PW Consulting: Renewable Energy Consultancy Services Market Research — A Strategic Playbook for 2026 Decision-Makers

As energy transition complexity accelerates, corporate leaders and investors must convert strategic intent into executable programs with surgical precision. PW Consulting’s new Renewable Energy Consultancy Service Market Research (base year: 2025) is designed to do exactly that: translate market dynamics into operational roadmaps for 2026 and beyond. Built on a multi-year historical lens and a 2026–2032 forecast horizon, the study quantifies the industry’s scale and trajectory while delivering field-tested tools for execution. To preview the report’s strategic value, this release highlights the high-level, data-driven signals and the practical frameworks contained within — while intentionally withholding granular sub-segmentation tables to encourage direct access to the full dataset and appendices.

Renewable Energy Consultancy Service Market Research

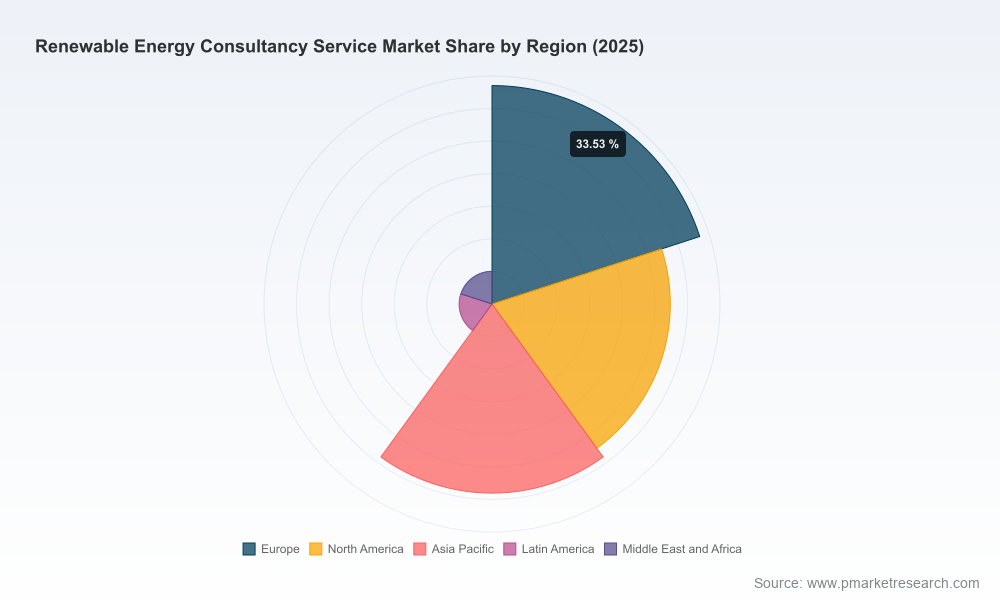

Topline market signal: growth, scale and concentration

The consultancy market supporting renewable energy projects reached an estimated USD 17,286.5 million in 2025 and is projected to grow at a compounded annual growth rate (CAGR) of 10.41% through the 2026–2032 forecast window. By the close of the forecast period, the market is expected to exceed USD 34,500 million (USD million basis). This trajectory reflects sustained demand for advisory across project development, grid integration, policy navigation, and emerging value pools such as green hydrogen and integrated solar-plus-storage solutions.

Renewable Energy Consultancy Service Market Research

Market concentration remains low by professional services standards: the top three firms account for under one-fifth of the market, and the top five for less than one-third. That fragmentation creates distinct opportunities for specialist boutiques, regional integrators and tech-enabled firms to capture meaningful share through capability differentiation or targeted M&A.

Renewable Energy Consultancy Service Market Research

Why 2026 is an inflection year — and what it means for strategy

- Regulatory inflections: New compliance regimes — including supply-chain restrictions entering force for projects that break ground in 2026 — are reshaping eligibility for tax credits and incentives. Advisory teams must now couple transaction support with supply-chain safe‑harbor strategies and compliance playbooks.

- Commercial realignment: Policy shifts in 2025 altered subsidy stacks and forced portfolio reprioritization across wind, solar and storage projects. Advisors are being asked to re-scope M&A diligence, re-price risk, and re-align client investment timelines.

- Hyperscaler demand: Large-scale corporate buyers and hyperscalers drove a step-change in clean energy procurement via PPAs and hybrid structures during 2025. These buyers demand integrated solutions combining generation, storage, grid services and sophisticated offtake arrangements.

- Grid and technical complexity: Accelerated electrification and the rapid build-out of variable renewables have increased the need for grid-connection engineering, flexibility services and storage integration — specialties that remain labor- and expertise‑intensive.

- M&A and platform plays: Policy-driven delays in some capacity additions paradoxically spurred M&A in managed platforms, contracted asset portfolios and scale-build capabilities — creating a fertile environment for advisers that can synthesize technical, commercial and regulatory due diligence.

What PW Consulting’s report delivers (practical, execution-oriented)

This study is structured as a practitioner’s dossier rather than an academic treatise. Key deliverables include:

- Macro market sizing and scenario-based forecasts (2020–2032) on an USD million basis, with transparent methodology and sensitivity testing.

- Decision frameworks to sequence actions across strategy, M&A, project-financing, and operations — tailored to developers, utilities, corporates and investors.

- Comprehensive risk matrices for supply‑chain compliance, permitting and tax-credit exposure, including playbooks for navigating newly effective FEOC-style rules and recent tax-code changes.

- Technical due-diligence templates and checklists for grid connection, interconnection risk, construction management, and operations & maintenance readiness.

- Commercial model libraries: PPA structures, hybrid contracts, merchant vs contracted optimization, and pricing mechanisms adaptable to client risk appetite.

- Implementation toolkits: vendor assessment scorecards, procurement RFP templates, and staffing models to quantify the trade-off between in-house capability building and partnerships.

- Scenario modeling and dashboards that stress-test portfolios against policy shocks, commodity price shifts, and grid-constraint scenarios.

Note: The report contains granular breakdowns by region, service type and energy source in the appendices; these detailed tables and percentage splits are intentionally omitted from this preview to preserve the report’s exclusive value.

Data-driven strategic implications for 2026

- Scale favors integrators with cross-disciplinary delivery: Given the compound growth trajectory and low concentration, firms that combine technical engineering, regulatory counsel and financial structuring outperform siloed competitors.

- Specialized human capital is a strategic bottleneck: Technical due diligence, grid connection engineering, and regulatory compliance are labor-intensive cost drivers. Firms should prioritize scalable people-and-tools models — for example, blended teams augmented by digital checklists and modular templates to reduce billable-hour exposure.

- Compliance-ready supply-chain strategies are now table stakes: Advisers must offer not only compliance assessment but executable safe‑harbor remedies (recontracting, alternative sourcing, restart timelines) to secure client tax credit eligibility.

- Flexibility and storage expertise unlock value: Integration of storage and demand-side services changes asset economics; advisors who monetize flexibility for clients (via market products or bilateral contracts) will capture incremental fees and recurring revenue.

- M&A pathways are accelerated but selective: The market’s fragmentation invites roll-up and capability consolidation, yet successful deals hinge on rapid post-merger integration of technical teams and data platforms.

Competitive landscape — where incumbents and challengers stand

The market’s leading global consultancies remain active, but no single firm dominates across all capability vectors. High-level positioning observed in our analysis:

- McKinsey & Company and BCG: Strategic advisory leaders on net-zero pathways, portfolio optimization and large-scale scenario modeling. Their strength is in cross-sector strategy and executive-level transformation programs.

- Accenture: Distinguished by technology-enabled delivery — smart grids, digital trading platforms and AI/IoT integrations that bridge advisory and implementation at scale.

- PwC and EY: Deep in transaction advisory, regulatory compliance and reporting — critical for clients pursuing M&A, refinancing, and sustainability disclosure obligations.

- DNV, WSP and SLR Consulting: Technical-engineering heavyweights. Recent acquisitions and client engagements illustrate their push to become one-stop shops for grid-connection engineering, due diligence, and project delivery.

- Wood Mackenzie and Guidehouse: Market intelligence and forecasting specialists who provide essential market signals for investment committees and deal teams.

- Boutiques and specialists (Baringa, PA Consulting, ICF, ERM): Play to their strengths in regulatory change advisory, offshore wind, hydrogen ecosystems, and environmental compliance — often partnering with larger firms for integrated bids.

Recent market moves underscore the trend toward capability aggregation. Notable examples include technical centers of excellence created through strategic acquisitions and enlarged Power & Energy offerings after select M&A completions. These moves tighten competition in grid-related advisory while opening white-space opportunities in environmental, permitting and hydrogen advisory niches.

Actionable recommendations for corporate decision-makers in 2026

- Re-assess portfolio timing and eligibility: Immediately model how supply‑chain and tax-credit rule changes affect project IRRs and refinancing options; prioritize projects with clear compliance pathways.

- Balance build-versus-buy on advisory capability: For repeatable needs (PPAs, interconnection studies), invest in internal playbooks and small centralized teams; for one-off strategic transactions, engage specialized advisers with proven delivery track records.

- Embed flexibility into procurement: Negotiate PPA and offtake clauses that address curtailment, storage dispatch and capacity revenue stacks to protect value during grid stress events.

- Prioritize strategic M&A only with integration plans: Target acquisitions that fill capability gaps (grid engineering, environmental permitting, hydrogen) and include early integration of people and data systems.

- Invest in digital tooling: Scenario-model libraries, automated DD checklists, and cloud-based collaboration platforms materially reduce transaction timelines and professional costs.

How the PW Consulting report supports execution

Beyond market sizing, the report is a playbook. It includes downloadable templates, vendor-selection frameworks, and scenario models ready to plug into corporate finance and project-development processes. For executive teams, the study provides prioritized roadmaps anchored to near-term decision gates for 2026 — the moments when portfolio decisions, financing structures and procurement strategies will be set.

We have intentionally presented a high-level, action-focused preview here. The full report contains the complete regional and service-type breakdowns, granular revenue splits, firm-level benchmarking, and appendices with source data and modeling assumptions. Those detailed tables are essential for execution and are available in the full PW Consulting report package.

Next steps

For corporate strategy teams, investor groups, and advisory firms preparing 2026 plans, the report is designed as a working manual — not just a reference. To access the full dataset, proprietary benchmarking, and downloadable implementation toolkits, please consult PW Consulting’s Renewable Energy Consultancy Service Market Research page or contact your PW Consulting representative. Our team stands ready to brief boards, underwrite due diligence, and co-author implementation roadmaps tailored to your asset and market exposures.

PW Consulting — translating market scale and growth into executable advantage for the energy transition.

For detailed analysis of this topic, please visit the official page:Renewable Energy Consultancy Service Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com