The Strategic Rise of Deep Tech Market 2033

Networking |

2026-04-10 05:28:12

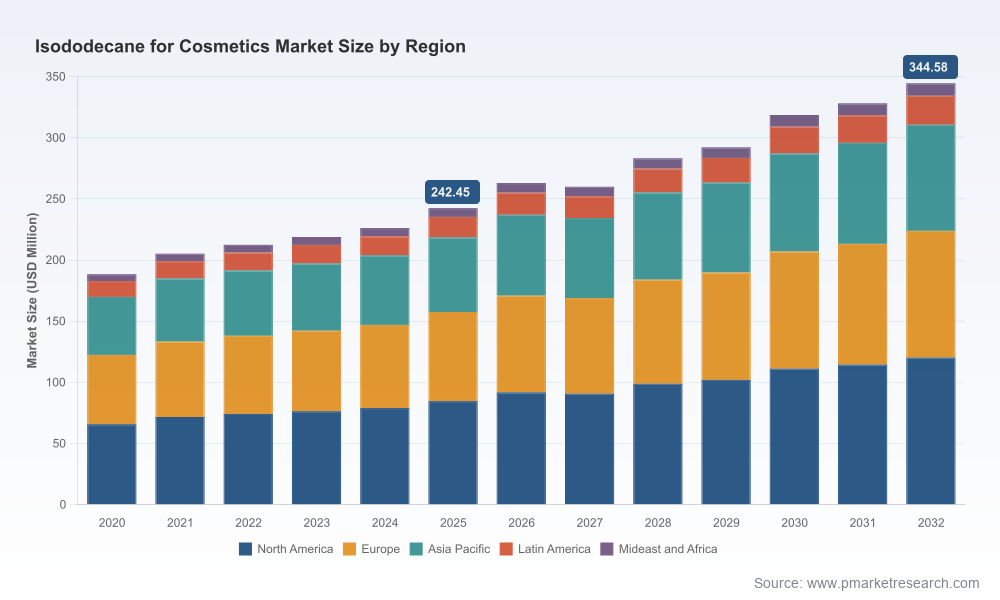

PW Consulting presents an executive briefing synthesizing the strategic implications from our new Isododecane For Cosmetics Market report (base year 2025, historical coverage 2020–2025, forecast period 2026–2032). This advisory is written for senior executives, corporate strategy teams, and investors who must make decisive 2026 allocations across R&D, sourcing, commercial strategy, and M&A. Our analysis combines granular supply‑side technical assessment with market economics to translate a projected compound annual growth rate (CAGR) of 5.14% into concrete actions. The total market reached approximately USD 242.45 Million in 2025 and is forecasted to expand materially through the 2026–2032 window.

Isododecane For Cosmetics Market

Strategic timing: 2026 sits at an inflection point where input‑cost volatility, regulatory pressure on petroleum‑derived chemistries, and a surge of formulation alternatives converge. The market’s steady mid-single‑digit CAGR masks important structural change that will determine winners and laggards over the next planning cycle.

Isododecane For Cosmetics Market

Decision readiness: Executives require not just market sizing, but executable gateways — supplier scorecards, plant‑level cost models, and scenario playbooks that map to three plausible feedstock and regulatory outcomes in 2026. Our report supplies those artifacts in ready‑to‑use form.

Isododecane For Cosmetics Market

Concentration and competitive dynamics: The market exhibits moderate concentration (CR3 ~58.4%, CR5 ~71.15%), indicating dominant incumbents control meaningful capacity but substantial room exists for targeted entrants and vertical integration plays.

Feedstock and cost pressure: Isododecane production remains tied to petroleum feedstocks (naphtha, isobutene routes). Strengthening naphtha prices observed in late Q4 2025 elevated manufacturing costs, compressing margins for producers exposed to spot feedstock. Companies with integrated upstream access or contractual indexation have already shown measurable resilience.

Regulatory intensity: Petroleum‑derived isododecane is drawing heightened scrutiny as regulators sharpen focus on volatile organic compounds (VOCs) and fossil‑origin materials in personal care. Compliance frameworks — including REACH obligations in Europe and evolving North American requirements — are becoming operational constraints rather than theoretical risks.

Technology and substitution pressure: Brands are actively seeking silicone alternatives and cleaner label ingredients. High‑purity synthetic isoparaffins remain valued for their sensory profile and solvency, but traction for bio‑based analogues is accelerating. The balance between performance, cost and sustainability claims will be decisive for formulation choices in 2026.

Value chain fragility and opportunities: The supply base combines large multinational producers and specialist suppliers. This creates pathways for contract optimization, strategic partnerships with household and indie brands, and bolt‑on acquisitions to secure differentiated grades or localized manufacturing capability.

Molecular specificity: Production centers on highly branched C12 isoparaffins (notably the pentamethylheptane isomer family). This technical specificity matters: small changes in isomer distribution materially affect sensory attributes, evaporation profile, and regulatory classification outcomes.

Our competitive profiling examines both scale players and specialty suppliers. Firms we highlight include INEOS Oligomers, Lanxess, MakingCosmetics Inc., Haltermann Carless, and Sojitz Solvadis. Each occupies a distinct strategic niche:

INEOS Oligomers (United States) — advantage: scale and high‑purity synthetic C12 capabilities that support large‑brand supply contracts and regulatory compliance documentation. Watch for contract pricing moves and capacity redeployment.

Lanxess (Germany) — advantage: a branded personal‑care offering positioned as a silicone alternative with formulation support for color cosmetics and hair care. Their route to market emphasizes technical service and co‑development.

MakingCosmetics Inc. (United States) — advantage: regulatory registration and customer proximity for smaller CPGs and indie brands. Their business model underscores agility and small‑lot supply, a strategic complement to larger producers.

Haltermann Carless (Germany) — advantage: established hydrocarbon production expertise and portfolio depth for formulators requiring specific evaporation and sensory profiles.

Sojitz Solvadis (Germany) — advantage: an established supplier to personal‑care channels with emphasis on product consistency and logistics solutions.

Collectively, these players demonstrate that the market is not winner‑take‑all; rather, differentiated technical capabilities, regulatory readiness, and close brand partnerships will decide who captures premium margins in 2026.

The PW Consulting report is structured for immediate operational use and boardroom decision support. Key deliverables include:

Market sizing & demand scenarios: base, upside, and downside forecasts through 2032 with sensitivity to feedstock and regulatory shocks.

Supplier scorecards: plant‑level cost models, capacity maps, lead‑time matrices and credit/contract risk assessments.

Price & margin model: transparent build‑up from feedstock to delivered cost, including freight, tolling, and VOC compliance costs.

Regulatory playbook: step‑by‑step REACH readiness, VOC mitigation options, and labeling strategies for the EU and North America.

Product & formulation radar: technical comparison of petroleum‑derived versus bio‑based IDD analogues and silicone substitutes, with guidance on trade-offs in sensory performance and shelf‑life.

Go‑to‑market templates: commercial pricing corridors, channel strategies for indie vs. mass brands, and a partner selection framework.

M&A and partnership blueprints: target criteria, valuation drivers and integration checklists focused on securing specialty grades or green‑feedstock capability.

Decision dashboards: interactive KPIs for procurement, R&D, and sales teams designed for a 2026 playbook.

For executive teams preparing budgets and strategic plans in 2026, our priority recommendations are:

Hedge and diversify feedstock exposure — move beyond simple spot purchases. Secure a mix of indexed contracts, strategic tolling agreements, and, where viable, back‑integrated feedstock access to mitigate naphtha volatility.

Invest in regulatory readiness — build or acquire dossiers, invest in emissions‑reducing manufacturing upgrades, and establish certification pathways for bio‑based alternatives where premium pricing is achievable.

Prioritize product differentiation — fund modest but focused formulation work to develop proprietary grades (evaporation profiles, sensory attributes) as a defensible margin booster against commodity pricing pressure.

Pursue targeted M&A or partnerships — prioritize bolt‑ons that deliver specialty grades, regional fill‑and‑pack capabilities, or bio‑feedstock experience rather than scale alone.

Adopt a segmented commercial playbook — differentiate pricing and service models for industrial formulators, multinational brands, and indie cosmetic houses to capture value across channels.

Run scenario planning exercises — stress‑test your 2026 P&L against at least three realistic outcomes (sustained high feedstock costs, tightening VOC regulation, rapid adoption of bio‑based alternatives) and identify trigger points for tactical pivots.

Our team offers targeted support to translate the report into results in 2026:

Custom procurement optimization (contract renegotiation playbooks and indexation modeling).

Regulatory dossier preparation and VOC mitigation program design.

Commercial segmentation and pricing implementation with A/B testing protocols for launch campaigns.

Due diligence and post‑merger integration protocols for acquisitions focused on specialty hydrocarbon chemistry or bio‑feedstock capacity.

This briefing intentionally highlights the strategic contours and decision‑relevant signals without reproducing the full set of proprietary split‑level data contained in our report. To access comprehensive region‑by‑region and application‑by‑application breakdowns, granular company shares, price decks, and the interactive decision dashboards, visit the PW Consulting report page or contact our industry team to schedule a bespoke executive briefing and scenario workshop. The full dataset and models are essential for precise budgeting and contract negotiation in 2026; consider the report the operational manual for turning market insight into margin.

In a market that is steady in headline growth yet unsettled beneath the surface, 2026 will reward firms that combine disciplined procurement, regulatory foresight, and targeted product differentiation. PW Consulting stands ready to help translate that combination into near‑term commercial wins and durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Isododecane For Cosmetics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com