TV Series Jackets

Shopping |

2026-05-20 14:02:36

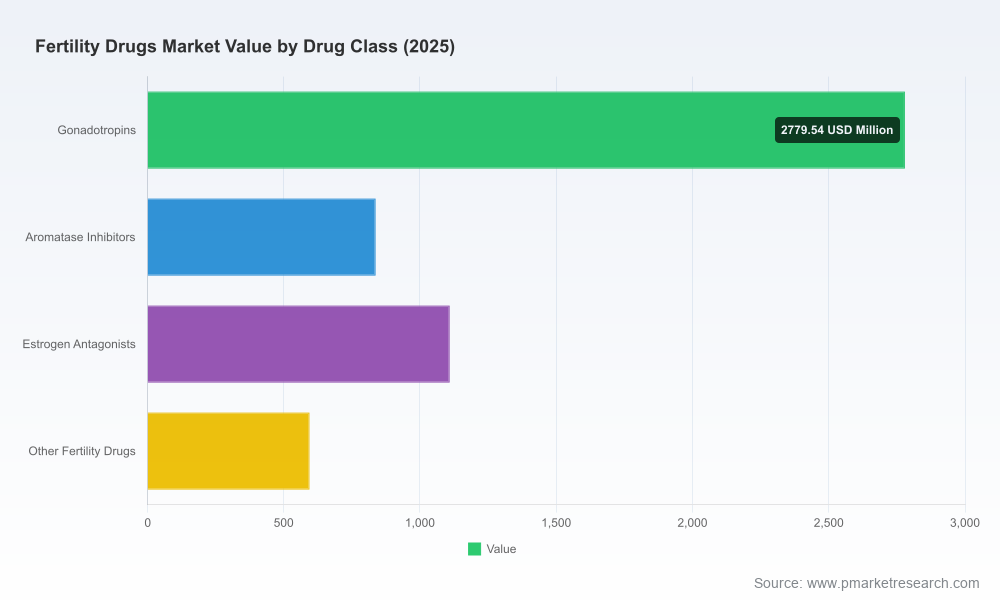

PW Consulting’s latest Fertility Drugs Market report — anchored to a 2025 base year and projecting through 2032 — equips executives with the evidence-based, decision-ready intelligence they need to act in 2026. The market has moved from roughly USD 3.95 billion in 2020 to about USD 5.32 billion in 2025, and our modelling projects continued expansion to the low‑to‑mid billions by 2032 at a compound annual growth rate of 6.1% across the 2026–2032 forecast window. Market concentration is material: the three largest companies command a majority share and the top five together account for over 80% of market value — a structural reality that shapes pricing power, access to distribution, and competitive responses.

Fertility Drugs Market

Timing: 2026 is a pivot year. Regulatory shifts, supply vulnerabilities, and the accelerating entry of generics and biosimilars are converging to reshape margins and go‑to‑market models.

Fertility Drugs Market

Actionability: The report translates macro growth into executable choices — which molecules to prioritize for biosimilar investment, where to de‑risk manufacturing footprint, and how to recalibrate commercial models in the face of direct‑to‑consumer pricing initiatives.

Fertility Drugs Market

Risk-to-reward clarity: We quantify the trade‑offs between defending branded franchises versus pursuing lower‑margin generic expansion, and map the scenarios under which each route maximizes enterprise value.

Market sizing & trajectory: A transparent, bottom‑up model reconciling historical performance (2020–2025) with scenario‑tested forecasts (2026–2032) that executives can re-run with their own assumptions.

Commercial playbooks: Go‑to‑market blueprints for branded gonadotropins, oral ovulation inducers, and emerging biosimilars — including pricing levers, channel economics, and payer engagement scripts tailored to different reimbursement regimes.

Portfolio prioritization matrix: A decision framework that ranks assets by strategic value, regulatory complexity, and revenue at risk, enabling resource allocation across R&D, lifecycle management, and marketing.

Supply‑chain & manufacturing risk map: End‑to‑end visibility on critical raw materials and biologics manufacturing capacity, plus contingency pathways for shortages and capacity constraints.

Regulatory & reimbursement scenarios: Four plausible regulatory outcomes — from rapid biosimilar approvals to price‑intervention regimes — and their quantified P&L impact over a five‑year horizon.

M&A & partnership funnel: A screened list of inorganic targets and co‑development candidates, with valuation levers and integration risk profiles tailored to each strategic thesis.

Provider and patient journey analytics: Data‑driven insights on clinic protocol shifts, cycle economics for assisted reproductive technologies (ART), and points of friction where commercial interventions can increase uptake and adherence.

The competitive field combines established multinational innovators with regionally strong generics and emerging biosimilar specialists. Incumbent leaders maintain a durable advantage in high‑complexity biologics, supported by integrated R&D, specialized manufacturing, and deep clinic relationships. At the same time, agile generic and biosimilar entrants are compressing price points on commoditized oral agents and moving up the value chain into biologics.

Global innovators (e.g., firms with comprehensive gonadotropin portfolios): Their strengths lie in clinical trust, long history within IVF protocols, and capacity to bundle therapies with diagnostic and services propositions — a powerful defense against pure price competition.

Big pharmas and branded portfolios: These players can deploy broad commercial networks and payer relationships to defend margins, but they face strategic choices around investing in biosimilar countermeasures versus protecting legacy branded lines.

Generics & regional champions: Cost‑focused manufacturers are rapidly scaling availability of oral ovulation inducers and generics of legacy agents, pressuring price points in high‑volume segments and expanding access in emerging markets.

Biosimilar specialists and niche biotech: These firms are targeting recombinant products and seeding the market with lower‑cost alternatives; their success will hinge on regulatory wins and clinician acceptance.

Generic launches: Late‑stage introductions of generic equivalents for widely used ovulation agents are accelerating cost competition and compressing entry barriers for new players focusing on volume markets.

Supply fragility: Regulatory updates highlighting shortages of certain gonadotropins underscore the systemic risk in biologics supply chains — a reality that raises the strategic value of redundant capacity and local fill‑finish options.

Policy interventions: Recent government‑backed initiatives seeking to influence IVF drug pricing and direct‑to‑consumer distribution are a material wildcard — forcing firms to develop flexible pricing and channel strategies.

Reassess portfolio sequencing: Prioritize programs where clinical differentiation, patent life, and pricing resilience align. For commoditizing oral agents, consider licensing or manufacturing partnerships rather than full commercial investment.

Invest selectively in biosimilars: Target biologics with the largest margin dilution risk and where manufacturing scale can be achieved with acceptable capital intensity. Use our sensitivity modelling to identify breakeven investment thresholds under different rebate and tender scenarios.

Harden supply resilience: Establish multi‑sourced raw material contracts, evaluate regional fill‑finish partnerships, and create strategic inventory buffers for key gonadotropins where shortages could disrupt clinic protocols.

Design flexible commercial models: Pilot alternative distribution channels, including DTC subscription models and clinic‑embedded services, while preparing payer value dossiers that emphasize cycle‑level economics and patient outcomes.

Pursue surgical M&A: Use the report’s M&A funnel to accelerate entry where organic timelines are too long — especially for biosimilar capabilities, niche biologics manufacturing, or distribution footholds in high‑growth markets.

Engage clinicians early: Invest in real‑world evidence programs and center of excellence partnerships to speed adoption of biosimilars and reassure clinicians about interchangeability and outcomes.

Board level: Use the report’s scenario suite to stress‑test budgets, capital allocation, and M&A appetite under alternative regulatory and pricing outcomes.

Commercial leadership: Leverage the playbooks and channel economics to redesign incentive plans, optimize launch sequencing, and run rapid pilots for DTC and clinic‑based models.

R&D & manufacturing: Apply the portfolio prioritization and risk map to gate decisions on biosimilar investment, capacity commitments, and technology transfers.

Corporate development: Use the curated M&A funnel and valuation templates to accelerate target screening and reduce time‑to‑deal certainty.

Our headline figures are derived from a bottom‑up aggregation of product‑level revenues, clinic adoption metrics, and payer reimbursement trends, reconciled to observed market behaviour from 2020–2025 and stress‑tested across multiple policy and supply scenarios for 2026–2032. The report intentionally balances disclosure and commercial sensitivity: we present comprehensive methodology, assumptions, and scenario outputs, but detailed subsegment tables and exact regional or application splits are reserved for the full report to protect proprietary modelling and to enable tailored client engagements.

The fertility drugs market is neither a slow‑moving legacy space nor a free‑for‑all commodity arena. It is a mid‑growth, highly concentrated market experiencing targeted disruption from generics and biosimilars, policy interventions, and supply shocks. For organizations that act decisively in 2026 — prioritizing surgical biosimilar investments, fortifying supply chains, and rethinking commercial models — there is a clear path to sustainable growth and margin preservation. PW Consulting’s Fertility Drugs Market report is designed to be the operational playbook that turns those strategic choices into measurable outcomes.

For access to the full dataset, subsegment tables, and the scenario modelling workbook referenced throughout this release, please visit the PW Consulting research portal and request the Fertility Drugs Market 2026 report package.

For detailed analysis of this topic, please visit the official page:Fertility Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com