Process Automation and Instrumentation Market Growth Drivers 2026: Shaping Industrial Efficiency

Other |

2026-02-03 11:18:53

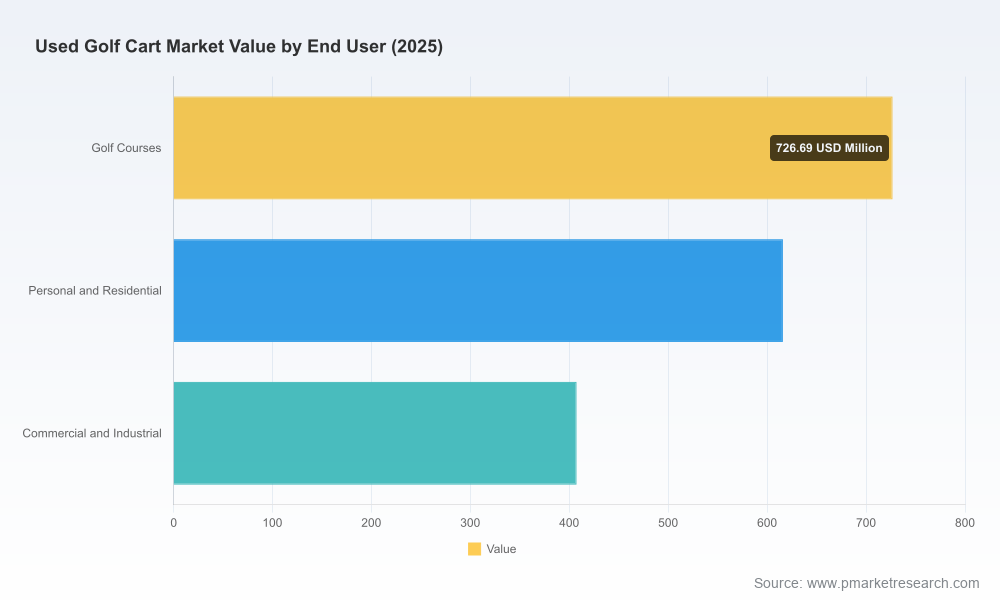

PW Consulting’s latest market intelligence brief on the used golf cart market frames 2026 as a pivotal planning year. With the secondary market already sized at approximately USD 1.75 billion in our 2025 base year and a steady mid-single-digit compound annual growth rate projected through 2032 (our model uses a 6.25% CAGR for the 2026–2032 forecast window), executives face an environment where technology, regulation, and channel economics are reshaping residual value, remarketing velocity, and total cost of ownership. This release is a concise executive preview of the report’s strategic value — showcasing our analytical depth and practical frameworks while preserving the granular segmentation tables and proprietary spreadsheets that accompany the full study.

Used Golf Cart Market

Transition decisions — retrofit vs. replacement, lithium BMS integration, and warranty exposure — dominate CapEx and Opex trade-offs. Our TCO models show that lifecycle planning for battery assets is now the most material driver of remarketed unit economics. Practical implication: adopt asset-level battery health monitoring and standardized end-of-life workflows to avoid sudden write-downs.

Used Golf Cart Market

Compliance is now operational rather than strategic. Firms that embed UL-standard safety testing, EU battery compliance, and air-transport SoC controls into their logistics stack reduce friction when accessing higher-value markets. We recommend a compliance scorecard that maps certification status to channel eligibility.

Used Golf Cart Market

OEMs and large dealers are investing in standardized refurbishment lines, documented part-replacement rules, and digital provenance records. For operators, the choice is clear: invest to create a repeatable refurbishment SOP, or partner with certified providers to preserve margin and brand integrity.

Inventory velocity is diverging across channels — direct OEM CPO, dealer lot sales, fleet auctions, and peer-to-peer marketplaces each carry different margin and reconditioning profiles. Our pricing framework lets you stress-test remarketing outcomes under different inventory aging and certification scenarios.

Unit-level telematics, service history, and certified battery health metrics are rapidly becoming the inputs for automated residual-value models. Firms that standardize data capture and integrate valuation analytics into procurement and remarketing will outpace peers in capture of upside.

The competitive set is bifurcating into two broad approaches: (1) OEM-led standardization and vertically integrated CPO programs; and (2) nimble independent refurbishers and EV-specialist brands focusing on rapid, price-sensitive channels. Our analysis highlights how leading manufacturers and EV entrants are positioning themselves.

Recent corporate actions typify these dynamics: several OEMs updated CPO programs in 2025–2026 to expand lithium offerings and to add street-legal low-speed vehicle (LSV) variants into certified inventory; others rolled model-year updates into refurbishment eligibility. These developments accelerate the pace at which pre-owned fleets are technologized and monetized.

Our full report is structured as an operational guide for 2026 planning cycles. Highlights include:

Importantly, the report preserves the detailed segmentation tables, regional allocations, and unit-level valuation curves for premium subscribers — consistent with our “trailer” approach to executive intelligence.

We offer rapid executive briefings, bespoke scenario modeling, and hands-on workshop facilitation to translate these findings into boardroom-ready decisions. Clients engaging our advisory teams receive template playbooks, the full forecast spreadsheet with sensitivity toggles, and a tailored channel optimization roadmap aligned to their fleet size and geographic exposure.

The preview above demonstrates the report’s analytical backbone and operational focus while intentionally withholding the granular regional and end-use breakouts that underpin the full valuation engine. For teams making budgetary allocations, M&A decisions, or platform investments in 2026, those granular inputs are the difference between a good strategy and a defensible one.

To access the full report, detailed segmentation tables, and to schedule an executive briefing with PW Consulting’s Used Golf Cart Market practice, please visit the PW Consulting publications page or contact our industry desk. Limited slots are available for hands-on roadmap sessions ahead of Q3 planning cycles.

For detailed analysis of this topic, please visit the official page:Used Golf Cart Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com