Carbon Fiber Sports Equipment Market: Strategic Imperatives for 2026 — PW Consulting Insights

As global demand for performance-driven sporting goods intensifies, carbon fiber has moved from a premium differentiator to a core material strategy for leading equipment manufacturers. PW Consulting’s latest market study — covering historical performance through 2025 and a seven‑year forecast period beginning in 2026 — frames the strategic options that will determine winners and laggards in the coming cycle. This briefing summarizes the report’s high‑value, decision‑ready takeaways for 2026 while preserving the report’s proprietary segment detail for subscribing clients.

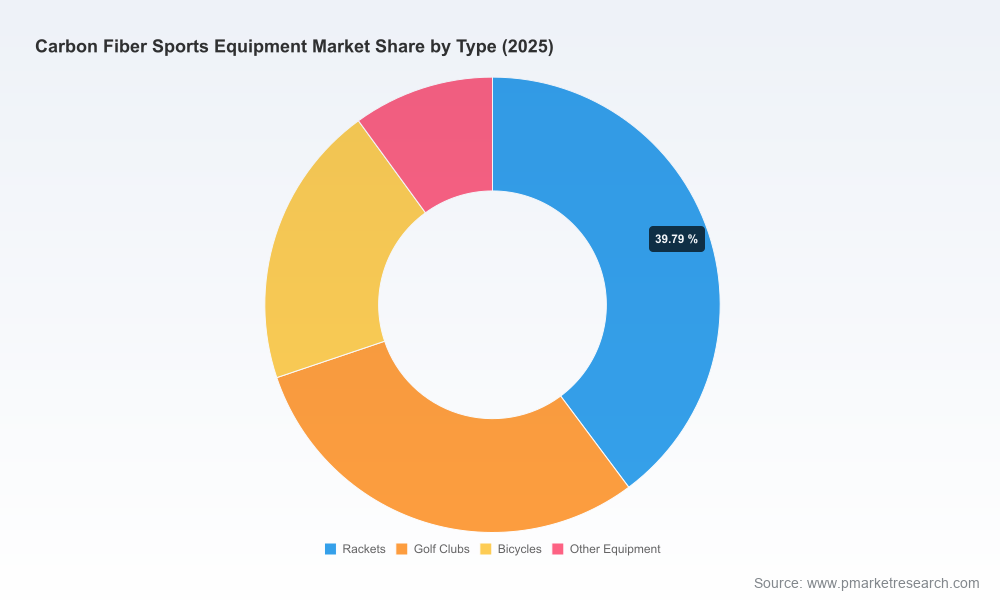

Carbon Fiber Sports Equipment Market

Market Snapshot

After a steady upward trajectory from 2020, the global carbon fiber sports equipment market reached an estimated USD 5,500 million (base year 2025). Our model projects a compound annual growth rate of 6.5% over the 2026–2032 forecast window, reflecting structural demand for lighter, stronger sporting goods and continued product premiumization. At the overall market level, this growth trajectory implies a material expansion of opportunity for manufacturers, material suppliers and aftermarket service providers, but it also amplifies operational, supply‑chain and regulatory pressures that require proactive management.

Carbon Fiber Sports Equipment Market

What’s Driving Growth — and Where Leaders Will Focus

- Performance and weight optimization: Athletes and serious amateurs continue to price lightweight, stiffness and tuned mechanical responses above cost, pushing designers to exploit carbon fiber’s property set across rackets, clubs, frames and skis.

- Consumer premiumization and diversification: Expanded product tiers and the spreading of carbon fiber into formerly metal/plastic‑dominated categories sustain ASPs and create higher margin segments for brand owners.

- Material and process innovation: New fiber architectures (e.g., boron‑modified hybrids), prepreg chemistries and automated layup are lowering production variability and enabling new performance envelopes.

- Raw‑material dynamics: Polyacrylonitrile (PAN) precursor pricing and availability remain the primary cost lever — standard modulus PAN prices have recently been observed in a band roughly between USD 12–20 per kg — and fluctuations here directly influence finished‑goods economics and pricing strategies.

- Regulation and circularity: Growing attention to end‑of‑life composite recycling (notable industry projects and regulatory focus) is shifting buyer expectations toward sustainable materials and recovery pathways — an emerging commercial and reputational battleground.

Competitive Landscape — patterns and positioning

The market remains moderately fragmented: leadership is shared between global fiber suppliers and vertically integrated OEMs, with the top industrial suppliers controlling a meaningful but not dominant portion of market value. This structure favors both supplier‑OEM partnerships and targeted consolidation plays.

Carbon Fiber Sports Equipment Market

- Material champions: Toray Industries, Teijin Limited and Mitsubishi Chemical remain central to high‑performance supply chains, advancing fiber grades and prepregs while positioning sustainability credentials (e.g., bio‑circular certs) as a commercial differentiator.

- Advanced composites specialists: Hexcel and SGL Carbon supply aerospace‑grade competencies that are increasingly applied to high‑end sports segments where tolerances and performance ceilings justify premium materials and processes.

- Brand and OEM strategies: Product innovators such as HEAD, Wilson, Babolat, Trek and Giant blend in‑house engineering and supplier co‑development to own the consumer experience. Recent product activity — from HEAD’s boron‑carbon Hy‑Bor racket updates to OEM collaborations integrating smart technology — underlines the importance of rapid product cycle innovation.

- Cross‑sector technology flows: Expect continued transfer of process and material advances from aerospace and automotive composites into sport; suppliers with multi‑sector footprints are advantaged in cost amortization and scale.

Notable recent milestones that underscore strategic direction: HEAD’s March 2026 rollout of Hy‑Bor racket technology, Toray’s recognition for ISCC PLUS bio‑circular prepregs in late 2025, and OEM partnerships for smart integration pursued through 2025. Together these moves signal where R&D investments are concentrating — performance per weight, sustainability claims verified by independent schemes, and an adjacent push toward electronics and software integration.

Strategic Imperatives for 2026 Decision‑Makers

For executives setting strategy in 2026, the following imperatives should guide capital allocation, product roadmaps and commercial models:

- Lock in material optionality: Secure multi‑tier supplier relationships for PAN and finished fiber; structure contracts with flexibility for grade mix and volume ramps. Consider upstream partnerships or minority investments in precursor production where supply tightness materially threatens go‑to‑market timing.

- Monetize sustainability: Pilot certified bio‑circular prepregs and clearly communicate cradle‑to‑grave metrics. Early movers that can demonstrate verifiable recycling pathways will gain retail and institutional access in regulated markets.

- Invest in manufacturability and automation: Reduce variability and per‑unit cycle time through automated layup, modular tooling and digital process control — investments that compress time‑to‑spec and protect margin as volumes scale.

- Partner on differentiated tech: Co‑develop material stacks and electronics integration with fiber suppliers and software firms to create defensible product features rather than competing exclusively on price.

- Adopt scenario‑based pricing and hedging: Build price models tied to precursor inputs and set threshold triggers for contracting, promotions and SKU positioning to absorb short‑term raw‑material swings without eroding brand equity.

- Evaluate focused M&A: Target acquisitions that supply either unique materials, in‑house weave/manufacturing capabilities, or circularity tech — not for scale alone but to fill strategic capability gaps that are hard to replicate organically.

Scenarios to Stress‑Test Investment Choices

Our forecast assumes a base CAGR of 6.5% through 2032. Boards should stress‑test three plausible scenarios when sizing investments and M&A:

- Base case (moderate growth): Continued premiumization and steady adoption. Priorities: secure supply, scale premium SKUs, invest in manufacturability and sustainability pilots.

- Upside (accelerated adoption): Faster consumer migration to carbon across more categories, driven by successful marketing and tech integration. Priorities: expand capacity, accelerate product launches and lock channel exclusives.

- Downside (input shock/regulatory constraint): Sharp PAN cost spikes or restrictive EOL rules without recycling infrastructure. Priorities: activate mitigation playbook — material substitution, dynamic pricing, and shared industry recycling investments.

Operational Playbook — near‑term actions (90–360 days)

- Run supplier stress tests: evaluate dual‑sourcing and lead‑time reduction plans for precursors and prepregs.

- Launch 1–2 branded sustainability pilots tied to certified prepregs or reclaimed fiber, with clear KPIs for cost, performance and consumer response.

- Initiate cross‑functional “composites war‑room” to align R&D, procurement, operations and commercial teams around material choices and SKU rationalization.

- Define an M&A screening funnel focused on capability, IP and channel control rather than pure capacity—prioritize assets that shorten time‑to‑market for differentiated products.

What PW Consulting’s Full Report Delivers

- Proprietary market sizing and a transparent forecasting model (2020–2032) calibrated to demand drivers and cost inputs.

- Supplier and OEM competitive profiles with strategic diagnostics and deal heatmaps.

- Price and cost models linking PAN precursor dynamics to finished‑goods margins.

- Technology and patent landscaping highlighting disruptive material architectures and process innovations.

- Sustainability and circularity assessment, including regulatory risk mapping and viable recovery business models.

- A practical go‑to‑market playbook with prioritized initiatives, KPIs and 12–36 month investment timelines.

- M&A screening criteria, integration checklists and illustrative synergies tailored for strategic and financial buyers.

To preserve the report’s value for corporate decision‑makers, we have intentionally kept this briefing at the macro level. Detailed segment and regional splits, discrete pricing schedules and the full dataset that supports scenario sensitivity are included only in the full PW Consulting report and interactive dataset.

Conclusion — The Decision Window for 2026

2026 presents a critical window for manufacturers, material suppliers and investors: seize supply optionality, embed sustainability into value propositions, and convert material science advantages into product and service revenue streams. Players that align procurement, R&D and commercial models around carbon fiber’s cost and performance vectors — while actively managing circularity obligations — will sustain premium positioning as the market expands.

PW Consulting’s Carbon Fiber Sports Equipment Market report is designed to be an operational companion for that journey: robust enough to guide boardroom trade‑offs, and detailed enough to underpin execution plans. For access to the full dataset, granular segmentation and bespoke advisory engagements, visit the PW Consulting report page to download the complete study and to request a tailored briefing for your executive team.

For detailed analysis of this topic, please visit the official page:Carbon Fiber Sports Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com