N-Methoxymethyl N-Trimethylsilylmethylbenzylamine Market — Strategic Imperatives for 2026

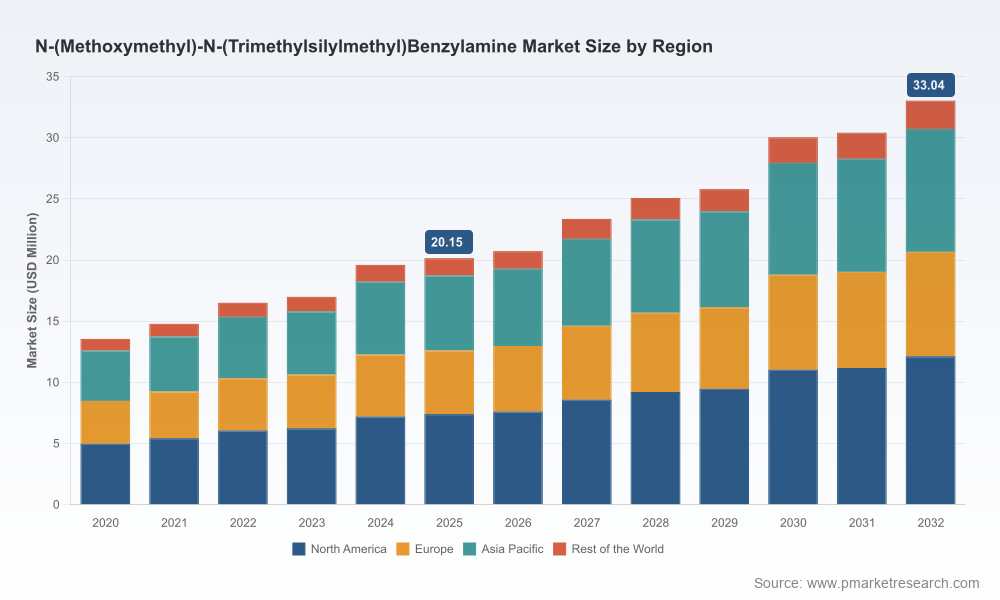

PW Consulting today releases a strategic preview of our forthcoming market study on N‑Methoxymethyl N‑Trimethylsilylmethylbenzylamine, a specialty organosilicon amine widely used as a reagent and building block in modern synthetic chemistry. Built on a 2025 base year with a historical backbone covering 2020–2025 and a forward-looking forecast to 2032, the study frames practical actions for procurement, R&D leaders, and corporate strategists entering 2026. At the macro level, the addressable market has expanded from the low‑teens (USD Million) in 2020 to just over USD 20 Million in 2025, and PW Consulting’s scenario-driven forecast anticipates continued expansion toward the low‑to‑mid tens of millions by 2032, implying a steady compound annual growth rate of 7.32% across the 2026–2032 horizon.

N Methoxymethyl N Trimethylsilylmethylbenzylamine Market

Why this specialty reagent matters to 2026 decision‑makers

This compound functions as a targeted reagent for the generation of non‑stabilized azomethine ylides—an essential intermediate for [3+2] cycloaddition reactions used in pyrrolidine and other heterocycle syntheses. Its primary role in research and synthesis (laboratory to small bulk) positions it at the intersection of medicinal chemistry, agrochemical discovery, and advanced methodology development. Several market realities make it strategically important for 2026:

N Methoxymethyl N Trimethylsilylmethylbenzylamine Market

- Concentrated application profile: The product is almost exclusively sold into synthesis and research workflows (not for direct therapeutic or household applications), which focuses demand among R&D organizations, CROs, and specialty API/intermediate manufacturers.

- Scale and purity economics: Commercial availability is typically at laboratory to small bulk scales and commonly offered in the mid‑90s purity range. That scale profile changes the commercial dynamics in favor of service, reliability, and technical support over raw price competition.

- Supply‑chain sensitivity: Upstream feedstocks (trimethylsilylmethyl derivatives and benzylamine precursors) and limited commodity‑scale production create supply tightness that translates into opportunity for differentiated service models, multi‑sourcing, and strategic inventory management.

What PW Consulting’s report delivers — operational, not academic

Our report is built for executives who must translate specialty chemical market intelligence into procurement, investment, and product strategy. Key deliverables include:

N Methoxymethyl N Trimethylsilylmethylbenzylamine Market

- Market sizing and validated forecasts with scenario analysis and sensitivity to R&D adoption rates and substitution risk.

- Supply‑chain maps that identify upstream feedstock bottlenecks, logistics constraints (including cold‑chain needs where relevant), and practical mitigation strategies.

- Supplier benchmarking and scorecards combining technical capability, compliance posture, catalog breadth, and delivery reliability.

- Commercial playbooks for buyers and sellers: contracting templates, quality acceptance protocols, qualification steps for secondary suppliers, and inventory guidelines tailored to gram‑to‑kilogram usage patterns.

- Pricing models that link raw material indices, batch economies, and purity grade premiums to expected list and net prices across forecast scenarios.

- Regulatory and IP checklists emphasizing permitted research‑use-only supply, use‑case restrictions, and labeling and documentation best practices.

- M&A and partnership candidate screening, with a practical rubric for evaluating small‑scale manufacturers and traders for bolt‑on acquisition or supply agreements.

- Fully interactive Excel models and raw data tables for client use, enabling custom scenario runs and procurement planning.

Macro dynamics steering the market through 2026

Several structural dynamics shape commercial patterns and merit attention from strategy teams:

- Demand driven by R&D intensity. Pharmaceutical discovery and method development in heterocycle chemistry remain primary growth engines. Investment cycles in small‑molecule discovery programs correlate strongly with reagent demand.

- Concentration with space for differentiation. The market displays moderate concentration: the top three suppliers account for a meaningful portion of commercial availability, and the top five further increase that share. This structure creates scope for both scale advantages among established players and niche opportunities for specialized suppliers.

- Specialty supply reality. This reagent is not produced at commodity volumes and there are no widely reported large‑scale capacity expansions. As a result, lead times, secondary supplier qualification, and technical service are decisive procurement criteria.

- Purity segmentation matters. Buyers trade off cost and performance across purity bands—mid‑90s purity is the norm. Purity, packaging, and handling (including cold‑chain where offered) are common negotiation levers.

- Regulatory clarity. The product is marketed strictly for research and synthesis use; that delimitation reduces some downstream regulatory complexity but raises the importance of correctly scoped use agreements and supplier certifications.

Competitive landscape — strategic profiles and implications

Our supplier review synthesizes public catalog data and proprietary validation work to create a practical view of market positioning and routes to partnership:

- Merck KGaA (Sigma‑Aldrich) — Global brand strength, a broad reagent catalog, and deep compliance infrastructure make it the default partner for life‑science labs seeking catalog reliability and documented provenance. Their offering emphasizes research chemical formats used in mainstream organic synthesis workflows.

- Thermo Fisher Scientific (Thermo Scientific Chemicals / Acros Organics / Alfa Aesar) — Distribution reach through Fisher channels provides unmatched accessibility for multi‑site organizations. Their catalogue strategy and channel integration support large institutional procurement but can be costlier at scale without negotiated terms.

- Specialty and regional suppliers (Oakwood Chemical, Enamine, BLD Pharm, Biosynth, Arborpharm, Otto Chemie, and multiple Indian manufacturers/traders) — These suppliers create options on service, custom synthesis, and regional proximity. Enamine’s positioning as a building‑block provider and Biosynth’s capacity to supply larger small‑bulk packs illustrate alternative go‑to‑market models focused on speed and customizability. Some players emphasize cold‑chain logistics and global stocking to reduce lead times for R&D customers.

For strategists, the implications are twofold: established global players provide compliance and catalog continuity while smaller, agile suppliers offer customization and batch scale flexibility. The market’s current concentration profile implies that partnerships with the right mix of global reach and local agility will determine secure supply in 2026.

Practical plays for buyers and suppliers in 2026

We recommend concrete, prioritized actions that can be executed with the intelligence in our full report:

- Buyers: implement a two‑tier sourcing strategy—secure a primary supplier for compliance and volume assurance while qualifying two secondary suppliers for technical backup and price competition. Translate reagent specifications into clause‑based acceptance criteria to reduce batch‑to‑batch variability risk.

- Buyers: lock in contingency inventory policies sized to typical project cycles (laboratory to kilogram) and link those policies to milestone releases in R&D programs to avoid overstocks.

- Suppliers: move up the value chain by bundling technical support, custom batch services, and regulatory documentation. Investment in small‑scale custom synthesis capability and digital cataloging will win repeat institutional buyers.

- Both sides: negotiate quality and continuity clauses (including substitution and change‑control protocols) to manage feedstock volatility and purity differentials that materially affect reaction outcomes.

- Investors: look for bolt‑on assets that add small‑bulk scale, regulatory documentation capability, or regional distribution hubs to existing portfolios; the market structure favors acquisitions that consolidate specialized capacity or create secure distribution channels.

Scenario signals and KPIs to watch in 2026

PW Consulting’s scenarios map a base case aligned with the 7.32% CAGR, an upside driven by accelerated adoption in targeted heterocycle programs, and a downside triggered by substitution or regional regulatory friction. Track these near‑term signals to validate scenarios:

- Announcements of capacity expansions or new commercial scale facilities (none widely reported at the time of this preview).

- Changes in upstream feedstock pricing and availability for trimethylsilylmethyl derivatives and benzylamine precursors.

- Order lead times and backorder frequency across major catalog suppliers; increasing backorders are an early indicator of structural tightness.

- Procurement wins by alternative reagents in standard protocols; a measurable substitution trend would compress growth assumptions.

- R&D hiring and project counts in pharmaceutical discovery groups working on pyrrolidine and related heterocycles.

How to extract immediate value from our research

The full PW Consulting report converts the above narrative into operational tools: granular demand and price models, supplier scorecards with audit checklists, a regulatory and labeling compendium, and downloadable Excel workbooks for bespoke scenario testing. We intentionally keep this release a strategic “trailer” — the detailed regional splits, application breakdowns, and supplier share tables that underpin procurement negotiation and M&A diligence are available only in the complete study and datasets.

For procurement directors, R&D leads, and corporate strategy teams preparing budgets and sourcing plans for 2026, the decisions you make in the next 6–12 months will determine your exposure to supply continuity risk and your ability to capture upside if reagent‑led workflows accelerate. PW Consulting’s study synthesizes the hard numbers, supplier realities, and executable playbooks you need to move from risk awareness to commercial action.

To access the full report, the interactive models, and supplier scorecards that contain the granular segmentation and data tables referenced in this preview, please visit the PW Consulting publication page for the N‑Methoxymethyl N‑Trimethylsilylmethylbenzylamine Market study.

For detailed analysis of this topic, please visit the official page:N Methoxymethyl N Trimethylsilylmethylbenzylamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com