarine Warfare Helicopter Market

Competitive clarity: The market shows meaningful concentration — top-three OEMs account for a clear majority of market share while the top-five widen the concentration further — a structure that favors established primes but also creates niches for specialized subsystems, unmanned systems, and MRO entrants.

Market sizing and trajectories: A consolidated topline model from 2020–2025 and a detailed forecast through 2032 with scenario sensitivity for high/low demand environments driven by geopolitical shocks and defense budget cycles.

Procurement playbooks: End-to-end guidance for ministries of defense and acquisition teams, covering procurement architectures (direct purchase, lease-to-own, Foreign Military Sales routes), negotiation levers, and contract clauses that protect sovereign sustainment needs.

Vendor performance dossiers: Strategic profiles of incumbents and challengers, capability maps across sensors, weapons integration, shipboard compatibility, and global sustainment footprints (public synopses included; full vendor matrices and scorecards are reserved for subscribers).

Operational integration blueprints: Practical checklists for integrating manned helicopters with shipborne combat systems and unmanned ASW assets, including sonobuoy management, tactical data links, and mission system architectures.

Supply chain and industrialization playbook: Risk register and mitigation pathways for key supply nodes, inventory policy prescriptions (spares, consumables, torpedoes), and options for nearshoring vs. globalized sourcing to maintain operational availability.

Commercial scenarios and ROI tools: Decision-support spreadsheets and NPV models to compare procurement mixes (new-build vs. upgrade vs. leased), sustainment outsourcing vs. in-house MRO, and implications for sovereign industrial participation.

Geopolitical realignment and defence budgets: NATO allies and several Asia-Pacific navies are prioritizing ASW capability as a strategic hedge. Higher defense budget allocations across key allies create procurement tailwinds for ASW platforms and integrated mission systems.

Export dynamics and approvals: Continued use of established export mechanisms — including U.S. Foreign Military Sales — is expanding fleet interoperability among partner navies. Recent notifications and approvals have direct implications for program timelines and supplier lead times.

Platform evolution: The manned ASW helicopter remains the centerpiece of blue-water ASW, but its role is being re-cast within a distributed sensor-shooter construct that includes unmanned surface and aerial vehicles and more integrated torpedo/sonobuoy management.

Industrial concentration and competitive pressure: A market dominated by a relatively small set of OEMs concentrates negotiation power but also leaves procurement authorities dependent on a finite set of sustainment ecosystems.

Lockheed Martin (Sikorsky): The MH-60R Seahawk continues to anchor U.S. and allied ASW forces. Delivery milestones and steady production cadence reinforce Sikorsky’s position as a cornerstone supplier. The 350th MH-60R delivery in early 2026 demonstrates production maturity and supports export momentum.

NHIndustries (Airbus Helicopters, Leonardo, Fokker): The NH90 Sea Tiger variant is entering operational fleets, with initial deliveries in late 2025 marking the start of a multi-year in-service ramp. As a consortium product, its industrial and political footprint has distinct implications for Europe-led naval programs.

Leonardo Helicopters: With the AW159 Wildcat and participation in NH90 supply chains, Leonardo remains a flexible partner for mid-sized navies seeking tailored ASW solutions and local industrial partnerships.

AVIC (Harbin): China’s Z-20F/Z-18F series and mass production activities point to growing regional self-sufficiency and export ambitions within regional alignments — a factor that shifts competitive dynamics in Asia-Pacific procurement planning.

Kamov (Russian Helicopters): The Ka-27/28 family retains relevance through modernization and refresh programs in existing fleets and export channels, particularly among operators with legacy coaxial rotor requirements.

Airbus Helicopters (unmanned effort): The VSR700 unmanned ASW system signals a strategic pivot toward mission kits and unmanned augmentation; buyers evaluating future-proofing should weigh unmanned interoperability as a key procurement criterion.

Procurement architecture should be phased and diversity-aware. Ministries should design mixes that combine mature manned platforms with an acquisition roadmap for unmanned adjuncts to reduce operational risk and accelerate capability delivery.

Negotiate sustainment commitments early. With market concentration favoring established primes, securing long-term MRO rights, local capability transfer, and predictable spares provisioning will materially affect lifecycle costs and fleet availability.

Invest in systems integration capability. The value in ASW now lies in the mission system and sensor-to-shooter orchestration; ministries and suppliers that can demonstrate rapid integration of sonobuoy management, dipping sonar data fusion, and torpedo control will win tenders.

Build industrial hedges. Suppliers and governments should develop dual-track supplier strategies — combining incumbent relationships with targeted investments in small-to-medium enterprise (SME) subsystem suppliers — to reduce single-source vulnerabilities.

Prepare for export-control friction. Program timelines must factor potential delays from export licensing, offsets and political approvals; scenario planning and contract clauses around approval contingencies are now procurement best practice.

Adopt predictive sustainment. Digital twins, condition-based maintenance, and data-driven spares policies can materially reduce downtime and cost-per-flight-hour over the lifetime of an ASW fleet.

Executives will find two distinct outputs in the report especially useful for 2026 decision cycles: (1) a customizable procurement and cost-of-ownership model that converts capability options into multi-year budget needs and affordability envelopes; and (2) a supplier risk and readiness index that ranks vendors across industrial capacity, exportability, sustainment footprint, and upgrade pathways. These outputs are packaged with stakeholder brief decks and vendor engagement templates to accelerate decision timetables while protecting negotiating positions.

To preserve our “trailer” principle and ensure clients access the full analytical depth, this public brief emphasizes strategic conclusions and market-level trajectories while withholding granular segment-by-segment figures, country procurement-by-procurement breakdowns, and detailed vendor scorecards. The full report contains the segmented market model, region- and application-level forecasts, granular CR-based share tables, and line-item supplier assessments that procurement teams use to finalize requirements and contractual terms.

90 days: Finalize capability requirements and draft RFP language that prioritizes modular mission-system interfaces and sustainment guarantees. Open supplier dialogue with key primes to validate lead-times and options for local workshare.

180 days: Execute affordability stress tests against the PW Consulting cost-of-ownership model; begin formal industrial partnership negotiations to secure MRO and training commitments.

360 days: Lock in a phased procurement schedule that blends initial capability delivery with a roadmap for unmanned integration and mid-life upgrades, and institute the digital sustainment platform across the nascent fleet.

As ASW helicopter procurements shift from symbolic commitments to executable programs in 2026, decisions taken this year will set sustainment, industrial and operational trajectories for decades. PW Consulting’s Anti-Submarine Warfare Helicopter Market report provides the market sizing, scenario workstreams, and actionable procurement tools that program managers and defense executives need to move from planning to contracting with confidence. For access to the full segmented dataset, the vendor scorecards, and the procurement toolkits — including the detailed country- and application-level forecasts withheld from this brief — visit PW Consulting’s report portal or contact our strategic sales team to arrange a licensed briefing.

For detailed analysis of this topic, please visit the official page:Anti Submarine Warfare Helicopter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com