Why Heat Exchangers Matter in Renewable Energy

Other |

2026-02-16 08:03:08

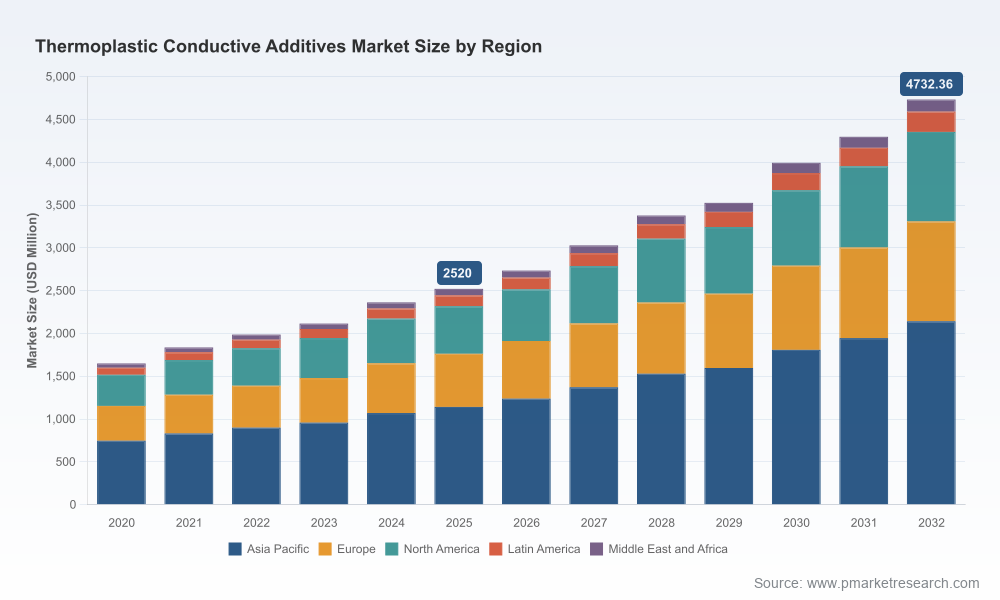

As electrification, miniaturization and increasingly stringent electromagnetic compatibility requirements reshape plastics design, the market for thermoplastic conductive additives is moving from niche engineering to industrial scale. PW Consulting’s latest market study — anchored on 2025 as the base year and projecting through 2032 — quantifies the change and translates it into decision-ready intelligence. Our analysis shows the total market expanding from USD 2,520 million in 2025 to roughly USD 4,732 million by 2032, representing a compound annual growth rate of approximately 9.42% over the 2026–2032 forecast window. This brief previews the strategic takeaways executives should act on in 2026 while preserving the detailed segment-level data for subscribers of the full report.

Thermoplastic Conductive Additives Market

Velocity of demand shift: Multiple end-markets (automotive electrification, consumer electronics miniaturization, industrial automation, and medical devices) are driving both volumetric growth and specification complexity for conductive thermoplastic solutions. The expansion is not only in volume but in performance differentiation: thermal management, EMI shielding, and controlled surface resistivity are now concurrent product requirements.

Thermoplastic Conductive Additives Market

Input cost and availability risks: Feedstock dynamics — from carbon black to next-generation nanotubes and graphene concentrates — are increasingly decisive for cost models and supplier strategies. Recent price moves and upstream capacity additions create both near-term cost pressure and mid-term opportunities for substitution or value capture.

Thermoplastic Conductive Additives Market

Competitive and regulatory inflection points: Market concentration and the rise of specialty nano-additive suppliers are altering the bargaining landscape. Simultaneously, regulatory reviews of legacy materials in some jurisdictions introduce compliance risk that must be modeled into procurement and product roadmaps.

Market sizing and validated forecast model — transparent methodology supporting multiple scenarios (base, constrained-supply, and substitution-led acceleration) with sensitivity levers executives can reuse in internal planning.

End-use needs matrix — a pragmatic mapping of electrical and thermal performance requirements by application class, with material selection heuristics and design trade-offs engineers can apply immediately.

Supply chain and raw-material risk dashboard — live-style indicators for carbon black, carbon nanotubes (CNTs), and graphene concentrates, including a short-term cost-impact matrix and recommended contractual structures to mitigate volatility.

Technology benchmark and formulation playbook — comparative guidance on carbon black, graphene, CNTs, metal-based fillers and inherently conductive polymers, including low-loading strategies and processability checkpoints for injection molding and extrusion.

Competitive intelligence pack — concise profiles and positioning insights for the leading manufacturers, compounders and specialist nanotube/graphene suppliers, with strategic scenarios for partnerships, licensing and competitive responses.

Commercial go-to-market templates — route-to-customer options (direct compounds, masterbatches, concentrates, and toll compounding), pricing playbooks and margin protection tactics tailored to different buyer archetypes.

M&A and partnership heatmaps — prioritized targets and rationales for tactical investments to secure technology or capacity, plus integration checklists focused on IP, supply continuity and regulatory exposure.

Regulatory and standards tracker — a practitioner’s summary of upcoming chemical evaluations and compliance implications, with recommended testing priorities and labeling strategies.

The competitive environment combines legacy materials suppliers, specialty compounders and emerging nano-additive specialists. Market concentration is meaningful but not prohibitive: the top three players account for a significant portion of the market footprint, and the top five players extend that reach further — a structure that favors scale while leaving room for technology-focused challengers.

Key strategic archetypes we observe:

Materials incumbents (broad portfolio, scale advantage): companies with deep carbon black and graphitic offerings are leveraging established channels into electronics, wire & cable and industrial applications. Their scale supports effective logistics and cost optimization for commodity and mid-performance grades.

Compounders and formulators (application integration, customization): specialized compound houses differentiate through formulation expertise and production footprints close to customers, enabling rapid prototyping and customized conductivity windows from static-dissipative to EMI shielding.

Nano-additive innovators (performance at low loadings): graphene and single-wall CNT providers enable conductivity with minimal impact on mechanical properties, opening new design possibilities. Their value is most acute in applications constrained by density, surface finish or high mechanical performance requirements.

Notable firms profiled in the full report are representative across these archetypes — from long-standing carbon black and graphite players to focused nanotube and graphene specialists — each with distinct routes to commercial adoption and different implications for prospective partners or acquirers.

Raw-material price movement and availability: North American carbon black prices have shown upward pressure recently; buyers should expect continued volatility tied to tire-industry demand, feedstock cycles and logistics. These cost dynamics can erode margins quickly if not hedged by contractual or product strategies.

Capacity expansions for advanced additives: Several companies are committing to scale-up of graphene and nanotube production and to broadening compounding capacity in strategic regions. These moves will compress premium spreads for low-loading conductive solutions and accelerate adoption in high-value applications.

Regulatory reviews and classification updates: A number of legacy carbon-based materials are scheduled for evaluation in relevant jurisdictions. Procurement and product teams must track timelines and ensure alternate formulations or compliance pathways are identified.

Productization trends: Expect a continued shift from commodity masterbatches to application-specific concentrates and pre-compounded thermoplastics that reduce integration complexity for OEMs. This raises the strategic value of compounding partners with localized production footprints.

Lock in material access with layered contracting: combine short-term spot flex with multi-year offtakes for critical feedstocks (carbon black, CNTs, graphene) to stabilize costs without forfeiting upside participation when prices normalize.

Invest in low-loading conductive solutions where design constraints exist: prioritize partnerships or licensing with nano-additive suppliers to deliver conductivity at lower filler volumes, preserving mechanical properties and reducing weight.

Build a modular product architecture: separate formulations for thermal vs. electrical requirements to reduce complexity and accelerate qualification across multiple OEM platforms.

Strengthen regional compounding capabilities: near-market compounding shortens lead times, reduces logistics risk and eases regulatory compliance; evaluate toll compounding or JV models as faster routes.

Formalize regulatory watch and testing protocols: assign cross-functional owners to scenarios where material classification changes could affect supply or product compliance.

Prioritize pilot programs with OEMs in high-growth pockets: targeted demonstrators for EV thermal management, EMI shielding in 5G-enabled devices, or lightweight conductive components in wearables create early pull-through.

Consider bolt-on acquisitions for capability gaps: prioritize targets that add differentiated conductive technology, localized compounding, or secure raw-material feeds with predictable pricing dynamics.

Model multiple revenue/margin scenarios: incorporate raw-material volatility, substitution pathways and regulatory shifts into planning tools to stress-test commercial strategies and capital plans.

PW Consulting combines market-grade forecasting with hands-on commercialization support. Our services for stakeholders in the thermoplastic conductive additives space include bespoke market and technology due diligence, supplier and price-risk modeling, M&A target screening and integration planning, go-to-market playbooks, and rapid prototyping roadmaps with compounder partners. We also deliver executable pilot programs that connect material innovation to OEM validation and scale-up.

This briefing is intentionally selective — designed to surface the strategic inflection points executives must address now. The full PW Consulting Thermoplastic Conductive Additives Market Report contains the granular segment breakdowns, regional and application-level forecasts, supplier scorecards, pricing sensitivity models and downloadable scenario workbooks required to operationalize the recommendations summarized here.

For access to the complete dataset, downloadable tools and a consultant-led briefing tailored to your organization, please request the full report from PW Consulting’s research team. Subscribers receive the detailed segment tables, CR3/CR5 context drilled to product families, and the reproducible forecast model suitable for board-level planning and procurement negotiations.

For detailed analysis of this topic, please visit the official page:Thermoplastic Conductive Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com